With the war in Ukraine dragging on into its fourth month, fierce fighting ongoing in the country’s Eastern Donbas region, and sanctions on Russia being stepped up, both economies are suffering heavily from the conflict. However, Ukraine is taking by far the heavier toll. Almost five million Ukrainians—over 10% of the population—have fled the country. This, combined, with the conscription of working-age men for the war effort, is resulting in a drastic reduction in the labor force. Moreover, economic damage already runs into the hundreds of billions of dollars, while Russian control of the majority of Ukraine’s sea ports and its blockade of those ports still in Ukrainian hands is restricting trade—especially shipments of grains, Ukraine’s key export before the war.

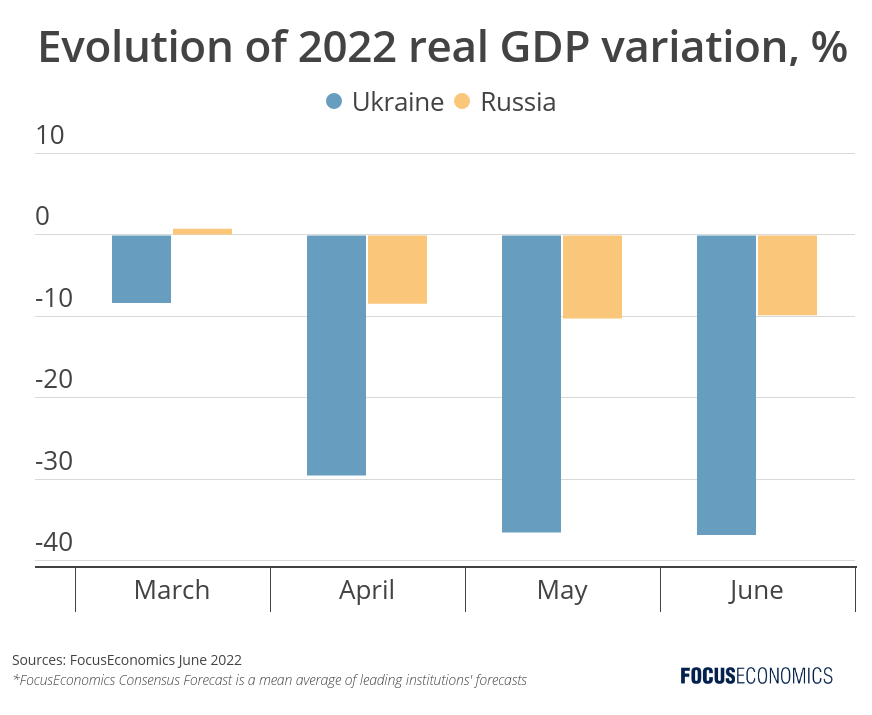

While high-frequency economic indicators are no longer being published due to the conflict, our analysts have grown increasingly pessimistic about Ukraine’s prospects in recent months, and now expect a 36.8% contraction in 2022 in our most recent monthly report. Further downgrades to forecasts are likely in coming months in the absence of any positive news on the war front. A lasting ceasefire is key, although other possible developments—such as the establishment of a corridor for the export of Ukrainian grain, which is currently under discussion—would also improve Ukraine’s outlook somewhat.

On the other hand, over the last month our analysts have grown slightly more upbeat about Russia’s economy, and now forecast a 9.8% contraction compared to the 10.2% fall expected last month. The latest economic data does not yet point to a wholesale economic collapse. GDP grew year-on-year in Q1, and contracted just 2.6% in April. Sky-high oil prices are buoying government coffers, while capital controls have boosted the ruble to above pre-war levels, allowing the Central Bank to slash interest rates to aid economic activity.

That said, the damage from Western sanctions is likely to grow with time. The Energy Information Administration sees Russia’s energy output falling by around 18% over the next 18 months, while close to 1000 companies have now curtailed their operations in the country. And while Russia’s economy will contract by far less than that of Ukraine, our analysts are still clear that on the economic front, neither country will emerge as the victor.

Insight from our analyst network:

On Ukraine’s longer-term prospects, the EIU said:

“Assuming that the war continues throughout the forecast period, albeit at a weaker intensity from 2023 onwards (our central forecast), the economy will rebound in 2023 by 9.1% owing to the reconstruction effort, supported by an influx of development aid. Growth will average 4.4% in 2024‑26, with a full recovery unlikely owing to Russia’s aim to cripple Ukrainian infrastructure and the continuous blocking of Ukraine’s ports in the Black Sea, inhibiting export flows. We do not expect real GDP to reach to pre-war levels before 2037.”

On economic dynamics in Russia, analysts at Goldman Sachs said:

“In Russia itself, output appears to be declining by less than we forecast. In our view, this resilience is due to the ongoing impetus from the post-Covid normalisation of economic activity. Nevertheless, given the combination of much tighter financial conditions and a commodity-driven squeeze on household incomes, we suspect that the slowdown has been delayed rather than avoided. Reflecting this, we have raised our 2022 growth forecasts, but lowered our 2023 projections.”