For the better part of four decades, the story of China’s economy was a simple one to tell. It was a narrative of breakneck speed, an insatiable appetite for steel, and the relentless migration of hundreds of millions from fields to factories. It was the era of the ‘Chinese miracle’. But that story has reached its final chapter. Today, the world’s second-largest economy is attempting to pivot from a model driven by investment and real estate to one powered by high-end manufacturing, green energy, and innovation, the “new quality productive forces”, as President Xi Jinping has referred to them. Navigating this structural transformation is the central challenge for Beijing, with vast implications for the rest of the world.

China’s New Growth Drivers

The Surge in High-Tech Manufacturing and Global Competition

With property no longer reliable as a main engine of growth, Beijing has channeled state credit and administrative might into advanced manufacturing. Success has been especially evident in the ‘New Three’ (xin san yang) sectors key for the green transition: electric vehicles (EVs), lithium-ion batteries and solar photovoltaics, with Chinese exports of these goods having boomed. China now accounts for over half of global EV sales and controls an even more dominant share of the upstream supply chain for batteries. Companies like BYD have transformed from battery manufacturers into vertical integrators capable of undercutting traditional European and American carmakers by thousands of dollars per vehicle.

Success in these sectors is the product of sustained state subsidies, cheap land and energy, targeted lending from state-owned banks, as well as fierce competition spurring innovation and cost reductions. For Beijing, the goal is not merely growth, but strategic autonomy. By dominating the technologies of the green transition, China aims to make the rest of the world reliant on its supply chains, flipping the script on Western attempts at ‘de-risking’.

However, this model carries a distinct risk: Domestic overcapacity. Because consumer demand in China remains tepid, much of this industrial output must find markets abroad. This is driving a second ‘China shock’ in global manufacturing. While the first shock in the 2000s hollowed out low-end manufacturing in the West, this new wave targets high-value, high-skill industries that form the core of advanced economies.

Global Trade Relations: Navigating Tensions with the U.S., Europe, and Emerging Markets

China’s industrial strategy is on a direct collision course with the trade policies of its largest trading partners. The relationship with the United States has transitioned from a trade war into a broader geoeconomic struggle. Washington has moved from broad tariffs to a ‘small yard, high fence’ approach, blocking China’s access to advanced semiconductors and chip-making equipment. This has forced Beijing to pour resources into domestic alternatives, with mixed success. While local champions like Huawei have shown remarkable resilience, the cutting edge of semiconductor physics remains largely out of China’s reach, for now.

Europe, meanwhile, finds itself caught in a painful bind. The continent is deeply reliant on Chinese supply chains for its green transition but fears that its own automotive and industrial base will be obliterated by state-subsidized Chinese competition. The EU’s stance has hardened, shifting from viewing China as a partner to a systemic rival. Brussels is now actively utilizing trade defense instruments, a move Beijing views as pure protectionism masked as fair play.

In response to these rising trade tensions in the West, China is aggressively cultivating commerce with emerging markets. Trade with ASEAN nations and countries along the Belt and Road Initiative has surged. China is exporting not just finished goods but the machinery and components needed for these nations to build their own industrial bases.

Yet, even here, tensions are brewing. Emerging economies from Latin America to Southeast Asia are raising tariffs on Chinese steel and chemicals, realizing that unchecked imports could smother their own nascent industries before they can take root.

Expect more protectionist measures against China in coming years, as well as more Chinese firms establishing factories outside China and Western attempts to transfer Chinese technology back home, a reverse of what happened in the 2000s and 2010s.

Domestic Consumption

Evaluating the Current State of Consumer Spending in China

For China to truly achieve a balanced and sustainable growth model, the heavy lifting must eventually be done by the domestic consumer, at least if we apply the model of today’s developed economies to China. Household consumption remains stubbornly low, accounting for only around 38% of GDP, compared to a global average of over 60%.

The primary driver of this reticence is the ‘negative wealth effect’. For the average Chinese family, property represents the vast majority of their net worth. As apartment values fall, which they have since 2022, households feel poorer, even if their monthly income remains stable. A culture of thrift, government austerity measures, high youth unemployment and population decline are further factors weighing on spending.

