What is the difference between light and heavy crude oil?

The difference between the two has to do with its liquid density to water. You may have heard the term “light” crude oil; this refers to oil of a lower density. The lower the density, the easier it is for it to be refined into gasoline or diesel fuel. Conversely, the higher the density, or “heavier,” the oil is, the harder it is to refine. Therefore, generally speaking, light crude oil tends to fetch a premium in the oil futures market, as it is easier to refine and produces a greater amount of gasoline or diesel fuel. Heavier crude oils are cheaper because they aren’t as easily refined, needing more advanced methods and technologies for refinement. For a consolidated view of projections and analysis, see our Consensus Forecast.

What is API Gravity? How does it measure the density of crude oil?

The American Petroleum Institute gravity (API gravity) is a measurement of the density of oil. This number will normally fall somewhere between 10 and 70. “Light” crude oil will float on water and the higher the API gravity of the crude oil or liquid petroleum the “lighter” it is. If the API gravity is lower, it might be considered “heavy” and will sink in water.

What is the difference between sweet and sour crude oil?

Another metric that is taken into account when judging the quality of crude oil is the sulfur content. The difference between sweet and sour crude oil lies in the sulfur content of the oil, which is measured against a benchmark of 0.5%, with anything higher than the half percent considered “sour” and anything lower considered “sweet”. Sweet crude oil also tends to command a premium in the futures market, similar to light crude oil, it is easier to refine into petroleum products.

What is the difference between sweet light crude oil and heavy sour crude oil?

If we put all of the above together, we have at one end of the spectrum sweet light crude oil, the holy grail so to speak, and at the other end heavy sour crude oil with some medium grades somwehere there in the middle. Sweet light crude oil has a lower liquid density to water and a lower sulfur content while heavy sour crude oil has a higher liquid density to water and a higher sulfur content. The light and sweet variety is preferred to its heavy and sour counterpart because of the amount of processing necessary to remove impurities for refinement into fuels such as gasoline and diesel. However, being that light and sweet crude is of a higher quality than its counterpart, it will probably cost you a pretty penny in the futures market.

How is crude oil processed and used?

Crude oil is used to produce various types of fuel—possibly the most notorious of which being gasoline, but how does it go from being raw crude to the gasoline that you put in your car? After crude oil is extracted it is transported to refineries where it is converted into finished petroleum products such as gasoline and diesel. Without getting too technical, refinement generally involves a distillation process to purify the oil. This is done basically by heating the oil and separating the useful stuff (fuel) from the not-so-useful. However, more sophisticated processes and equipment must be used to determine how much of each barrel of crude oil should be refined into the different types of fuel that the market demands. What this does is minimize the production of lower-value fuel types to maximize the production of higher value fuel. According to the University of Delaware, around 50% of each barrel of crude is converted into Gasoline, 40% is converted into middle distillates such as diesel fuel, heating oil, kerosene and jet fuel, while only 10% is refined into what they refer to as residual fuel oil. This residual fuel oil is of the lowest value and is used to, among other things, power large ocean going ships and freighters.

