So far this century, the global economic narrative has been dominated by a symbiotic, if increasingly tense, macroeconomic marriage of opposites. On one side sits the United States, the world’s ultimate consumer of first and last resort. On the other sits China, the world’s unrivaled workshop and capital-formation machine. This division of labor has shaped global trade flows, dictated the path of interest rates, and determined the geopolitical balance of power. However, this structural division is no longer functioning smoothly. As both superpowers face internal structural limits and external frictions, the viability of their respective economic architectures is under intense scrutiny.

Contrasting the Structural Types of Economies

To understand the friction between consumption- and investment-led models, one must first look at the composition of GDP as captured in the national accounting identity:

GDP = C + I + G + (X – M)

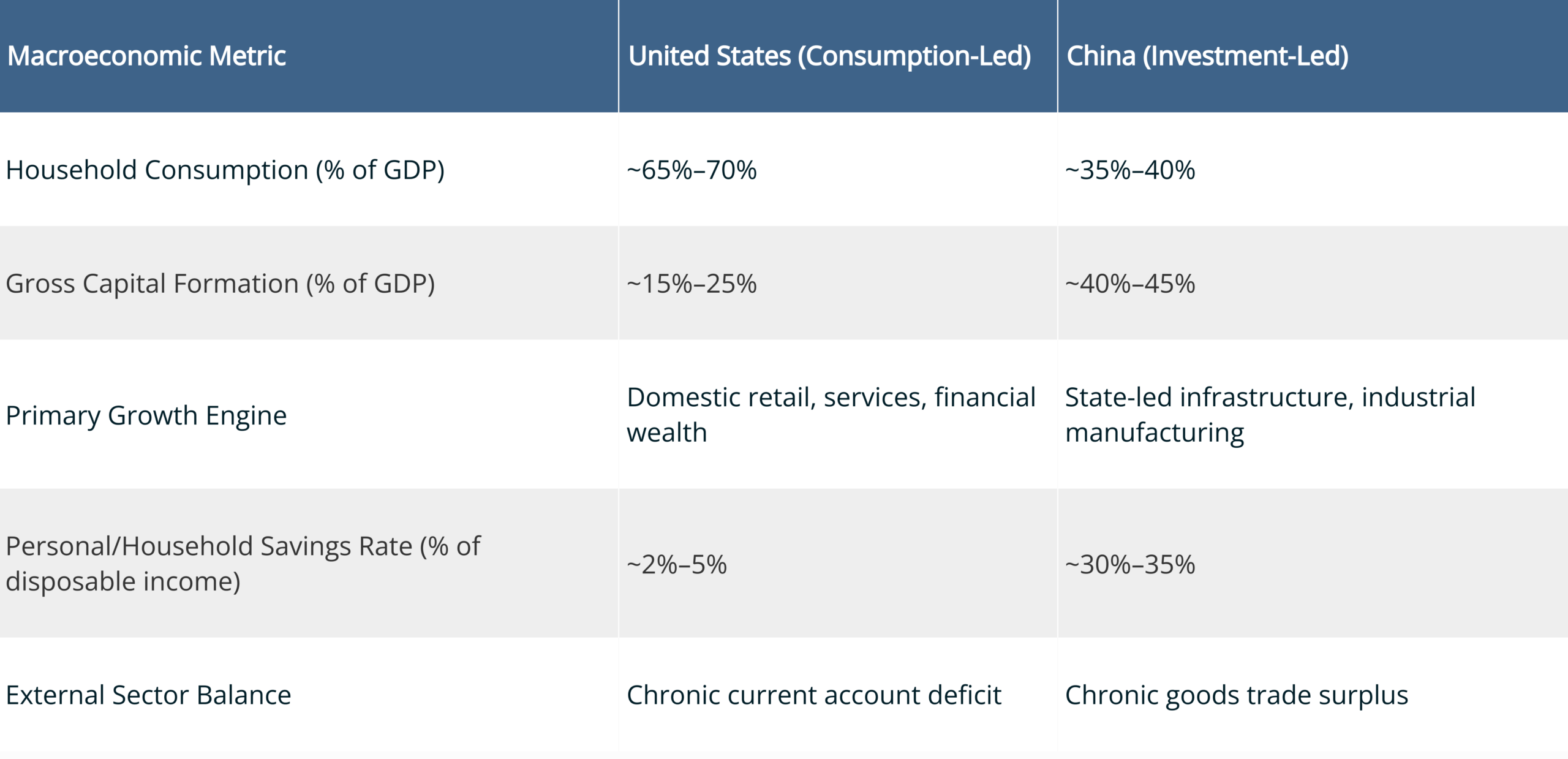

Where C represents private consumption, I is investment, G is government spending, and (X – M) represents net exports. While every modern nation requires a balance of these components, the U.S. and China have pushed their systems to diametrically opposed configurations, as the table below demonstrates.