Beyond the Trade-In Scheme: Extra Steps That Could Boost Spending

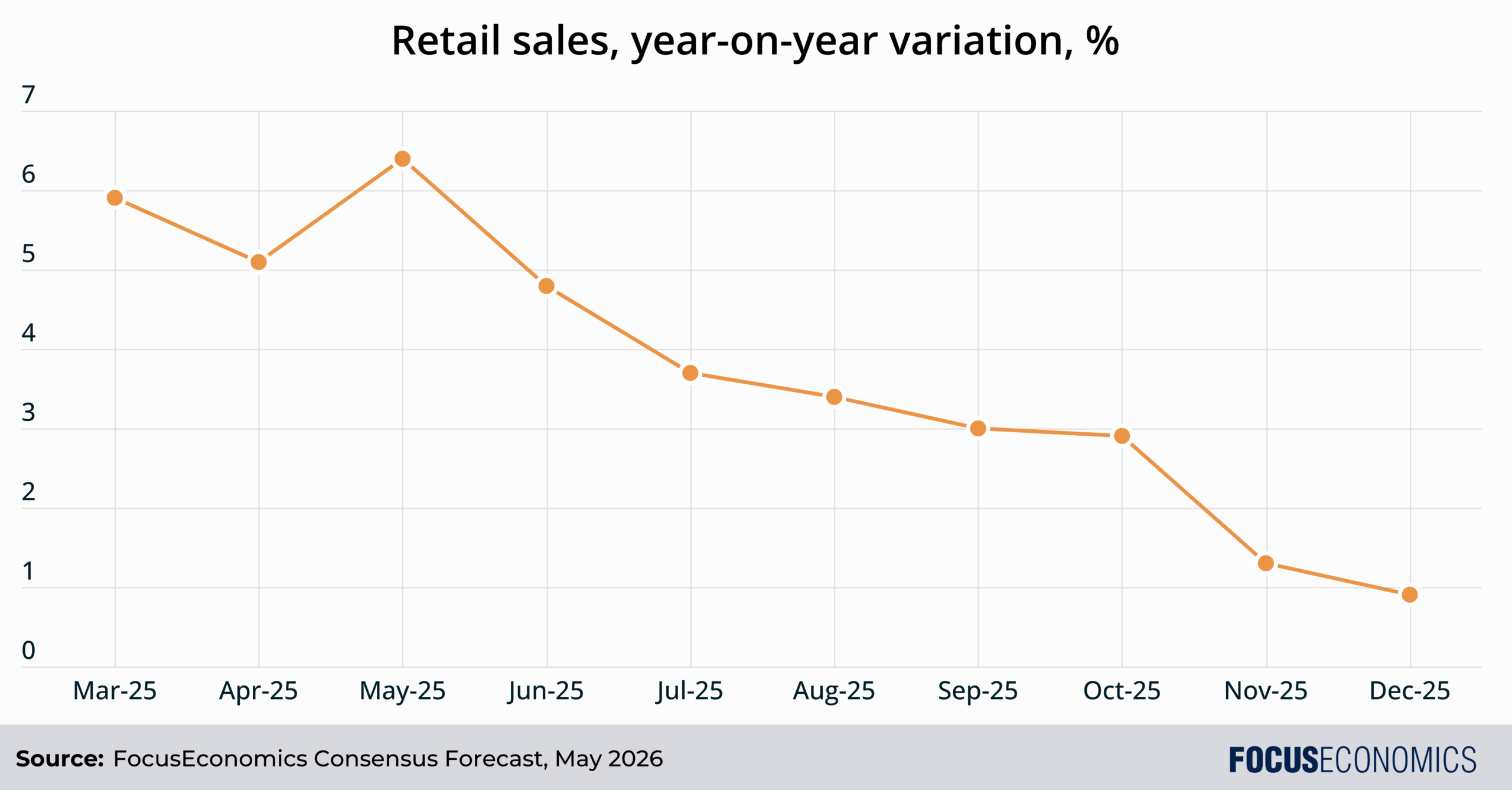

Recognizing the need to stimulate demand, Beijing rolled out an aggressive consumer goods trade-in scheme in 2024. This program offers subsidies and newer, more efficient models to households that trade in old appliances and cars. While the policy provided a temporary bump to retail sales in the first half of 2025, the boost faded from the middle of last year. Rather than creating new, sustainable consumption, it seemed to merely bring forward future demand.

To truly unlock the massive pool of Chinese household savings, more radical structural reforms are required. The first and most critical is an expansion of the social safety net. Chinese families save at exorbitant rates because they must self-insure against the risks of catastrophic healthcare costs, education and an underfunded pension system. If the state were to take on a larger share of these social costs, precautionary savings would naturally fall, liberating cash for discretionary consumption.

