Why is Eastern Europe Poorer Than The West?

The economic gap between Western and Eastern Europe isn’t the result of a single bad decade; it’s a complex cocktail of history, geography, and some very different approaches to running a country. While the East is catching up at a blistering pace, the “Great Divide” remains visible. Below are the key factors at work.

The Long Shadow of Imperialism and Industrialization

Long before the 20th century, Western Europe held a massive head start. Nations like Britain, France, and the Netherlands leveraged early industrialization and colonial empires to accumulate vast amounts of capital. While the West was building factories and global trade networks, much of Eastern Europe remained agrarian and feudal, often acting as a “breadbasket” for the West. This historical lag meant that when the modern era arrived, Western Europe already had the infrastructure, banking systems, and merchant classes that Eastern Europe was only beginning to develop.

The Communist Experiment and Central Planning

The most significant divergence occurred after World War II. While the West benefited from the Marshall Plan and embraced market capitalism, the East fell behind the Iron Curtain. For four decades, command economies replaced market signals with state-mandated quotas. This led to massive inefficiencies: resources were misallocated to heavy industry rather than consumer goods, and the lack of competition stifled innovation. By the time the Berlin Wall fell in 1989, the technological and productivity gap between the two halves of the continent was a chasm.

The “Shock Therapy” of the 1990s

Transitioning from a state-run economy to a free market wasn’t a smooth ride. Many Eastern European nations underwent “shock therapy,” suddenly privatizing state assets and lifting price controls. In many cases, this led to hyperinflation, the collapse of social safety nets, and the rise of powerful oligarchs who snatched up national industries for cents on the dollar. While some countries like Poland navigated this better than others, the initial decade of post-communism was marked by a deep recession that set the region back even further.

Institutional Strength and Corruption

Economic growth relies heavily on “soft infrastructure”—things like the rule of law, property rights, and transparent governance. Western European institutions have had centuries to mature and refine their legal systems. In contrast, many post-Soviet states struggled with institutional “hollowing out,” where corruption and weak legal frameworks deterred foreign investment. When investors fear their assets might be seized or that they’ll have to pay bribes to operate, they take their capital elsewhere, slowing the rate of wealth accumulation.

The Demographic “Brain Drain”

Since the EU enlargement in the 2000s, Eastern Europe has faced a unique challenge: the brain drain. The principle of “freedom of movement” allowed millions of the youngest, brightest, and most motivated workers to move from East to West in search of higher wages. While these workers send home significant remittances, their absence creates labor shortages and a “demographic winter” in their home countries. It is difficult to build a high-tech, high-wage economy when your most skilled engineers and doctors are working in London, Paris, or Berlin.

