Vincent Loo has been a senior economist at KAF Research since November 2019. Prior to joining KAF, he had spent more than 12 years working in the field of economic research with other research and investment firms. His previous occupations include senior economist at RHB Banking Group and assistant manager at KFH Research. He holds a bachelor´s degree in economics and finance from Curtin University.

Vincent Loo has been a senior economist at KAF Research since November 2019. Prior to joining KAF, he had spent more than 12 years working in the field of economic research with other research and investment firms. His previous occupations include senior economist at RHB Banking Group and assistant manager at KFH Research. He holds a bachelor´s degree in economics and finance from Curtin University.

Woon Khai Jhek is a senior economist at RAM Ratings. As part of the research unit, he provides macroeconomic analysis and projections on the Malaysian economy. He is also responsible for the production of the Bond Market Monthly, which reviews the performance and prospects of the Malaysian fixed-income market. Prior to joining RAM, he had been a research analyst at CEIC, a global economic database provider. He holds a BSc in economics from the University of Michigan and is also a CFA Charterholder.

Woon Khai Jhek is a senior economist at RAM Ratings. As part of the research unit, he provides macroeconomic analysis and projections on the Malaysian economy. He is also responsible for the production of the Bond Market Monthly, which reviews the performance and prospects of the Malaysian fixed-income market. Prior to joining RAM, he had been a research analyst at CEIC, a global economic database provider. He holds a BSc in economics from the University of Michigan and is also a CFA Charterholder.

Atiqa Noor Azlan is an economist at the research department of Kenanga Investment Bank. She is experienced in the areas of economic analysis, public policy and growth development. Prior to joining Kenanga, Atiqa worked at Bright Vision Consulting and Bank Negara Malaysia. She holds a bachelor’s degree in economics with a minor in Chinese language and international studies from the Pennsylvania State University.

Atiqa Noor Azlan is an economist at the research department of Kenanga Investment Bank. She is experienced in the areas of economic analysis, public policy and growth development. Prior to joining Kenanga, Atiqa worked at Bright Vision Consulting and Bank Negara Malaysia. She holds a bachelor’s degree in economics with a minor in Chinese language and international studies from the Pennsylvania State University.

Ahmad Nazmi Idrus is a senior economist at RHB Research Institute. With a demonstrated history of working in the financial services industry, government institutions and the Central Bank he is experienced in macroeconomics, policy analysis and econometrics. Prior to joining RHB he worked in the Malaysian BioeconomyDevelopment Corporation, the Retirement Fund Incorporated and Bank Negara Malaysia. He holds a masters degree in economics from the University of Warwick, as well as one from Lund University.

- FE: Could the new restrictions imposed in mid-January threaten the recovery?

RHB: Yes, the government expects a loss of MYR 600 million [around USD 148 million] for each day the economy is under the measure. Our expectation is much less at MYR 430 million [around USD 106 million] a day due to non-compliance. But the overall impact on the economy is expected to be significant.

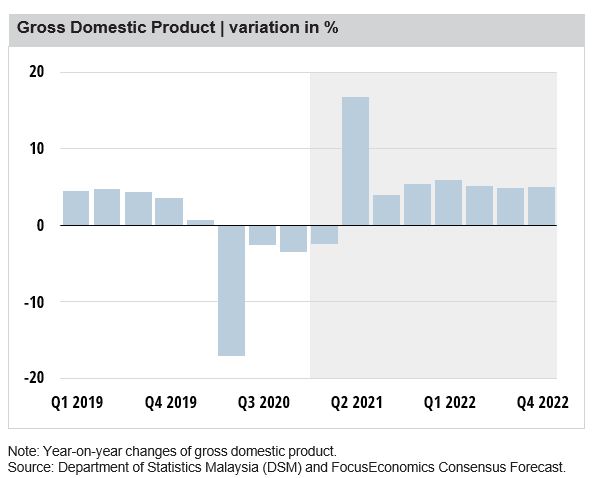

KIB: Yes, the new lockdown (MCO2.0) involves mobility restrictions and closure of certain business operations. These have hindered purchasing activities, and weighed on sentiments of both businesses and households, resulting in worsening labour market conditions. However, on 10 Feb, the government relaxed some of the rules, allowing the reopening of most retail sectors and permitting dine-in. Hence, following this relaxation, 1.0 (government’s estimate: MYR 2.4 billion), it is still much higher than the MYR 200–300 million projected by Bank Negara Malaysia (BNM) amid the conditional MCO (CMCO) in October– November. Hence, we should see a further deceleration in economic growth come 1Q 2021. The current extension until 18 February 2021 has led us to trim our full-year GDP forecast to 5.5%, from our initial projection of 7.1% prior to the imposition of MCO 2.0. Every subsequent day of extension after that is estimated to trim 0.04 ppt off growth this year.