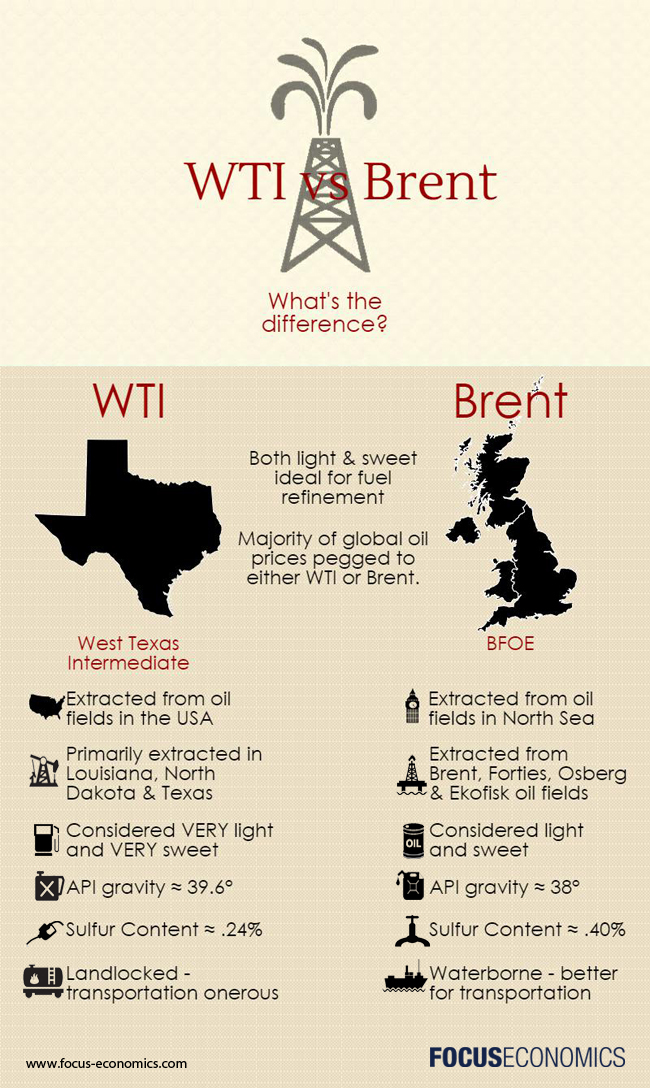

Brent and WTI Crude Oil: What’s the difference?

Global production and consumption of oil has continually increased over the years—according to IEA statistics, more than 90 million barrels are produced and consumed globally per day. As the demand for crude oil increases, the more crude oil is produced and traded all over the world, however, all of these different crude oils need some kind of benchmark on which to base their pricing structures.

Brent and WTI are two major trading classifications of crude oil and serve as the two major benchmarks for crude oil pricing globally, however, Brent has been adopted increasingly as the preferred benchmark in recent years. According to ICE Futures, it is estimated that 60% of the world’s traded oil is priced off of Brent. Before getting into the Brent and WTI’s importance to the futures market, we should take a look at the differences between the two.

!function(a){var b=”embedly-platform”,c=”script”;if(!a.getElementById(b)){var d=a.createElement(c);d.id=b,d.src=(“https:”===document.location.protocol?”https”:”http”)+”://cdn.embedly.com/widgets/platform.js”;var e=document.getElementsByTagName(c)[0];e.parentNode.insertBefore(d,e)}}(document);

Embed

Brent Crude Oil

Originally Brent referred to oil extracted from the Brent oilfield located in the North Sea off the coast of the UK, however, for various reasons Brent now refers to four different crude oil grades extracted from various wells in the North Sea – Brent blend, Forties blend, Osberg, and Ekofisk (together also known as BFOE). This mixing of the four oil grades actually made Brent a heavier oil, although it is still considered to be relatively light and low in sulfur.

While Brent is relatively heavier than it was in the past, it is still ideal for oil refinement and the fact that it is waterborne from oil fields near to the coast of the UK and Norway makes it all the more attractive. Transportation of Brent is easier and less costly due to the location of its extraction sites. After it is extracted, the oil is transported to a floating vessel near the oil platform called an FPSO (Floating Production Storage & Offloading) where it can be produced and stored. This makes Brent crude oil very accessible for means of transportation. The oil can be offloaded from the FPSO directly onto oil tankers and easily transported across the world by sea. It can also be sent a short distance away to oil terminals like Sullom Voe Terminal in the Shetland Islands, where it can be stored before loading on to tankers. It is also be sent via pipeline to refineries and storage facilities on the coast of the UK. The relative ease of transportation and its high quality makes Brent an attractive investment and plays a major part in the pricing of crude oil as well as in the adoption of Brent as the major oil benchmark price globally.

WTI Crude Oil

WTI or West Texas Intermediate is the other major global benchmark oil for price setting and is actually of better quality than Brent. It is extracted from wells in the United States and is considered to be a very sweet and very light crude oil.