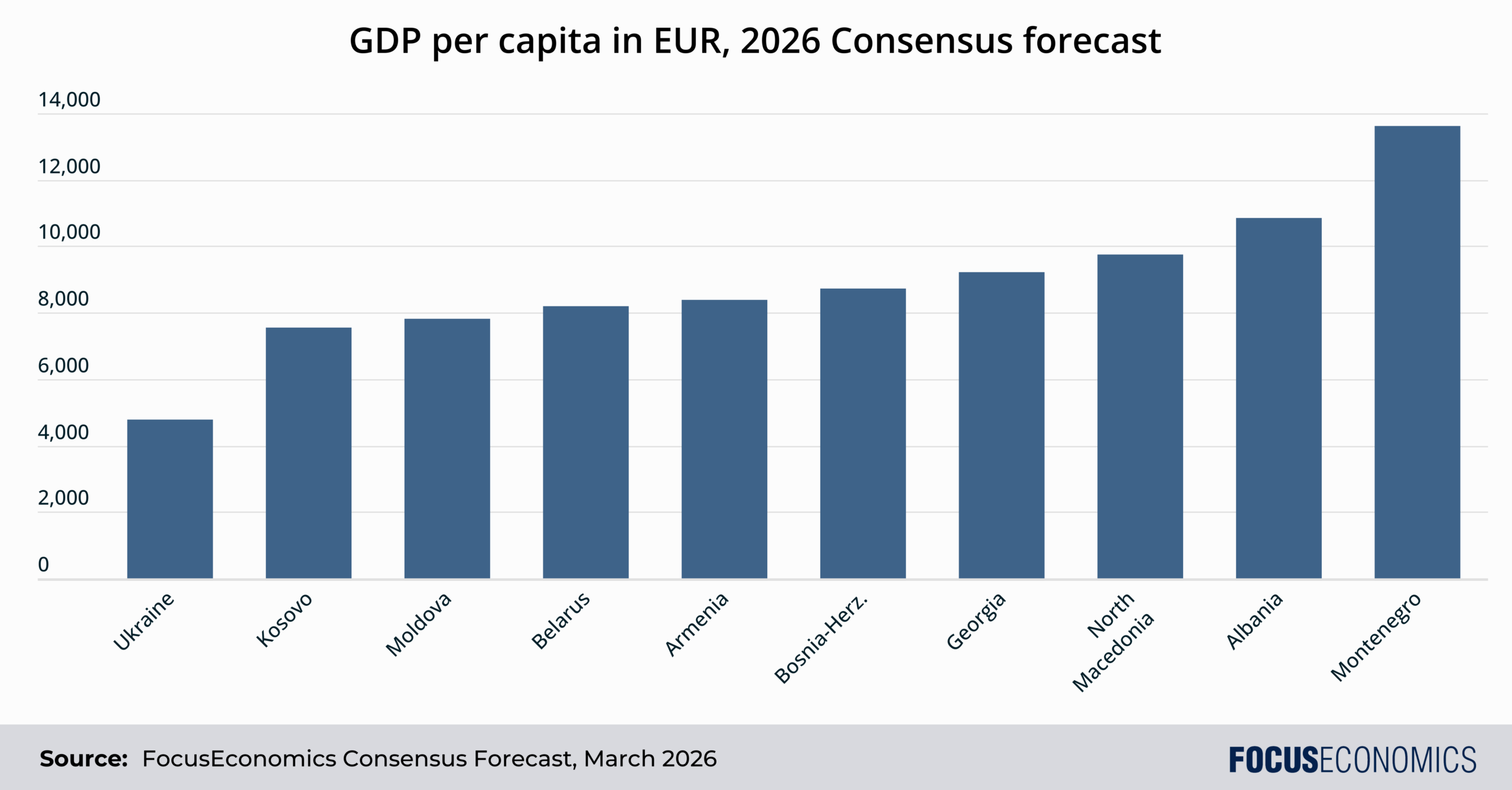

The Top 10 Poorest Countries in Europe by GDP per Capita

1. Ukraine. 2026 GDP per capita Consensus forecast: 4795

Ukraine remains the poorest country in Europe, a status exacerbated by the catastrophic impact of the ongoing Russian invasion. Prior to the war, Ukraine’s economy struggled with a slow transition from its Soviet past and widespread corruption. Since 2022, the destruction of critical infrastructure, particularly in the energy sector, and the displacement of millions of citizens have led to a massive contraction in GDP. Although the economy showed resilience with growth in 2023-2025, the outlook remains precarious as the conflict drags on, stifling private investment, bidding up inflation and leaving the nation heavily dependent on international financial aid.

2. Kosovo. 2026 GDP per capita Consensus forecast: 7559

Kosovo’s economy is hampered by its status as a young state with limited international recognition and a lack of economic diversification. While the country has maintained a resilient average growth rate of around 4% in recent years, it faces severe structural issues, including a youth unemployment rate where roughly one-third of young people are not in employment, education, or training. The economy relies heavily on remittances from its large diaspora and faces persistent challenges such as corruption, a weak rule of law, and an energy sector that is prone to instability.

