For decades, the economic narrative of Asia’s two most populous economies was elegantly simple. China was the roaring dragon, its growth an inexorable force of nature reshaping the world. Meanwhile, India was the elephant, vast and stirring but always lumbering a few paces behind. That long-held script is now being gradually rewritten. A cocktail of diverging demographics, geopolitical shifts and fundamentally different economic blueprints is redrawing the long-term map for these two Asian behemoths. While the sheer scale of China’s economy still casts a long shadow, India currently has the greater economic momentum, which could set the stage for convergence in the coming decades. The story of the 21st century will, in no small part, be the story of this rivalry. For further analysis and projections, see our Consensus Forecast.

Macroeconomic Overview

GDP and GDP per Capita

The starkest measure of the economic chasm carved out over the past three decades is Gross Domestic Product (GDP) per capita. In 2024, an average citizen in China is, on a nominal basis, nearly five times richer than their Indian counterpart. China’s GDP per capita hovers around USD 13,000, while India’s GDP per capita is a more modest USD 2,700.

This disparity is surprisingly recent. As late as 1990, India was marginally the wealthier of the two nations. The subsequent divergence was nothing short of explosive. China, harnessing a model of state-directed, export-oriented industrialization, powered by a seemingly limitless reservoir of low-cost labor, catapulted itself from poverty into the ranks of middle-income nations.

With both countries having similar populations, this means that China’s total GDP is close to USD 20 trillion—making it the world’s second-largest economy behind the U.S. In contrast, India’s GDP is a more modest USD 4 trillion.

The Key Economic Sectors in China and India

The engines of each economy reveal contrasting economic journeys. China has become, unequivocally, the “workshop of the world”. Its economic heart is a colossal industrial sector, which has moved relentlessly up the value chain from cheap textiles to sophisticated electronics and high-tech manufacturing. It is a state-driven machine, designed for scale and global dominance. Investment and exports are key growth drivers, while private consumption makes up a comparatively weak 40% of GDP due to the lack of a social safety net.

India’s story is different. Its growth has been powered not by factories but by keyboards. The services sector is the crown jewel of the Indian economy, contributing over half of the nation’s Gross Value Added (GVA) and more than a third of its total exports. Within services, IT is a particular strength thanks to the country’s English proficiency and large numbers of engineering graduates, with companies such as Tata, Infosys and HCL now global players. While India’s manufacturing ambitions are significant, championed by the “Make in India” initiative, the sector’s contribution to GDP has actually decreased slightly in recent years. At the same time, private consumption is far more important to India’s economy than China’s economy, worth around 60% of total output.

This structural divergence is mirrored in labor markets. China has orchestrated a monumental migration from farm to factory. India’s transition has been less linear. The South Asian nation’s urbanization rate is close to half China’s at 36%; a vast proportion of its workforce remains tied to agriculture, and an even larger segment operates within the sprawling, unregulated informal economy. This persistently drags on productivity, tax collection and wage growth.

