Capitalism does not move in a straight line. It advances, stumbles, overreaches, corrects and starts again. Economies expand as firms hire, consumers spend and investors grow bold. Then something changes. Profits are squeezed, credit tightens, demand cools or confidence cracks. Output slows. Jobs disappear. Asset prices fall. Policymakers intervene. Eventually the conditions for recovery are laid down, and the machine begins to whirr again.

This pattern is known as the economic cycle, or more narrowly the business cycle: The recurring movement of an economy between expansion and contraction. Yet the classic business cycle is now under strain as an explanatory device. Modern economies are more service-heavy, more globalized, more financialised and more aggressively managed by central banks and governments than the industrial economies from which the theory of the classic economic cycle emerged. Recessions still occur. Booms still intoxicate. But the old rhythm of inventory-led expansions and corrections has become harder to detect.

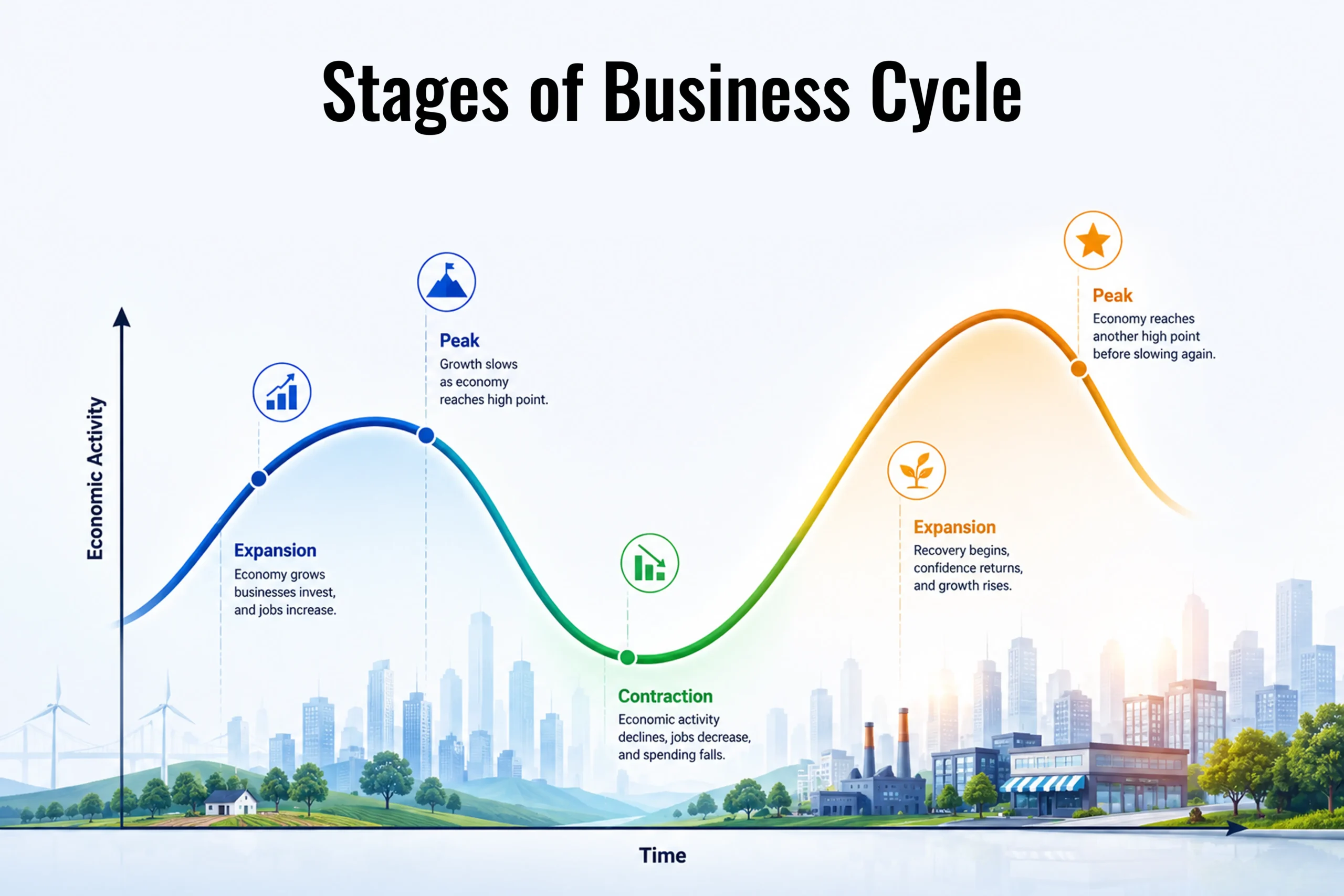

The Anatomy and Stages of the Traditional Business Cycle

The traditional business cycle describes fluctuations in total economic activity around a long-term growth trend. The trend is the economy’s underlying capacity: Its labour force, capital stock, technology and productivity. The cycle is the economy’s deviation from that path. When output rises above sustainable capacity, inflationary pressure tends to build. When it falls below capacity, unemployment rises and spare resources accumulate. This framework is usually split into four phases: Expansion, peak, contraction and trough.

Explaining the Business Cycle: The Four Core Phases

- Expansion: Output rises, unemployment falls and incomes grow. Firms see stronger demand and respond by hiring workers, extending shifts and investing in new capacity. Banks become more willing to lend, because defaults are low and collateral values are rising. Consumers feel richer and spend more freely, especially on discretionary goods such as cars, vacations and home improvements. Governments benefit from higher tax receipts and lower welfare costs.

- Peak: Peaks aren’t always obvious at the time. Indeed, they often feel like triumphs. Employment is high. Profits are strong. Headlines are cheerful. Politicians claim credit. Yet beneath the surface, imbalances have usually formed. Inventories may be too large. Companies may have borrowed on the assumption that cheap financing will last forever. Inflation may be forcing the central bank to raise interest rates.