RAM: We estimate daily economic losses from MCO 2.0 at about MYR 500–600 million. While this is less severe than MCO 1.0 (government’s estimate: MYR 2.4 billion), it is still much higher than the MYR 200–300 million projected by Bank Negara Malaysia (BNM) amid the conditional MCO (CMCO) in October– November. Hence, we should see a further deceleration in economic growth come 1Q 2021. The current extension until 18 February 2021 has led us to trim our full-year GDP forecast to 5.5%, from our initial projection of 7.1% prior to the imposition of MCO 2.0. Every subsequent day of extension after that is estimated to trim 0.04 ppt off growth this year.

KAF: Yes, we expect the latest restrictions to pose a further drag on 1Q 2021 GDP, which could delay the eventual recovery but is unlikely to derail it. Economic activity is expected to recover from 2Q 2021 onwards on the back of the vaccine rollout and the anticipated lifting of restrictions.

- FE: In January, the government announced a new fiscal package to address the socioeconomic impact of the new restrictions. Are the measures sufficient? Do you expect any further fiscal stimulus measures

RHB: The measures should be enough for the length of current lockdown. Any longer, the government may need to come up with greater support.

KIB: Provided that we are heading to a gradual economic reopening since 10 Feb, I view the package as sufficient. However, should the Covid-19 cases remain unabated even after the kick-off of the vaccine distribution, resulting in a retightening of the MCO, another fiscal package is needed. Measures should remain targeted, allowing a swift transfer of funds to the pockets of individuals that have been adversely affected.

RAM: Fiscal stimulus measures related to mitigating the pandemic’s economic impact are likely as current legislation provides additional fiscal flexibility despite rising tax revenue pressures. In Budget 2021, the government had already allocated up to MYR 17 billion under the Covid-19 Fund in 2021, which has yet to be utilised. The Temporary Measures for Government Financing (Coronavirus Disease 2019 (Covid-19)) Bill 2020 allows the government to debt fund various stimulus measures (e.g. the wage subsidy programme and cash transfer programmes) and vaccine acquisition via this Fund. Given that the risk to the government’s growth forecast of 6.5%–7.5% has intensified amid the recent lockdown, we expect a higher likelihood of targeted stimulus rollout in the near-term.

KAF: January’s PERMAI fiscal package is hardly sufficient. Considering that it is mainly a reprioritisation of existing funds and not a fiscal injection, it would not have a major impact on the economy. Any further fiscal stimulus depends on how long the current containment measures last. I do not rule out more fiscal stimulus announcements by the government this year, but the size of stimulus may likely be small due to the fiscal constraints.

- FE: Do you expect the government to achieve the fiscal targets set in the 2021 budget? What is your outlook for fiscal policy this year and next?

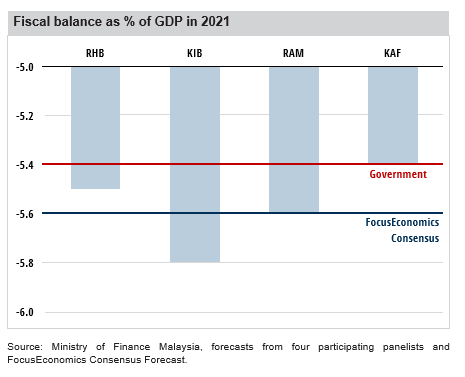

KIB: Fiscal policy will likely remain expansionary as evidenced by the record-high expenditure planned under Budget 2021. This is applaudable as we do not want to have a premature withdrawal of support measures, which would just weigh on the sustainability of the growth recovery. Our in-house deficit forecast (5.8%) is slightly wider than the government’s (5.4%), mainly because some of the measures announced under the PERMAI package would result in greater forgone revenue.

RHB: The target is somewhat optimistic in our opinion. The slow pace of recovery and lower revenue collection may affect the deficit target. We expect the deficit at -5.5% of GDP.

RAM: Achieving the government’s fiscal deficit target of 5.4% of GDP in 2021 will be challenging as the weaker-than-anticipated economic conditions will suppress tax revenue growth. […] Fiscal policy is expected to remain supportive of growth in 2021 and 2022. However, without an upward revision or relaxation to the government’s current debt ceilings, the government’s ability to support the economic recovery will be significantly constrained.

KAF: Yes, as the government has in the past been quite consistent in achieving its annual fiscal targets. The government is still committed to fiscal consolidation over the medium-term. I expect the fiscal deficit to be reduced gradually to 4.4% of GDP in 2022, from 5.4% in 2021. However, it would still be higher than pre-pandemic levels of 2.8–3.7% of GDP.