The U.S. Model: Mechanics of a Consumer-Driven Economy

The U.S. economy’s consumption-led model is supported by several institutional mechanisms:

- Deep Financialization and Easy Credit: Unlike societies where citizens must save cash for major purchases, the U.S. financial system specializes in turning future earnings into present-day demand. Mortgages, credit cards, auto loans, and securitization structures allow American households to maintain a high marginal propensity to consume.

- The Global Reserve Currency Advantage: Because the U.S. dollar retains its global hegemony, the United States can run persistent current account deficits without triggering a classic currency collapse. Foreign central banks and investors have historically recycled their dollar surpluses back into U.S. Treasuries, lowering domestic borrowing costs and subsidizing American consumer demand.

- The Wealth Effect: American household balance sheets are deeply linked to asset markets. Around three fifths of American households own stocks, and a slightly higher proportion own their own homes. As a result, when the S&P 500 or home equity increases—which both have done significantly over the past decade—consumers feel wealthier and increase their spending, even if their real wages remain flat. This creates a self-reinforcing loop where asset price inflation directly stimulates real economic growth.

The primary characteristic of this model is its demand-pull nature. Production follows consumption. Capital is allocated primarily by market forces toward sectors that promise the highest near-term returns. In recent decades this has tended to favor services, technology, and consumer experiences over heavy industry or physical infrastructure, though currently a shift is underway towards data centers and other large physical assets to power the AI boom.

The China Model: Investment-Led Economic Development

In sharp contrast, the Chinese economy’s architecture is built from the supply side up. Gross capital expenditure (I) consistently commands over 40% of China’s GDP—a proportion roughly double that of the United States and unprecedented among major economies at China’s stage of development. Conversely, private household spending languishes at a level over twenty percentage points below that of the U.S. as a share of total output.

Beijing’s leadership appears ideologically resistant to Western-style consumerism, viewing large-scale cash transfers to households as unproductive welfare spending. The state has actively avoided a large economic rebalancing towards consumption. As such, the economy’s structural orientation is not merely an accidental byproduct of cultural thrift; it is the deliberate result of systemic institutional design. Key features include:

- Financial Repression and Capital Channeling: For many years, China’s state-dominated banking system capped deposit rates and repressed household savers’ returns, helping banks provide low-cost credit to favored borrowers, including SOEs and local-government financing vehicles. This acted as a hidden tax on households, transferring wealth from savers to industrial and infrastructure sectors.

- The Local Government Growth Machine: Local officials in China have historically been evaluated based on nominal GDP targets. Lacking broad property tax tools, they utilized Local Government Financing Vehicles (LGFVs) to borrow heavily against land values, driving massive investments in roads, high-speed rail, urban housing, and industrial parks.

- Industrial Subsidies and Supply-Side Support: Rather than distributing significant direct financial support to households to boost consumption, the state provides comprehensive supply-side subsidies. These include cheap land, subsidized electricity, tax rebates for exporters, and directed state bank credit aimed at achieving dominance in strategic manufacturing sectors.

China’s model thus prioritizes capital accumulation over immediate welfare optimization. The system is designed to build capacity first and worry about demand later, creating a peerless manufacturing apparatus that relies heavily on foreign markets to absorb its excess production.

Pros and Cons: Growth Prospects of Each Model

Neither system holds a monopoly on economic virtue. Each possesses distinct structural advantages that can drive rapid growth under the right conditions, yet both harbor internal imbalances that threaten long-term stability.