3. Moldova. 2026 GDP per capita Consensus forecast: 7816

Moldova’s economy is among the most vulnerable in Europe, historically tied to its agricultural sector and deeply impacted by regional instability. The spillover effects of the war in neighboring Ukraine have caused severe energy shocks and disrupted trade routes, leading to stagnant growth in recent years. Despite being granted EU candidate status, the country continues to struggle with low labor force participation, a large state presence in the economy, and a significant brain drain as younger workers emigrate for better wages in Western Europe.

4. Belarus. 2026 GDP per capita Consensus forecast: 8195

The Belarusian economy is characterized by heavy state control and an increasing dependence on Russia following international sanctions imposed after the 2020 political crisis and the country’s role in the Ukraine conflict. While the government has used price controls and directed lending to maintain artificial stability, these measures have led to supply-side bottlenecks and labor shortages. Belarus’ ICT sector, once a bright spot for the economy, has contracted significantly as professionals and firms have fled the country, leaving the nation’s growth prospects tied to the volatile Russian market.

5. Armenia. 2026 GDP per capita Consensus forecast: 8401

Armenia’s economy has recently experienced a period of robust GDP growth. The economy expanded 46% between 2020 and 2025, driven by a surge in trade, construction, and services following the influx of Russian migrants and capital. However, this growth is expected to moderate as these temporary tailwinds dissipate. The country’s landlocked geography and closed border with Azerbaijan remain significant long-term hurdles to trade diversification. Furthermore, regional geopolitical uncertainty continues to weigh on investor sentiment and the nation’s long-term fiscal stability.

6. Bosnia-Herzegovina. 2026 GDP per capita Consensus forecast: 8733

Bosnia-Herzegovina’s economy is stifled by one of the most complex governance systems in the world, which creates a fragmented and inefficient market. Frequent political deadlocks and ethnic tensions deter foreign direct investment and delay necessary structural reforms. The economy suffers from a bloated public sector that crowds out private enterprise and a high rate of out-migration, particularly among skilled workers. As a result, the country remains far from achieving income convergence with the European Union.

7. Georgia. 2026 GDP per capita Consensus forecast: 9206

Georgia has historically been a reformer in the region, but recent political instability and a stalled EU accession process have clouded its economic outlook. While Georgia’s economy has boomed since the pandemic thanks to an influx of Russian people and trade amid Russia’s war against Ukraine, businesses face significant challenges, including a major skills gap and workforce shortages that are estimated to cost the country a significant portion of its potential GDP. Currency fluctuations and concerns over the rule of law continue to challenge financial planning and deter the high-quality foreign investment needed for long-term development.

8. North Macedonia. 2026 GDP per capita Consensus forecast: 9732

North Macedonia’s economy over the past decade has been characterized by steady, moderate growth, hindered periodically by political uncertainty and structural bottlenecks. While the resolution of long-standing naming disputes bolstered investor confidence and facilitated NATO accession in 2020, the delayed path toward EU integration has tempered the expected inflow of large-scale foreign capital. Growth has been primarily driven by the automotive manufacturing sector within Technological Industrial Development Zones (TIDZ) and, more recently, by intensive public investment in major infrastructure projects like Corridors 8 and 10d. However, the economy remains vulnerable to external demand shocks from the Eurozone and faces a critical long-term headwind in the form of demographic erosion; the persistent “brain drain” of skilled labor has led to significant shortages.

9. Albania. 2026 GDP per capita Consensus forecast: 10837

Albania’s economy has benefited from a recent tourism boom, which has helped push output above pre-pandemic levels and supported average GDP growth of 4% from 2022 to 2025. Despite this positive momentum, the country remains one of Europe’s poorest due to low productivity and a rapidly aging population. Mass emigration has led to labor shortages in key sectors, while the economy’s reliance on informal work and narrow diversification leaves it vulnerable to external shocks and climate-related risks to its agricultural and energy sectors.