Long-Term GDP Outlook in China and India

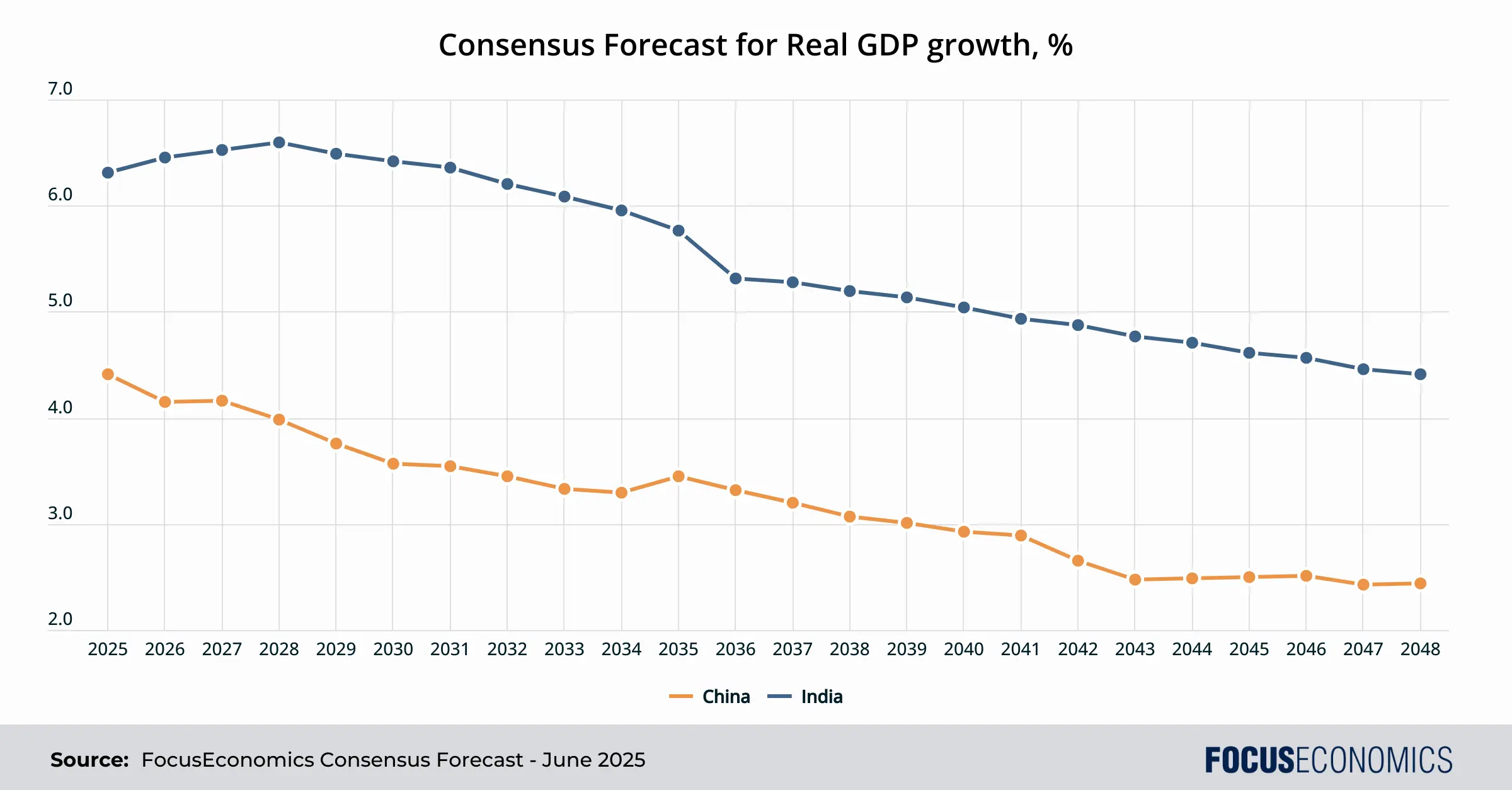

However, the perpetual Chinese outperformance of past decades is now over. Our panelists’ projections suggest that India’s real GDP growth will consistently outpace China’s by more than two percentage points annually in the coming years. The Indian economy should expand above 6% per annum through to the mid-2030s, while China’s growth is expected to soon dip below 4%. This is not a cyclical blip but a structural shift driven by powerful underlying forces.

First and foremost, demographics have become India’s decisive advantage. In April 2023, India officially surpassed China to become the world’s most populous nation. But the headline number masks a more crucial reality: India’s population is young and growing, while China’s is shrinking and rapidly aging. A staggering 65% of Indians are under the age of 35. This “demographic dividend” represents a vast, dynamic pool of labor and a burgeoning consumer market that could—if properly managed—drive demand for decades. China, in stark contrast, faces a “demographic time bomb”, a direct legacy of its one-child policy and subsequent failure to raise the fertility rate since the policy was reversed. A shrinking workforce and a swelling cohort of retirees will act as a powerful brake on long-term growth potential.