Advantages and Disadvantages of Consumption-Driven Growth

The main strength of the U.S. consumption-led model is its demand responsiveness. Because growth is anchored in household spending and relatively decentralized capital markets, firms receive fast feedback about what consumers value, allowing capital and labor to shift toward sectors with genuine end-market demand. This makes the economy flexible, innovative and less prone to prolonged economy-wide overcapacity than an investment-led model that can continue building capacity even after returns have begun to fall.

However, there are several disadvantages:

- Low National Savings: The U.S. relies heavily on foreign capital to fund its domestic investment needs. This isn’t necessarily a problem as long as that capital is forthcoming, but could become so if international appetite for U.S. assets ever wanes.

- Underinvestment in Fixed Assets: Private capital markets can favor short-term equity buybacks and quarterly dividends over long-term, high-risk capital investments in physical infrastructure, transport networks, and deep-tech manufacturing.

- Wealth Inequality: A consumption model reliant on the wealth effect naturally concentrates gains among those who own equities and real estate. Though most Americans own at least one of these assets, a substantial chunk of the population don’t. The have-nots may thus find their purchasing power eroded by asset-driven inflation, leading to social polarization.

- Deindustrialization: U.S. reliance on consumption has gone hand in hand with offshoring of manufacturing capacity to lower-cost destinations. The resulting job losses in certain communities created a volatile political environment which has fueled populist movements.

- Supply Chain Vulnerabilities: A consumption-led economy that imports many of its goods from abroad is vulnerable to disruptions in the supply of those goods.

Balancing Manufacturing and the Shift Away from Export Led Growth

China’s investment-led system excels at rapid mobilization of capital. When an economy lacks basic infrastructure, an investment-driven model can compress decades of development into a single generation. China has demonstrated this, building world-class transport networks, deep-water ports, and dense industrial supply chains with incredible speed. This supply-side focus has allowed China to become the undisputed global hub for manufacturing, achieving unmatched economies of scale in sectors ranging from basic steel to electric vehicles (EVs).

That said, there are drawbacks:

- Diminishing marginal returns: When an economy lacks roads, building a highway yields massive economic benefits. When it already has advanced infrastructure, building a parallel highway yields negligible returns while adding significant debt.

- Capital Misallocation: The most visible example of this misallocation is China’s real estate crisis, where decades of credit-fueled construction left behind vast inventories of unsold, unoccupied housing. By some estimates, China’s empty or underused housing stock could accommodate several hundred million people.

- Suppressed Domestic Living Standards: Because national income is structurally diverted toward capital formation, Chinese households receive a smaller share of the national economic pie than their peers in Western nations. This under-consumption makes the domestic market too small to absorb the output of its massive industrial base.

What Are The Key Challenges to Each System’s Long-Term Sustainability?