10. Montenegro. 2026 GDP per capita Consensus forecast: 13616

Montenegro’s economy is heavily reliant on the tourism and services sectors. Moreover, the country faces a significant current account deficit, largely driven by its dependence on imports for energy and manufactured goods. While Montenegro is a frontrunner for EU membership, its high levels of public debt and the need for fiscal consolidation present ongoing challenges to ensuring that its economic growth is sustainable and inclusive across its less-developed northern regions.

What factors have driven Eastern Europe’s economic convergence with Western Europe?

Though Eastern Europe remains on the whole notably poorer than Western Europe, there’s good news: The gap between East and West is shrinking. In the last few decades Eastern European nations have maintained much higher average growth rates—often doubling or tripling the GDP growth of their Western neighbors. Convergence is in some instances already complete: Countries like Estonia and the Czech Republic now boast higher GDP per capita (PPP) than some of their Southern European neighbors. Below are the key factors at work.

EU Accession

The accession of 11 Central and Eastern European (CEE) countries to the EU between 2004 and 2013 has been the primary catalyst for convergence—evident in the fact that all ten of the poorest countries in Europe today are not members of the EU. Membership removed trade barriers, allowing Eastern factories to become integral parts of Western supply chains. For example, the automotive industry in Slovakia and Czechia became a “hinterland” for German manufacturers, benefiting from seamless logistics and zero tariffs. This “integration model” allowed the East to export its way to wealth, with trade openness (exports + imports as a % of GDP) reaching over 150% in countries like Slovakia.

Massive Foreign Direct Investment (FDI) in Eastern Europe

Western companies, particularly from Germany, Austria, and France, poured billions into the East to capitalize on a skilled but lower-cost labor force. Unlike “hot money” that can leave quickly, this was greenfield investment—building physical factories, research centers, and service hubs. Between 2004 and 2023, the net capital stock in CEE countries surged, bringing with it advanced technology and managerial expertise that boosted local productivity.

EU Cohesion and Structural Funds

The EU’s “Cohesion Policy” acts as a massive wealth redistribution mechanism. Since 2004, hundreds of billions of euros have been transferred from wealthier net contributors (like the Netherlands) to poorer regions in the East to fund infrastructure, R&D, and human capital. In many Eastern European nations, these funds account for 3% to 4% of annual GDP.

Rapid Productivity Gains

Eastern Europe started the 1990s with highly inefficient, state-run industries but generally skilled workforces. The transition to a market economy allowed for “low-hanging fruit” productivity gains. By adopting Western technologies—a process called technological catch-up—Eastern workers became dramatically more efficient. While labor productivity growth in the Euro area has hovered around 1% in recent years, Eastern European countries have tended to do much better. For instance, from 1996 to 2023, productivity growth in Poland averaged over 3% per annum, allowing wages to rise without triggering unsustainable inflation.

Institutional Reform and the Rule of Law

To join the EU, Eastern nations have to adopt a massive body of EU law that harmonizes everything from property rights to food safety standards. The process of adopting this law reduces risk for investors and creates a stable environment where businesses can plan ahead—even before a country joins the EU.