Secondly, the simple logic of economic development gives India more runway for growth. Its lower per capita income means the potential for “catch-up growth”—rapid expansion driven by adopting existing technologies and production methods—is far greater than in China, which now finds itself grappling with what economists call the “middle-income trap”. In several technology areas, China has no more catching up to do; Chinese solar, battery and electric vehicle firms are already world leaders in their fields for instance. Beating the trap requires a shift from an investment-led to a productivity-led growth model, a transition made more perilous by an increasingly assertive state sector that risks crowding out the very private-sector dynamism needed to foster genuine innovation.

That said, even India’s path to prosperity is still strewn with obstacles. Chronic infrastructure deficits, a labyrinthine bureaucracy and profound shortcomings in public education and healthcare are formidable barriers to realizing its potential.

As a result, even though India’s growth should outpace China’s, the Chinese economy’s overall size will remain far ahead of that of India. In 2034 for instance, our panelists project China’s GDP at USD 30 trillion, compared to USD 10 trillion for India.

Inflation in China vs India

Historically, inflationary dynamics in both countries have been distinct. In India, the specter of inflation has often been a rural phenomenon, driven by the vagaries of the monsoon. Food items, which carry a heavy weight in India’s consumer price index (CPI) basket, have been the primary source of volatility. Erratic rainfall and inefficient agricultural supply chains have frequently led to painful spikes in food prices, which then ripple through the broader economy. Over the last decade, Indian inflation has tended to fluctuate in the 3–7% range.

China’s inflation narrative has been more industrial. Its breakneck economic expansion created an insatiable demand for global commodities, from iron ore to oil. Consequently, its inflation has often danced to the tune of global commodity price cycles. Recently, China’s recent challenge has not been inflation but its opposite: Deflation. A combination of industrial overcapacity, a property sector downturn and weak consumer confidence has created persistent downward pressure on prices, which fell in annual terms for four straight months from February–May 2025. Deflation tends to be a more difficult problem for policymakers to solve—as Japanese monetary authorities can attest, having grappled with it persistently since the 1990s.

Looking forward, as India’s economy modernizes, the importance of food inflation should gradually wane. Better logistics, a more developed food processing industry and rising incomes encouraging the consumption of non-staple goods and services will smooth out the volatility. Instead, the key challenge for the Reserve Bank of India (RBI) will be managing the demand-side pressures that come with sustained high GDP growth. Anchoring inflation expectations through a credible monetary policy framework will be paramount.

For China, the primary battle will continue to be against deflation. The government’s success will hinge on its ability to pivot the economy toward domestic consumption and away from its over-reliance on investment and vast manufacturing production. This is a monumental task that involves rebalancing the country’s entire economic model. A successful transition to a more services-oriented economy would fundamentally alter its inflation dynamics, making the price of haircuts and healthcare more important than the price of steel and cement.