A second lever is tax reform. China’s tax system is heavily reliant on indirect taxes, which fall disproportionately on lower-income households. Shifting toward a more progressive income tax and increasing direct cash transfers to low-income families would boost the marginal propensity to consume. Lastly is reform of the hukou (household registration). Granting the hundreds of millions of migrant workers full access to urban social services would encourage them to settle permanently and spend like the middle class they have become.

That said, major tax reform seems unlikely for now, given the government’s ideological aversion to generous, European-style welfare states plus its focus on using available funds to boost industry.

Addressing Challenges in China’s Property Sector

Recent Property Indicators and Government Support Measures

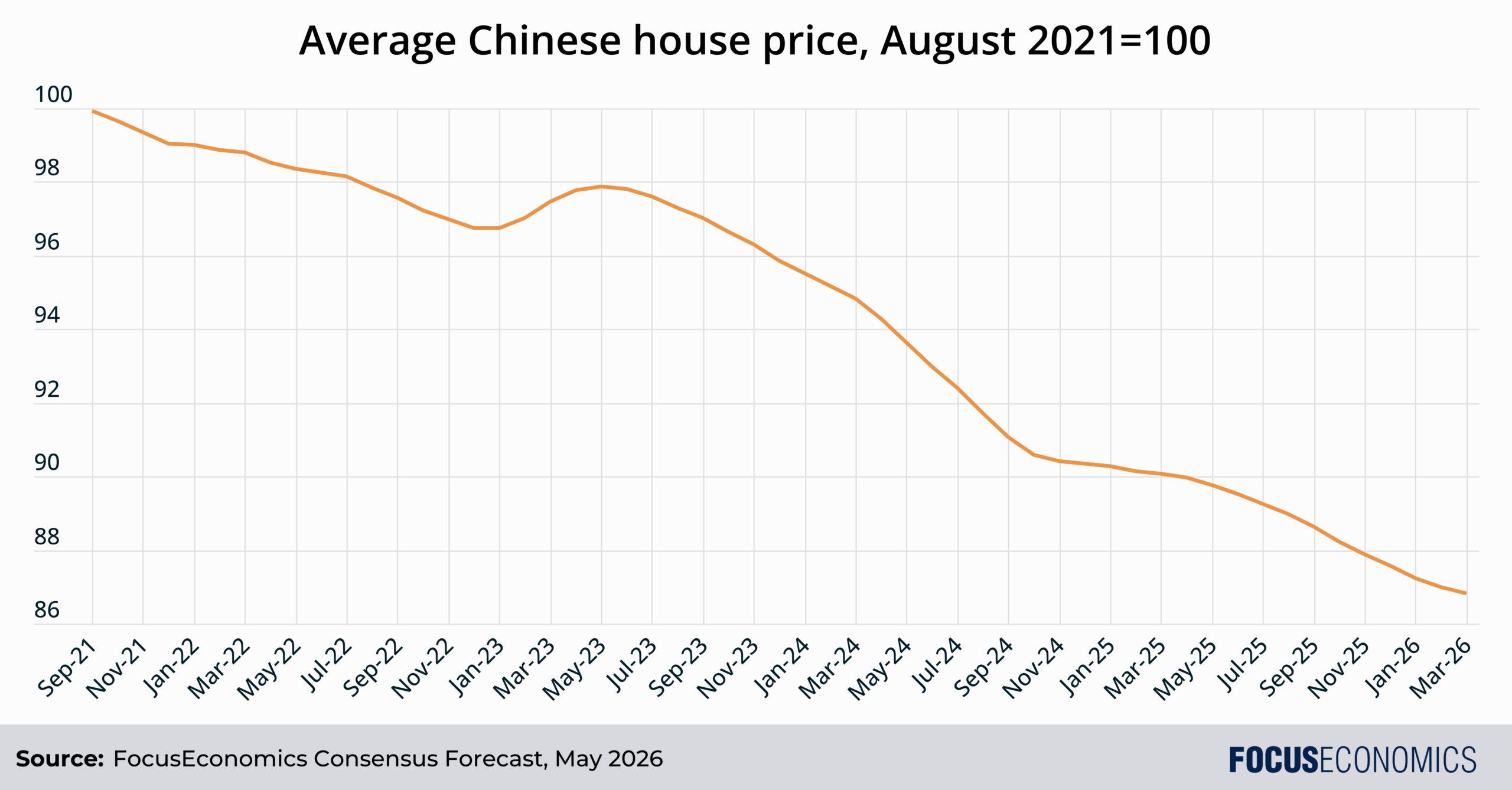

The real estate sector was been mired in a downturn for years, triggered by the government’s ‘three red lines’ policy designed to curb developer leverage: Home prices have fallen in annual terms every month since early 2022, as have construction activity and housing investment. The wealth destruction has been immense, directly weighing on consumer confidence and local government revenues, which historically relied heavily on land sales.