- Contraction: Demand weakens. Firms cut production, cancel investment and slow hiring. Some shed workers. Consumers, seeing weaker labor markets and falling asset prices, become cautious. Banks tighten lending standards. Risk appetite retreats. What began as a slowdown can become self-reinforcing: Lower spending reduces revenue; lower revenue prompts layoffs; layoffs reduce income; lower income reduces spending further. A contraction becomes a recession when the decline in activity is broad, persistent and material. The common shorthand is two consecutive quarters of falling real GDP, but that rule is crude. A serious recession is visible across many macroeconomic indicators: Output, employment, industrial production, real income, retail sales and credit conditions.

- Trough: This is the bottom of the cycle, when activity stops deteriorating and the conditions for recovery emerge. Inventories have been run down. Weak firms have exited. Interest rates may have fallen. Governments may have loosened fiscal policy. Consumers who postponed purchases begin to spend again. Firms discover that demand is no longer getting worse. The trough, like the peak, is usually identified only after the fact. It rarely feels like a turning point when one is living through it. It feels like exhaustion.

Traditional Drivers: What Causes Business Cycles to Shift?

For centuries, economists have debated the primary recession triggers that push an economy from boom to bust. In the traditional framework, three primary forces dictate the rhythm.

- The Price of Money and Credit Cycles: Capitalism runs on credit, and the cost of that credit is the single most powerful lever in the economy. When interest rates are low, borrowing is cheap. A business can easily justify taking out a loan to build a new facility if the cost of debt is 3%, but that same project becomes unprofitable if debt costs 8%. Consumer spending is similarly tethered to credit via mortgages, auto loans, and credit cards. Therefore, the expansion and contraction of credit, often orchestrated by central banks but amplified by commercial retail banks, is the primary engine of the cycle. Expansions are fuelled by credit creation; recessions are triggered by monetary tightening and credit contraction.