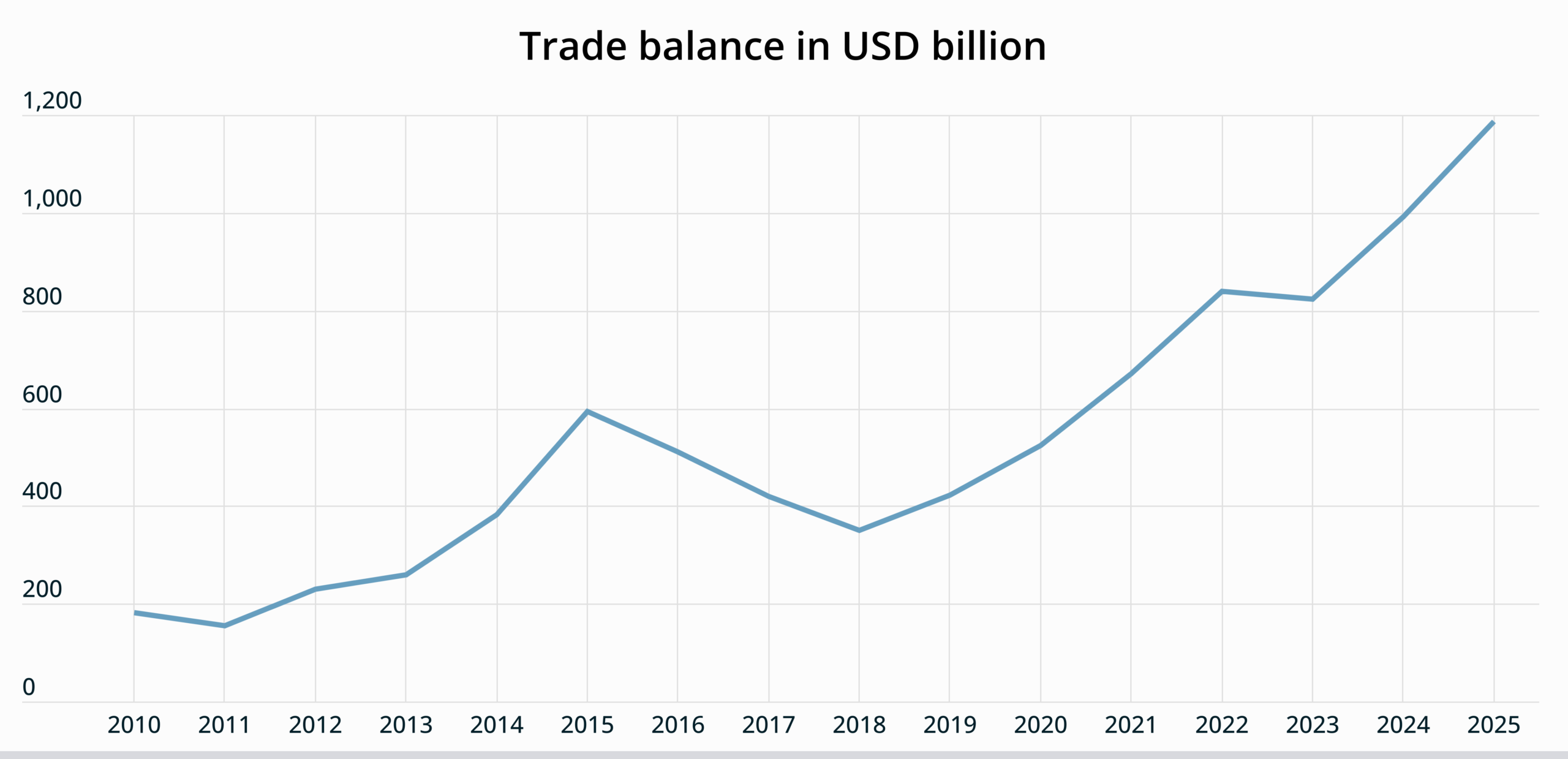

Both countries will face challenges to their economic models in the coming years. China’s main challenge is likely to be rising pushback from other nations over the Asian giant’s vast positive trade balance and increasing export dominance in ever-more areas.

Crucially, it’s not just the U.S. voicing concerns anymore. The European Union has in the last few years opened anti-subsidy investigations and imposed countervailing duties on Chinese goods to protect its domestic industrial base. Moreover, countries like Brazil, India and Turkey have erected trade barriers against Chinese steel, machinery and vehicles to safeguard their own infant manufacturing sectors.

China’s investment-led model thus faces a fundamental mathematical constraint: it cannot continue to sustainably grow its manufacturing capacity faster than other countries are able or willing to absorb it.