The Economic Outlook for Europe’s Poorest Countries

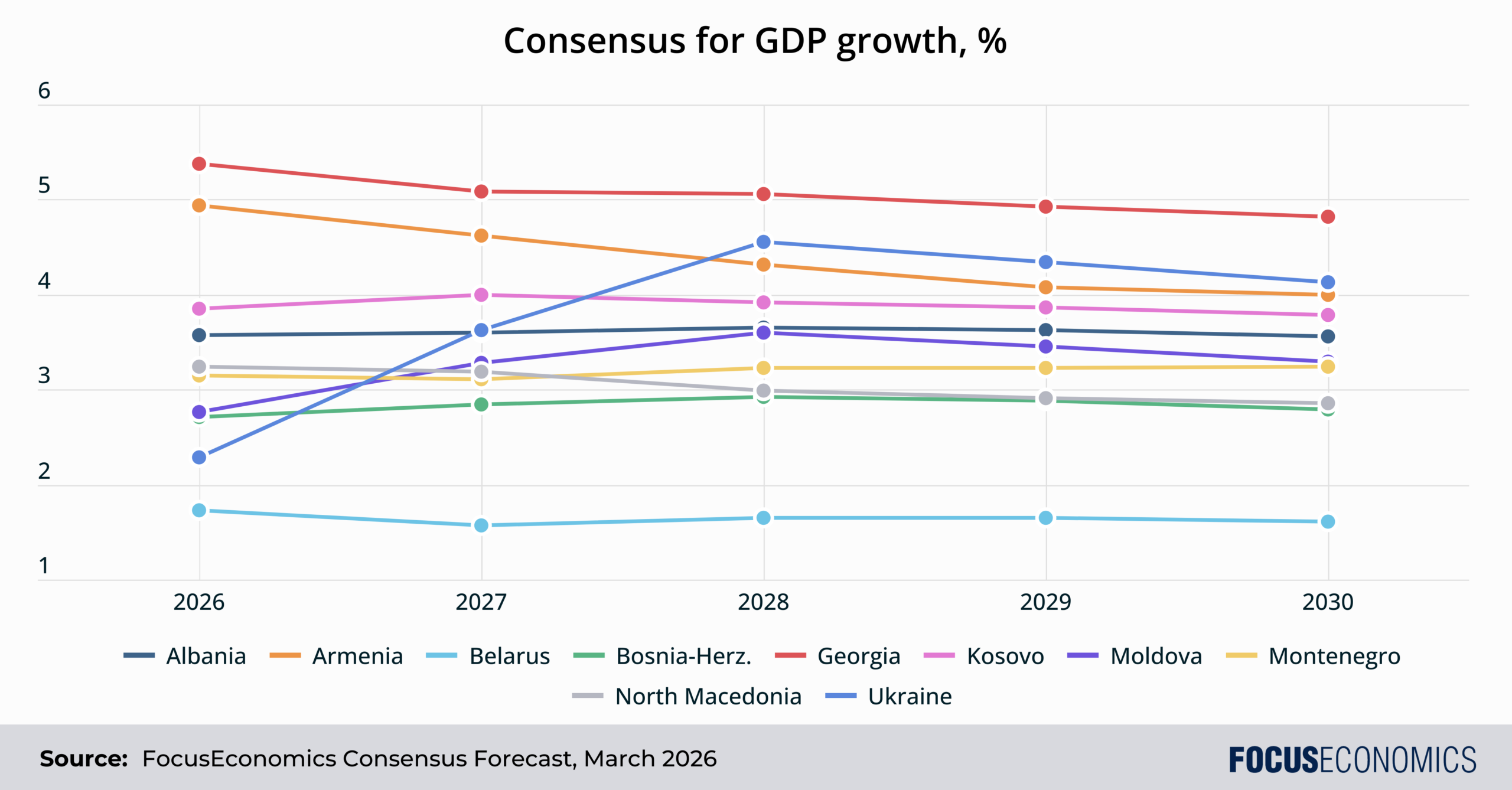

The Consensus among our panelists is for the ten poorest countries in Europe to grow on average over twice as fast as the Euro area for the rest of this decade, indicating income convergence with wealthy Western European nations. Growing tourism, EU investment and structural reforms linked to EU membership ambitions will be key drivers. On EU membership, the candidacies of Albania and Montenegro are the most advanced, with possible accession to the bloc by 2030. Late last year the European Commission also singled out Moldova and Ukraine for praise—though the latter is unlikely to join as long as the war with Russia drags on.

That said, panelists forecast a large discrepancy among countries. At one end of the spectrum is Georgia, which will likely benefit from capital inflows from Russia, Turkey and China even as Georgia’s EU ambitions are put on ice. At the other is Belarus, where economic activity will be weighed on by international isolation and weak rule of law.

In sum, Europe’s poorest countries currently have income levels that are a fraction of those in the West. But if current trends continue, things in most Eastern European countries are unlikely to stay that way forever.