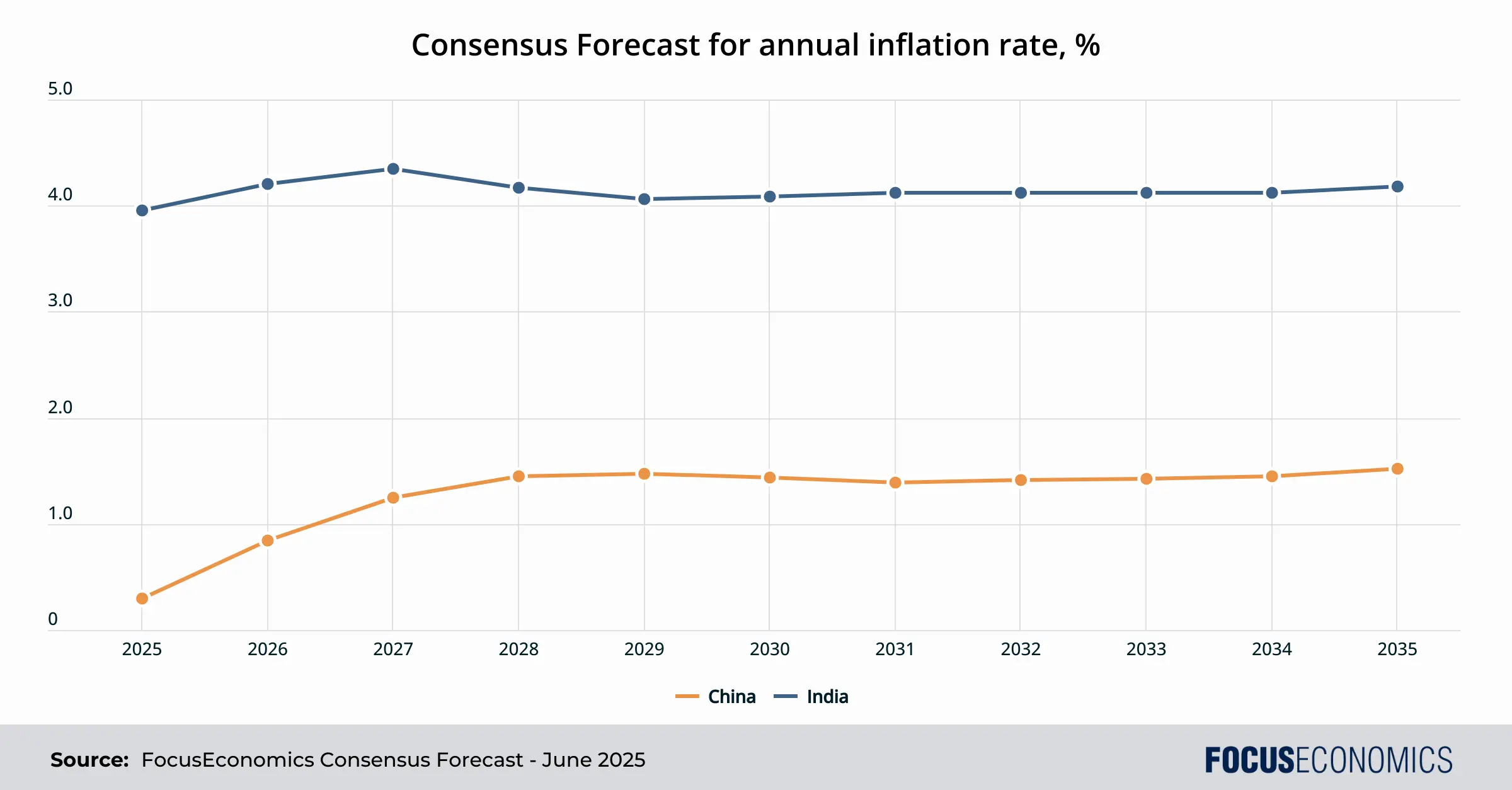

In terms of forecasts, India is likely to continue to see structurally higher inflation than China in coming years as a result of a more buoyant economy, robust population growth and a greater focus on private consumption relative to investment, as can be seen in the below graph:

Interest Rates: Monetary Policy Trends in China and India

The central banks of the two nations, the People’s Bank of China (PBOC) and the Reserve Bank of India (RBI), have navigated very different monetary seas in recent years. The RBI has adopted a conventional, flexible inflation-targeting framework. Its primary mandate is to keep inflation within a specified band in the medium term—currently set at 2.0–6.0%. The RBI uses its repo rate as the main lever, hiking to cool prices and cutting to stimulate growth. Its actions are relatively transparent and follow a playbook familiar to central bankers worldwide.

The PBOC, in contrast, operates with a far more complex and opaque toolkit. It employs a dizzying array of instruments, including price-based tools like the loan prime rate and quantity-based measures such as the reserve requirement ratio for banks. Its mandate is broader and more political, encompassing not just price stability but also economic growth, financial stability, and often, the strategic goals of the Communist Party. This leads to a more interventionist and less predictable policy approach.