- The Inventory Bullwhip Effect: Before the advent of modern software, economies were heavily reliant on manufacturing and physical goods. This gave rise to the inventory cycle. When consumer demand rises slightly, retailers order more from wholesalers to avoid running out of stock. Wholesalers, in turn, order even more from manufacturers to ensure they have a buffer. Manufacturers ramp up production, hire workers, and buy raw materials. This creates a boom. However, once consumers stop buying, retailers abruptly cancel orders. Manufacturers are suddenly left holding stockpiles of unsold goods. They shut down assembly lines and lay off workers, triggering a recession. This amplification of small demand shifts into massive production swings is known as the bullwhip effect.

- Psychology and Exogenous Shocks: Human emotion cannot be quantified in an economic model, but it drives the cycle. In a boom, the fear of missing out overrides basic risk management. In a bust, the instinct for self-preservation overrides logical investment opportunities. Beyond psychology, traditional cycles are often violently shifted by exogenous shocks: events outside the financial system. A sudden geopolitical conflict that spikes oil prices can instantly drain consumer spending power, artificially inducing a recession regardless of where the credit cycle currently sits.

Examples Of Past Cycles That Fit The Traditional Mould

To see these mechanics in action, one need only look at the macroeconomic history of the late 20th and early 21st centuries.

- The 1981-1982 Volcker Recession: This was a classic, policy-induced contraction. By the late 1970s, the United States was suffering from stagflation: stagnant growth combined with high inflation. To break the psychology of perpetual price increases, Federal Reserve Chairman Paul Volcker aggressively hiked the federal funds rate to nearly 20%. The medicine worked, but the side effects were unpleasant. The exorbitant cost of capital crushed the housing and manufacturing sectors. Unemployment soared to double digits. It was a textbook example of a central bank deliberately triggering the contraction phase to purge inflation, resetting the board for the massive expansion of the 1980s.

- The 1990-1991 S&L Crisis Recession: Following the boom of the 1980s, the U.S. and global economies succumbed to a classic credit and real estate hangover. Deregulation had allowed Savings and Loan (S&L) institutions to aggressively lend to commercial real estate developers. When the Federal Reserve raised rates to cool the overheating economy in 1989, property values dropped. The S&Ls collapsed under the weight of bad loans. Credit froze, businesses could not roll over their debts, and consumer confidence plummeted, leading to a brief but sharp traditional recession.

- The 2001 Dot-Com Bust: The late 1990s provided a flawless demonstration of Keynesian animal spirits. The advent of the internet triggered a massive wave of capital investment into telecommunications and technology companies. Valuations decoupled from reality as investors threw billions at companies with no revenue, let alone profit. When the euphoria broke in early 2000, the capital taps were abruptly shut. Some telecom and tech companies went bankrupt, massive capital investments were written off, and the resulting wealth destruction bled into the broader economy, triggering a recession led almost entirely by burst asset bubbles and corporate overinvestment rather than consumer exhaustion.

Do Economic Cycles Still Exist in the Modern World?

If you trace the data from the mid-19th century through the mid-20th century, recessions were incredibly frequent. The U.S. economy spent roughly a third of its time in a state of contraction. Yet, as we move into the 21st century, the large swings of the economic pendulum appear to be slowing down.

Economists in the early 2000s proudly proclaimed the arrival of the “Great Moderation”: an era where enlightened monetary policy and structural economic shifts had supposedly tamed the violent business cycle forever. While the devastating 2008 Global Financial Crisis violently shattered the illusion that severe busts were a relic of the past, the core question remains hotly debated among macroeconomic strategists today: Has the fundamental nature of the economic cycle irrevocably changed? The evidence suggests that while the cycle is not dead, it has mutated into something distinctly less rhythmic and far more artificial.

The Classic Business Cycle Is Becoming Less Relevant

The most glaring evidence that the traditional cycle is breaking down is the sheer duration of modern expansions. Historically, economic expansions lasted roughly four to five years before overheating and triggering a recession. However, recently we have seen more long-wave cycles. The U.S. expansion spanning the 1990s lasted 10 years. The expansion following the 2008 crisis lasted a staggering 128 months (nearly 11 years), the longest in recorded history, only ending because of a literal global pandemic, not an endogenous economic failure.