Although WTI is a sweeter and lighter crude than Brent, a major drawback is that it is landlocked meaning that transportation is more expensive and more involved than it is for a waterborne crude oil such as Brent. WTI is extracted across the US and sent via pipeline to Cushing, Oklahoma where it is stored. Then it must further rely on the capacity of pipelines or rail to get it to refineries in the gulf coast region so that it may finally be transported across the world or wherever its final destination may be after refinement. Brent, as mentioned earlier, is waterborne and therefore is much easier to transport. Although it has been the leading global benchmark crude in the past, many analysts believe that for all the quality WTI has in terms of density and sulfur content, the fact that it is extracted from land undermines it’s potential to be the leading global benchmark for crude oil pricing.

What are the density and sulfur content measurements of Brent and WTI?

It is hard to put an exact number on both oils, as they come from different oil fields in their respective parts of the world. Brent has an API gravity of around 38 degrees and a sulfur content of somewhere around .40%. As was mentioned earlier, WTI is a lighter and sweeter crude with an API gravity of 39.6 degrees and a sulfur content of 0.24%.

What is the role of Brent and WTI in the futures market?

There was a time when crude oils were traded based on the spot price, which is the current price at which securities, in this case crude oil, can be bought or sold at a given time and place. However, the volatility of crude oil prices necessitated some kind of solution to minimize the risk of the ever changing prices, which came in the form of futures. As was mentioned earlier, these futures are tied to benchmark oils whose prices are traditionally less volatile allowing traders to lock in a price to buy or sell crude oil months or possibly even years in advance. This is where Brent and WTI come in.

WTI and Brent were both for many years globally accepted as benchmark oil prices, as the prices were essentially the same. However, the prices of the two crude oils began to diverge in 2011, and although the prices converged once again beginning in late 2014, the 2011 divergence, or the reasons behind it, may have contributed to the widespread adoption of Brent as the global benchmark oil price.

The divergence in the prices between the two has been attributed to many things. Some believe it was due to the gradual depletion of Brent oil in the North Sea, while others have cited the oversupply of WTI oil in the U.S. as the culprit. Production of WTI has significantly exceeded the capacity of the oil pipelines for transportation in recent years, while oil production in Canada has rapidly increased. Although Brent was always more likely to be used in Europe as the benchmark, this oversupply of oil in North America and lack of reliable transportation prompted Brent to be adopted as the benchmark for oil trading markets even on the east coasts of the U.S. and Canada.

WTI is now being transported by rail, which is significantly more expensive than by pipeline. Brent’s waterborne oil is perhaps more attractive to investors, which may be what prompted pricing hubs to adopt Brent as the benchmark while its price rose and WTI’s price stagnated.

Some have stated that the increasing adoption of Brent is simply a case of the oil being seen as a more reliable indicator of global crude oil prices because of the increase of its adoption globally.

How do supply and demand influence market prices of crude oil?

The reasons for the adoption of Brent as the preferred crude oil for global pricing is debatable, but what is clear from the above is that the laws of supply and demand play a big role in the price of oil – as demand increases and supply decreases, price increases and vice versa.

In general, many different factors can move the price of commodities, especially oil, such as currency movements, variations in regional demand, geopolitical concerns, and politics among many other factors.

Supply and demand are the fundamental drivers that affect all commodities prices – there is a reason they are referred to as laws. However, the two fundamental drivers have been on show for all to see with regard to oil prices in the last year.

A good anecdote to demonstrate how the price of oil is highly influenced by supply and demand can be seen in what has taken place over the last year as an unprecedented global oil glut has impacted oil prices significantly. On January 15, the price of Brent was USD 28.1 per barrel and WTI traded at USD 29.5 per barrel which marked a 41.2% and a 36.5% annual drop respectively.

Brent and WTI were not alone, however, as OPEC oil prices were also hit hard by the oversupply. On 20 January, the OPEC oil basket price fell to USD 22.5 per barrel marking the lowest price since 2002. The reading marked a sharp 47.8% drop on an annual basis.

The roots of the global oil glut go back a few years. Along with a ramp up in US oil production in recent years, Canadian and Iraqi oil production has been rising year after year, and Russia, amid its economic issues, has still managed to pump oil at record rates. Saudi Arabia’s strategy beginning back in mid-2014 to produce at record-high levels in an attempt to price higher cost producers out of the market is also more than worth mentioning. And lest we forget, Iran’s economic sanctions removal earlier this year that has only served to add to the glut, as it paved the way for a surge in oil exports from the country.