Long-term challenges exist for both central banks. The RBI must continuously fine-tune its policy to manage the inflationary side effects of rapid development without choking off growth. The PBOC faces an even trickier task: Orchestrating the deleveraging of a dangerously indebted Chinese economy and transitioning to a more market-driven financial system without sparking financial instability.

Regarding our Consensus, panelists expect that Indian interest rates will average higher than those in China over the coming decades, in line with the South Asian country’s higher projected GDP growth and inflation figures.

Trade in India and China

Each country is plugged into the global trade system in different ways. China’s story is one of unparalleled export dominance. It has become the world’s factory, its ports churning out a torrent of manufactured goods, from cheap toys to iPhones, and its export machine is now pushing aggressively into higher-tech domains. China has run a consistent trade surplus for decades; this surplus reached a record of around USD 1 trillion last year due to muted domestic consumption, a push to reduce reliance on foreign manufactured parts, and booming sales of EVs and electronics.

India’s export basket is a more eclectic mix. Its standout success has been in the realm of services; Indian IT firms and business process outsourcing hubs are integral to the functioning of global corporations. In merchandise trade, its strengths lie in petroleum products (reflecting its refining capacity), pharmaceuticals—particularly generic drugs—and jewelry. Unlike China, India has seen a persistent trade deficit in past years. Between the two nations, trade is heavily geared in China’s favor: In the year ending in March, India’s trade deficit with China widened to a record USD 100 billion.

Looking ahead, the intensifying geopolitical rivalry and trade barriers between the United States and China, coupled with a broader corporate desire to “de-risk” supply chains, is redirecting trade flows. The “China+1” strategy, where multinational firms actively seek to diversify their manufacturing base away from China, represents the single biggest economic opportunity for India in a generation. India has so far managed to maintain a neutral stance in global affairs, allowing it to largely avoid the ire of politicians in Washington and Beijing. The potential to capture a significant slice of global manufacturing is now a tangible reality.

Seizing this opportunity, however, is not a given. It will require a concerted national effort from India to dismantle its own barriers to competitiveness. This means a massive upgrade of its creaking infrastructure, a radical simplification of its regulatory environment, and a quantum leap in the skilling of its workforce. Initiatives like “Make in India” and production-linked incentive schemes are crucial first steps, but the race is long and the competition is fierce—other Asian nations are also keen to grab any lower value-added manufacturing activity that migrates from China.

Meanwhile, China is not standing still. It is responding to these pressures by doubling down on technological self-sufficiency and moving aggressively up the value chain. Its strategy is to become less dependent on the world for technology and make the world more dependent on it for high-value goods. Simultaneously, it is building its own parallel economic ecosystem through schemes like the Belt and Road Initiative, deepening its trade and investment ties with the developing world and creating a sphere of influence less dependent on Western markets.