Furthermore, when recessions do arrive today, they rarely look like the classic inventory-and-credit burnouts of the past. Instead, they resemble sudden, exogenous shocks. The 2020 recession was a government-mandated shutdown of commercial activity. The severe economic pain of 2022 in Europe was driven by an energy shock resulting from the war in Ukraine. We are increasingly experiencing shocks to the system rather than natural cyclical turns.

Additionally, the modern economy is displaying a new phenomenon: The rolling recession. In a traditional cycle, the entire economy sinks together. In the post-pandemic era, we have seen sectors contract in isolation while the broader economy remains afloat. In 2022 and 2023, the technology and real estate sectors experienced contractions, featuring layoffs and falling valuations. Historically, this would have dragged the entire economy into the abyss. Instead, the travel, leisure, and healthcare sectors boomed simultaneously, keeping aggregate GDP growth positive. The syncopation of the cycle is broken.

Why The Business Cycle Is Becoming Less Relevant

Why is the classic sine wave flattening out and distorting? The answer lies in structural shifts in what the global economy produces, and massive changes in how governments and central banks manage it.

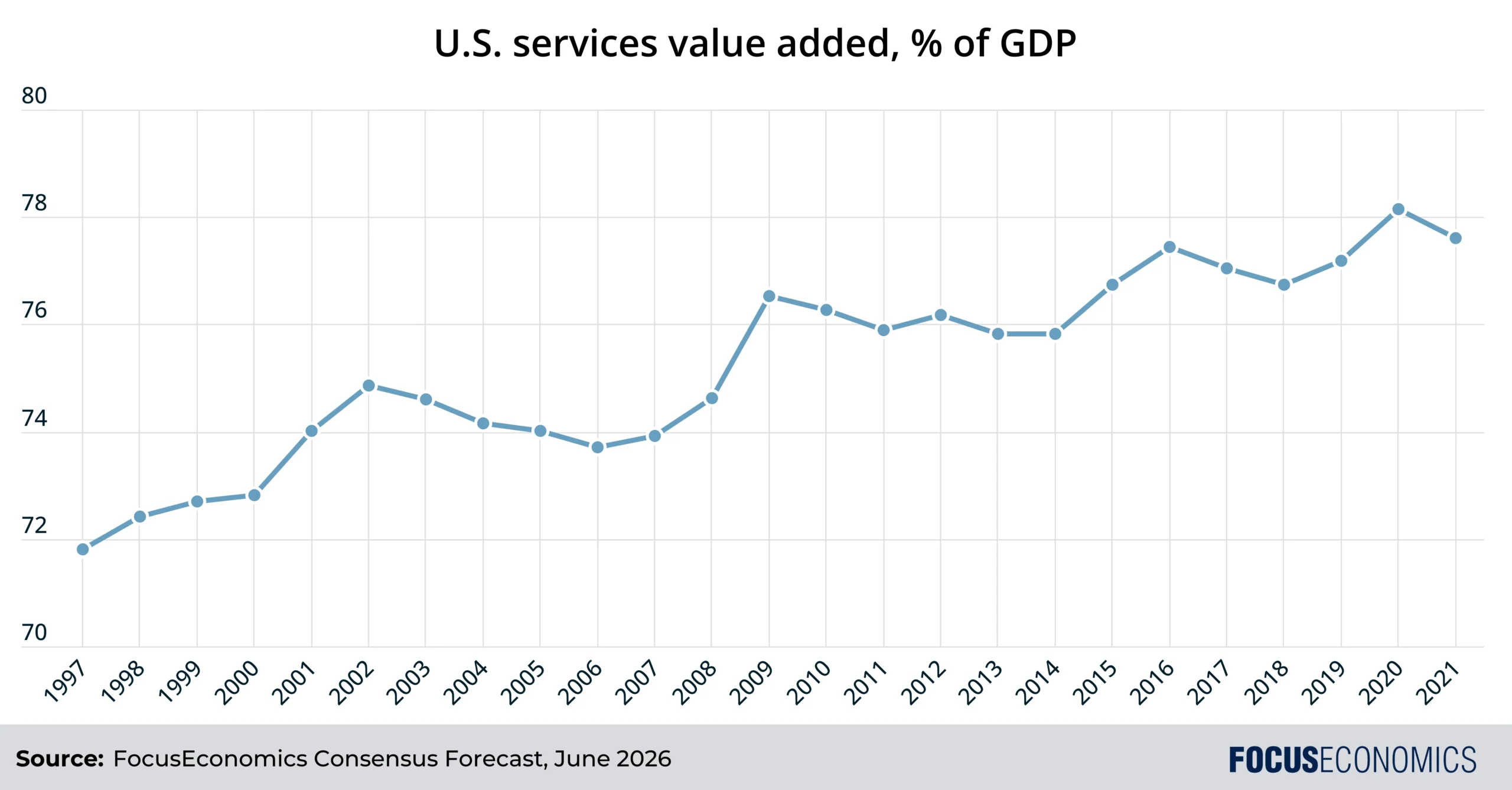

- The Rise of the Intangible Services Economy: The traditional business cycle was built on factories, warehouses, and railcars. If you produce steel or automobiles, a 5% drop in consumer demand creates a massive backlog of physical goods that forces you to shut down operations. Today, advanced economies are overwhelmingly dominated by services and intangible assets: software, consulting, healthcare, finance, and media. You cannot stockpile healthcare, and you do not need an inventory of software algorithms. Because the services sector does not suffer from the violent bullwhip effects of physical inventory, it is inherently more stable. The structural shift away from manufacturing has fundamentally insulated modern economies from the sharpest edges of the classic cycle.