China’s economic slowdown that seemed to creep up on everyone semi-unnoticed last year sparked fears of a global economic slowdown and demand for oil decreased as a result. In early 2016, the world economy appeared to be following suit, which was affirmed by Q1’s dismal growth data.

After prices came down to record lows in January, it was announced that an agreement to freeze oil production was in the works between Russia, Saudi Arabia and other OPEC members in an effort to curb oil production to bring prices up. However, when Saudi Arabian Minister of Petroleum and Mineral Resources Ali al-Naimi announced shortly thereafter in February that, “oil production cuts won’t happen,” doubts arose as to the viability of such a deal to prop up oil prices. Further uncertainty arose after it became clear that both Iran and Iraq were reluctant to join the pact. Although oil prices did recover slightly after the February announcement, production kept up and positive sentiment over the announcement faded, keeping prices low.

On 17 April, the long-awaited Doha meeting between oil chiefs from the world’s biggest oil producers, was supposed to yield an oil production freeze between the members. Alas, it did not come to fruition and prices were held down. OPEC’s June meeting in Vienna failed to yield a production cap yet again, however, by that time prices began to creep back up.

In Q2 prices started to come back up as second quarter growth data from the world’s major economies was unexpectedly positive after the disappointing Q1, which ramped up demand. This coupled with production disruptions in Canada due to wildfires destroying much of the oil sands region and rebel forces attacking Nigerian oil pipelines, brought prices back up above USD 50 in June.

It looked as if oil prices were rallying spectacularly from the over-10-year lows hit in January, but the infamous Brexit halted the oil price rise. Fears over the world economy stemming from Brexit have driven investors away from oil to safe haven assets, namely gold and the U.S. dollar, in recent weeks. Canada has returned to production after the Alberta wildfires, Nigeria’s geopolitical issues have abated, and U.S. oil producers have been turning the taps back on. As a result, renewed negative sentiment over the global oil glut has once again dampened demand and prices have been falling since.

It is difficult to say where oil prices will go from here, but one can see that it is evident from the above that supply and demand have a tremendous effect on oil prices.

Where are Brent and WTI traded?

So, you might ask yourself, where are Brent and WTI traded? WTI futures are chiefly traded in New York City at the New York Mercantile Exchange (NYMEX) while Brent contracts are traded through ICE Futures Europe, which is located in London. Although most trading and transactions are done electronically these days, the NYMEX, much like the New York Stock Exchange (NYSE), still has a small venue in which traditional open outcry trading is still practiced on the floor, in which traders shout and employ complex gestures during the buying and selling process.

Conclusion

Although oil influences so much of our daily lives we almost take it for granted. Prices have been falling steadily over the past year, leading to cheaper goods for consumers, and most notably cheaper gas prices, putting a bit more money in our pockets. The supply and therefore price of oil impacts us every day whether we are aware of it or not. Brent and WTI are especially important because they are the global benchmark oils relied upon to set prices for oil produced all around the world.

As was mentioned previously, the global oil glut looks as if it will continue to impact oil prices, keeping the prices low, especially as normalizing Iran means that even more oil will flood the market in the near future. According to FocusEconomics Senior Economist Ricardo Aceves, “Although the generalized view is that oil prices will recover going forward, the majority of analysts continue to adjust their price projections down or maintain them unchanged in light of the recent developments.”

While they differ in a variety of areas including density and sulfur content, extraction locations and transportation, as well as futures prices, Brent and WTI Crude Oil are arguably the most important crude oils to global futures markets. In fact, oil is the leading energy commodity futures contract in the world by volume. It’s no secret that oil is integral to our lives and knowing a bit more about this key commodity can at the very least give you some interesting bar conversation topics.

Author: Brian Dowd

Related Pages:

Energy Commodities

Brent Crude Oil

WTI Crude Oil

|

Sample Commodities Report

Get a sample of our new Consensus Forecast Commodities report Price forecasts, historical data, & written analysis 33 commodities in the energy, metals & agricultural sectors. |