Public Debt

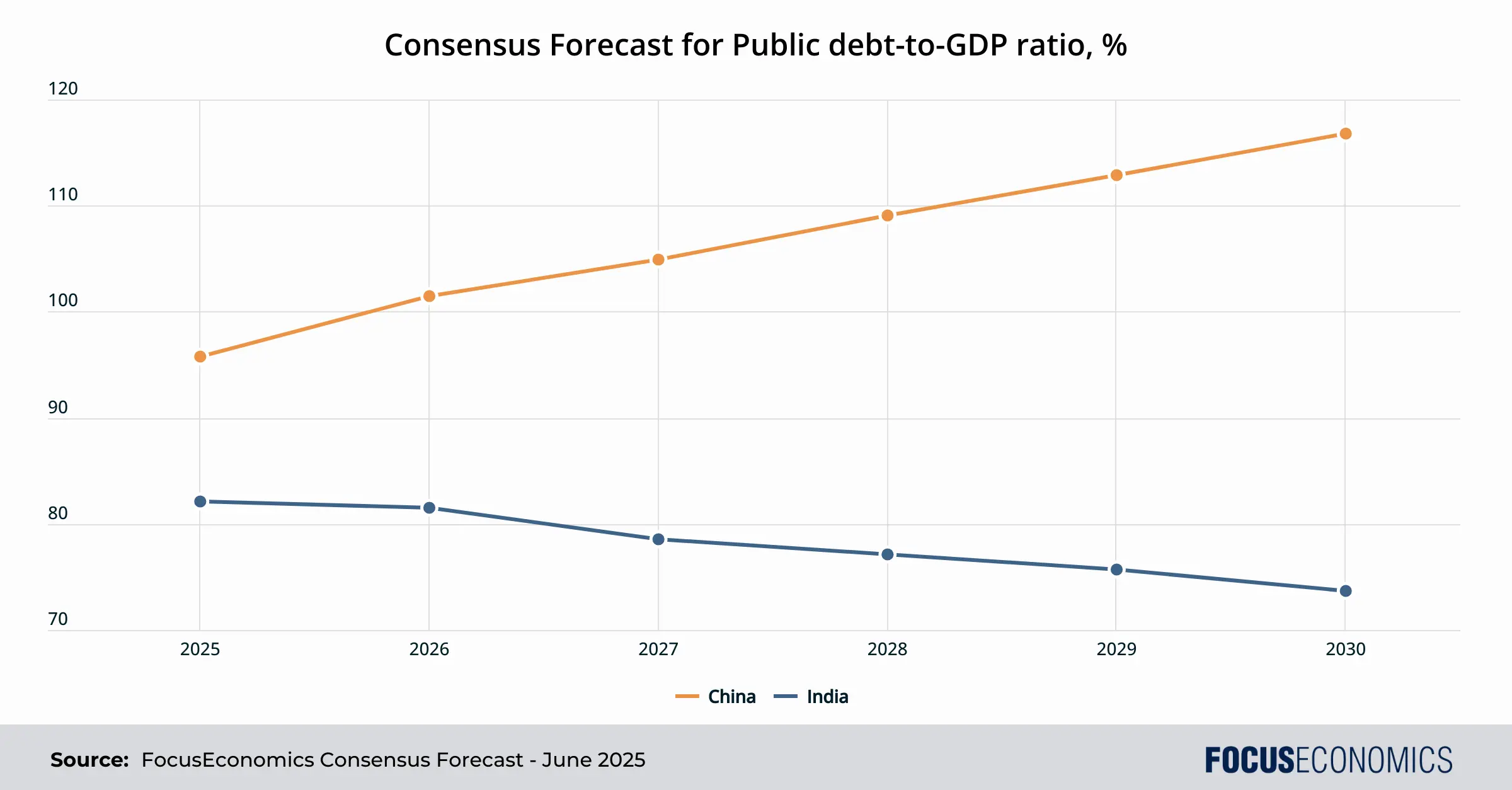

The specter of debt looms large over both these economic giants. On the surface, their headline public debt-to-GDP ratios appear similar, with China’s at around 88% and India’s at 81% in 2024. However, the nature and trajectory of their debt profiles are worlds apart.

China’s public debt problem is arguably the biggest single risk to its economy. The headline figure conceals a much larger mountain of hidden debt, particularly at the local government level, accumulated through off-balance-sheet financing vehicles to fund a gargantuan infrastructure and property boom. This debt is opaque, its quality is questionable, and the risk of a systemic financial crisis, while managed by the state, is ever-present. The long-term sustainability of China’s debt is contingent on its ability to navigate a controlled demolition of its property bubble and restructure its local government finances without triggering a catastrophic collapse.

India’s public debt, while high, is generally considered more transparent and more stable. It is predominantly held domestically and denominated in its own currency, which contains vulnerability to external shocks and currency fluctuations. The primary risk for India is that the high cost of servicing this debt crowds out essential public investment in infrastructure and human capital, thereby constraining its long-term growth potential.

Regarding the outlook, our expert analysts expect rapid GDP growth to enable India to shrink its debt pile as a share of GDP in coming years: In contrast, China’s debt burden is forecast to rise as the workforce shrinks, economic growth slows, and health and social spending demands increase.