- Omnipotent Central Banks and Active Firefighting: In the past, central banks generally allowed recessions to play out, viewing them as a healthy clearing of the economic throat. Today, central banks suffer from a profound fear of deflation and deep contractions. The moment financial plumbing begins to creak, institutions like the Federal Reserve or the European Central Bank intervene with overwhelming force. The invention of Quantitative Easing (QE), where central banks create money to buy government and corporate bonds, has fundamentally altered the cycle. By artificially suppressing bond yields and flooding the system with liquidity at the first sign of trouble, central banks successfully prevent the harsh cleansing phase of the traditional cycle.

- Fiscal Dominance and the State as Consumer of Last Resort: Historically, when private sector demand collapsed, a recession was inevitable. Today, governments are increasingly willing to step in and replace that lost private demand with public debt. During the 2020 Covid-19 shock, governments did not wait for the cycle to correct; they bypassed the banking system entirely and directly deposited cash into the checking accounts of citizens and businesses. Even outside of crises, the return of massive industrial policy (such as the US CHIPS Act or the European Green Deal) means that governments are constantly injecting hundreds of billions of dollars into specific sectors. When the state accounts for such a massive, price-insensitive portion of aggregate demand, the traditional market signals of the business cycle are inevitably muffled.

- Data and Just-In-Time Supply Chains: Finally, the sheer velocity of modern data has neutered the classic inventory cycle. In the 1970s, a retailer might not know they were overstocked until the warehouse was full. Today, sophisticated software tracks inventory at the barcode level in real-time. Corporations order dynamically, maintaining “just-in-time” supply chains. While this fragility was briefly exposed during the pandemic supply chain disruptions, under normal conditions, it prevents the massive, slow-moving inventory gluts that historically triggered deep recessions.

Summing Up

The economic cycle is not dead. The laws of supply, demand, and human folly guarantee that booms and busts will persist as long as capitalism does. However, the traditional, rhythmic heartbeat of the 20th-century business cycle has been irrevocably altered. Muffled by central bank interventions, stabilized by the service economy, and distorted by rolling sector shifts, the modern cycle is a far more complex and entirely less predictable beast.