- FE: In its first meeting of the year, the Central Bank held its policy rate. Do you consider its stance accommodative enough? What is your outlook for monetary policy ahead?

RHB: If lockdown gets tighter or longer, the economy may need more support. We expect rate cuts in March and a possibility of another one in 2Q 2021 if the current economic trajectory remains and infections are high.

KIB: Yes, it is accommodative enough. Against the prospect of recovery (especially in 2Q 2021 onwards), wider rollout of vaccines, stronger external demand (technology upcycle, persistent demand for Covid-related supplies) and the BNM governor’s emphasis on the greater effectiveness of targeted measures, we expect the BNM to keep the policy rate unchanged at 1.75%. Nonetheless, should the Covid-19 situation take a turn for the worse, leading to further tightening of the lockdown measures, we believe that the BNM has ample room to cut the policy rate by another 25 to 50 basis points.

RAM: RAM Ratings’ view is that the four rate cuts in 2020— amounting to 125 basis points—remain sufficient to support economic activity this year. While the latest PERMAI stimulus package may partly mitigate the impact on near-term growth, further extensions of MCO over the next few months, coupled with a persistently weak global outlook, would heighten the probability of future rate cuts. For now, we have maintained our OPR forecast at 1.75% for the year, with a downside bias given growth uncertainties and muted inflationary pressures. We believe BNM will instead employ more targeted monetary easing measures to sustain economic recovery.

KAF: Current monetary policy remains accommodative for the economy. Although there is still some room for further easing amid high real policy rates, this room is eroding with inflationary expectations building up on the back of climbing commodity prices. We expect the Central Bank to maintain the policy rate at the current level of 1.75% throughout 2021 before it begins hiking rates in early 2022.

- FE: Deteriorating government debt metrics were behind Fitch Ratings’ decision to downgrade Malaysia’s credit rating. Do you expect other agencies to go down the same path? What would be the impact of further rating downgrades on the economy

KIB: Yes, other agencies may do the same. However, a downgrade is not necessarily bad, as the rise in debt is justifiable as we are facing an unprecedented crisis and other countries are also concurrently being downgraded. But it is important that we firm up fiscal consolidation efforts as soon as the economy recovers

RAM: Rating downgrades on Malaysia’s sovereign rating would increase its (and any government-linked entities’) cost of funding, making it more expensive to borrow. There may also be foreign investors who may not be able to invest in lower-rated debt, hence it may affect their participation in government securities. However, as the track record indicates, domestic institutions have been able to mitigate any external demand shortfall due to the country’s large pool of domestic savings. Other impacts on the external front are marginal given the limited exposure to foreign debt funding for both government and private sectors

KAF: It won’t be a major surprise if other agencies follow suit in rerating Malaysia. The impact would mainly be felt on the fixed income market in the form of accelerated outflows as investors rebalance portfolios and the subsequent effect on the MYR currency. However, the adverse impact on the currency is likely to be cushioned for now by the lingering USD weakness, low global interest rates and rising oil prices.

- FE: What is your outlook for the external sector this year and next?

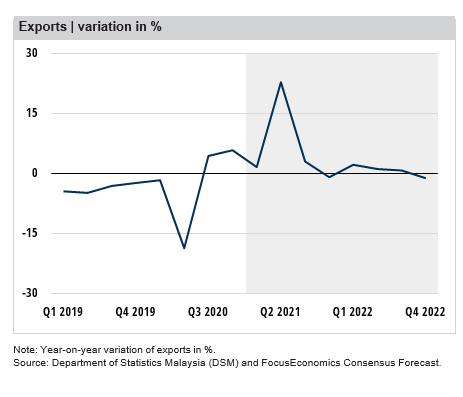

RHB: Two factors support Malaysia’s strong exports recently: Electrical & electronics (E&E) is on an upcycle, and strong palm oil exports. The E&E segment should last longer due to strong demand for mobile communications and the internet of things; however, palm oil prices could come down from recent highs as supply constraints ease. As a result, expect exports to be more normalized in the coming quarters.

KAF: The external sector […] has been surprisingly resilient and is held up by strong demand for electronics and medical- related products such as rubber gloves, and optical & scientific equipment. We think these sectors will continue to expand going forward and will be aided further by a recovery in commodity exports such as palm oil, crude oil and LNG. We expect export performance to return to positive territory and expand 6.0% and 4.5% in 2021 and 2022 respectively compared to -1.4% in 2020, in tandem with the recovery in the global economy.

KIB: I remain optimistic on the external sector, mainly due to the technology upcycle (cloud infrastructure services, laptops, electric vehicles, smartphones, etc.), underpinned by the 5G-related demand and rising trend of working and studying from home. The expected rebound in global commodity prices and greater fiscal spending by the U.S. government would also support external demand.