Fiscal Balance

As is clear from the above, both governments consistently spend more than they earn, running fiscal deficits that were exacerbated by the pandemic. China has long used fiscal policy as a primary tool of economic management, unleashing stimulus packages—primarily funneled through state-owned enterprises and local governments—to boost growth whenever it has faltered. This has led to the creation of world-class infrastructure but also to monumental waste and the build-up of unproductive assets.

India’s fiscal policy has been more constrained by its high debt burden and a narrower tax base. While it has also used fiscal stimulus to support the economy, its firepower is more limited.

Looking ahead, both nations will likely continue to run sizable fiscal deficits, but with China’s expected to be larger than India’s due to the same aforementioned factors driving up the public debt ratio. For China, the key task is to rein in the profligate and often unaccountable borrowing of its local governments and to shift public spending toward social safety nets to boost consumption. For India, the priorities are to widen its tax base—particularly by bringing more of the informal economy into the formal system—to improve tax compliance, and to rationalize its extensive subsidy programs.

Exchange Rates

The rupee has been on a long-term depreciating trend against the U.S. dollar, a reflection of India’s higher inflation differential with the US and its persistent current account deficit. The RBI’s approach has been to softly manage India’s exchange rate, intervening to curb excessive volatility but generally allowing market forces to determine the currency’s direction.

China’s exchange rate, in contrast, is more tightly controlled. Its value is not a true reflection of market forces but a carefully calibrated instrument of national policy. The PBOC manages it against a basket of currencies, using it as a lever to support exporters, manage capital flows and project economic stability.

The long-term outlook for both currencies is divergent. While China’s yuan should appreciate due to persistently lower inflation than the U.S., India’s will remain on a depreciatory trend due to relatively high price pressures and its chronic current account deficit.

In terms of global importance, Beijing has ambitions for the yuan to challenge the U.S. dollar’s dominance as the world’s reserve currency. Achieving this, however, would require a level of capital account liberalization and financial market transparency that seems fundamentally at odds with the Communist Party’s desire for control. That said, the use of both the rupee and yuan in cross-border trade settlements is likely to increase in the coming years as governments in both countries look to promote their local currencies, even if the U.S. dollar will likely remain preeminent.

Population History and Outlook

No single factor will shape the destinies of these two nations more profoundly than their sharply diverging demographic trajectories. India’s population is set to continue growing until the 2060s. Its greatest economic asset is its people—young, aspirational and increasingly connected. This demographic dividend is a powerful engine for growth, but it is also a race against time. India must create millions of jobs each year to absorb the youth entering the workforce; failure to do so would risk turning this demographic dividend into a demographic disaster, fueling social unrest and instability. This requires a reorientation of the economy towards more labor-intensive manufacturing or services activities.

China’s population, meanwhile, is in decline. Its workforce has already peaked, and the number of elderly dependents is set to explode. This will place strain on its public finances, particularly the pension and healthcare systems. China’s challenge is to get rich before it gets old; it is a race it is in danger of losing.

Summary

The economic rivalry between India and China has entered a new, unpredictable and arguably more fascinating leg. The era of China’s seemingly effortless, gravity-defying growth is decisively over. It now faces the formidable triple challenge of escaping the middle-income trap, defusing its debt bomb and coping with a demographic winter. Its future economic growth will be slower, harder won and more contested.

India, by contrast, is stepping onto the accelerator. Buoyed by favorable demographics, geopolitical tailwinds and a vast potential for catch-up growth, it is poised for a multi-decade run of rapid expansion.

However, India’s ascent is not guaranteed. Its future prosperity depends entirely on its ability to confront its own deep-seated structural demons: Reforming its bureaucracy, building world-class infrastructure and educating its youth. And in China, a fresh burst of private-sector liberalization combined with reforms to unlock huge household savings could yet provide renewed impetus to the economy. The unfolding rivalry between the elephant and the dragon will be one of the defining economic spectacles of the coming decades, a competition that will not only determine each country’s future but will also profoundly reshape the global balance of power.