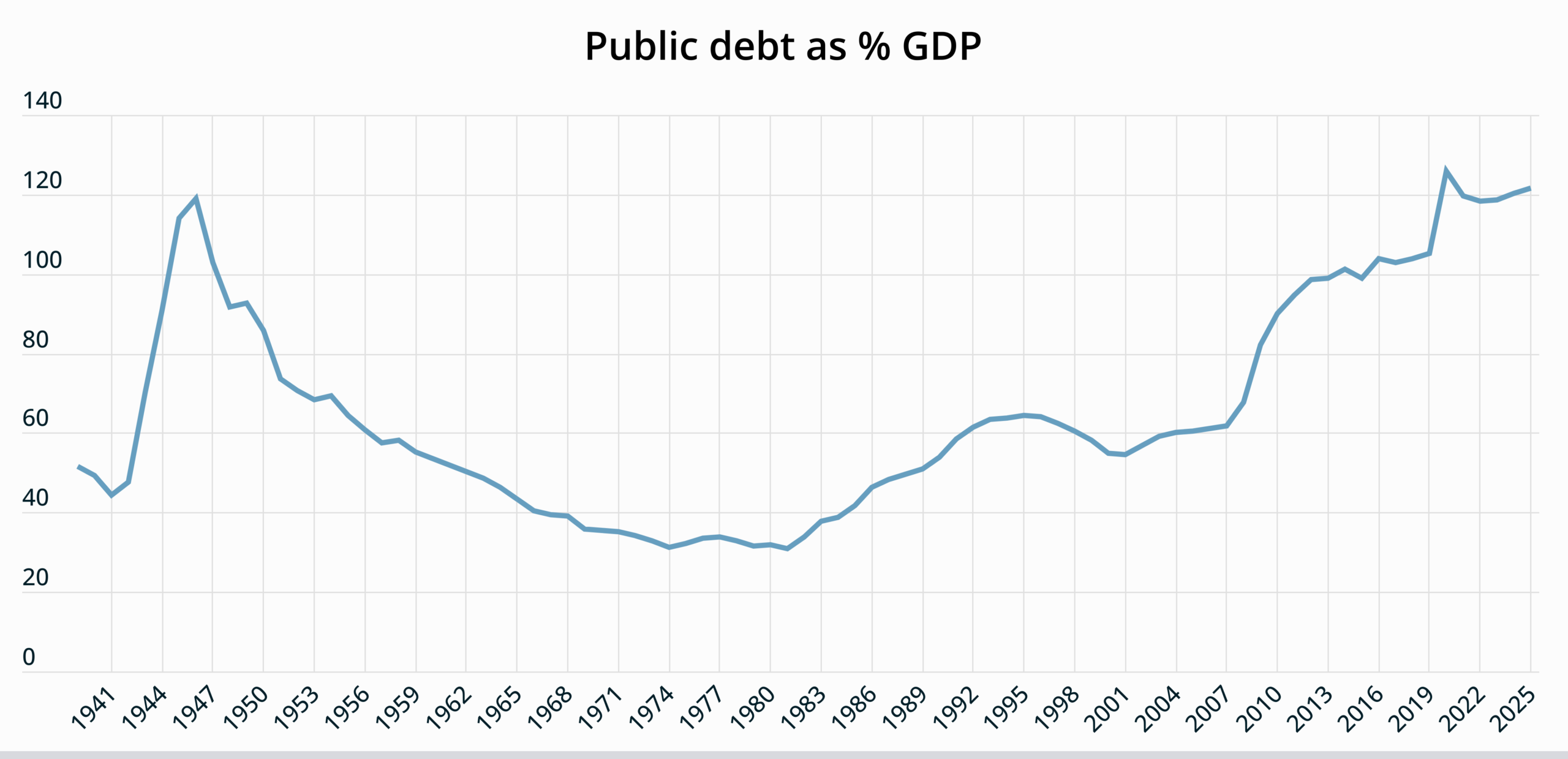

Meanwhile, the key issue facing the U.S. model is arguably debt. The country’s fiscal deficit has been running at over 5% of GDP for the last six years, far wider than the corresponding figure in other G7 economies, and gross federal debt is now over 120% of U.S. GDP—near historic highs. With U.S. consumers and many politicians tax-averse, the government is borrowing to cover the large shortfall between tax receipts and public spending commitments.

While the U.S. government currently has little issue servicing its interest payments or finding borrowers to bankroll it, this might not be the case forever—particularly if the current government continues to chip away at the country’s institutions. Even in the absence of a full-blown collapse in investor confidence, debt servicing costs will still crowd out productive public investments.

What is the Future Outlook for the Two Dominant Global Powers?

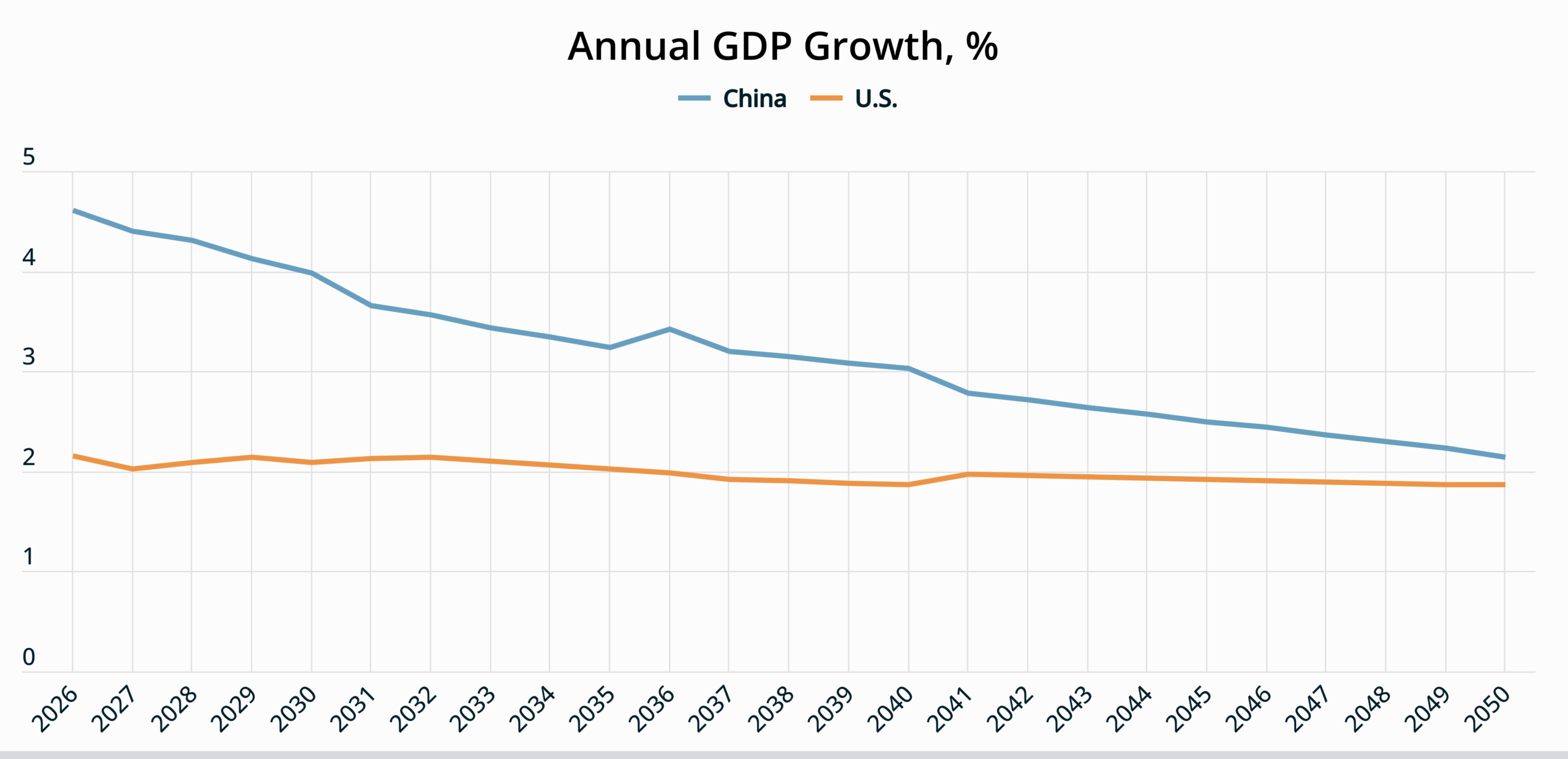

Our long-term Consensus forecasts currently see U.S. GDP growth hovering close to 2% per year over the next few decades—the strongest rate in the G7 and an impressive pace given the country’s already high standard of living and future population ageing. This robust outlook is underpinned by an AI productivity boost, together with the country’s pre-existing strengths such as a flexible labor market, deep capital markets and world-leading research institutions.

In contrast, China’s GDP growth is projected to converge towards the U.S. rate as the Asian giant is held back by an accelerating decline in its population and the exhaustion of large gains from the investment-first economic model.

Several scenarios could flip this narrative. U.S. institutional erosion could eventually reach a point when it begins to weigh substantially on GDP—particularly if the Federal Reserve loses independence or free and fair elections are interrupted. Or, if tech boosters are correct, the current AI boom could cause a jump in the trend rate of U.S. GDP growth in the coming years.

In China, a future change in leadership could potentially herald a break from the current all-out focus on investment towards consumption, with a greater role for private-sector firms. This could keep the country’s economic growth higher for longer, though the overall trend will likely still be downwards as the economy matures and the population drops.

There is also the risk of the two nations clashing over Taiwan. If that were to occur, all bets would be off regarding both countries’ economic trajectories—as well as the future of the wider world.