There have been a series of support measures at the national and local level, including lowering down-payment ratios, cutting mortgage interest rates, taking steps to support property developers and providing funding to complete unfinished housing projects. However, the efficacy of these measures has been limited. The pool of funds allocated for housing buybacks is small relative to the mountain of unsold real estate inventory. Local governments, already heavily indebted and deprived of land sales revenue, lack the fiscal capacity to execute these buybacks at scale.

The Structural Impact of the Housing Market Downturn

The downturn in the property sector is not merely a cyclical downturn. It’s a permanent structural reset. The era of real estate acting as the primary store of value for Chinese households and the main growth engine for the economy is over. This shift has profound implications for the fiscal architecture of the state. For decades, local governments funded their budgets and infrastructure projects by selling land to private developers. That model is broken.

With land sales revenue plummeting, some local governments have recently struggled to pay civil servants and maintain basic services. This has exposed the massive ‘hidden debt’ held by Local Government Financing Vehicles (LGFVs). To prevent a wave of local defaults, the central government has stepped in with debt swap programs, essentially moving local liabilities onto its balance sheet. This process buys time but does not solve the underlying mismatch between local expenditure responsibilities and revenue sources.

Structurally, the economy must now find new ways to allocate capital. For years, credit was disproportionately channeled into real estate, starving other sectors. Now, that credit must find its way into manufacturing and green tech. However, high-tech sectors cannot absorb the same volume of capital as property did, nor do they generate the same level of broad-based employment for lower-skilled workers. The transition leaves a gap in demand and employment that is proving difficult to fill.

Demographics and The Future of Economic Reforms

Domestic Structural Reforms

To successfully reach developed-economy living standards, conventional logical would suggest market-friendly reforms are necessary. The goal: Improve total factor productivity to compensate for a shrinking workforce.

A good place to start would be to level the playing field between state-owned enterprises (SOEs) and the private sector. Currently, SOEs enjoy preferential access to credit and land, despite being generally less efficient and less innovative than private firms.

Another potential area is financial reform. China’s financial system remains heavily dominated by state banks that favor state clients. Developing deeper, more transparent capital markets would allow for more efficient allocation of capital to high-growth, innovative private companies. Improving legal and regulatory predictability, thus avoiding abrupt crackdowns such as those on the tech and tutoring sectors in recent years, is another reform possibility

However, for now, China’s leadership appears intent on pursuing an alternative model to the West, one where the government maintains a key hand over the economy and society with a goal of ensuring stability, while promoting rapid AI diffusion and ferocious competition in favored sectors.

Demographics: The Economic Impact of an Aging Population

The ultimate constraint on China’s future growth is not its financial system or trade policies, but its demographics. China is aging rapidly. The labor force has already peaked and is now in a steady decline. The overall population has been declining too since 2022. The one-child policy, combined with the exorbitant costs of child-rearing in modern Chinese cities, has resulted in fertility rates well below the replacement level. China faces the daunting prospect of becoming old before it becomes rich.

The economic consequences of this demographic squeeze are profound. A shrinking workforce puts upward pressure on wages, threatening China’s competitive advantage in labor-intensive industries, though this chimes with the government’s goal of moving up the value chain. More seriously, it also implies a rising dependency ratio, with fewer workers supporting a growing population of retirees. This will strain the national pension and healthcare systems, requiring the central government to allocate a larger share of GDP to non-productive social expenditures.

To counter these headwinds, Beijing is betting heavily on automation and artificial intelligence. China is now the world’s largest market for industrial robots, as factories look to substitute capital for increasingly scarce labor. The government has also raised the statutory retirement age, a necessary but politically sensitive move to prolong the working life of the population. Ultimately, demographics make the push for a high-value, innovation-led economy an absolute necessity rather than a choice. China has no option but to generate greater productivity gains.

Conclusion: The Road Ahead

China’s state-led, export-led model has produced big wins, lifting hundreds of millions from poverty, transforming infrastructure and generating world-beating firms in many sectors. However, rising trade tensions with the rest of the world could test the limits of the country’s ability to export its way to wealth, at the same time as a tumbling population and workforce provoke domestic challenges.

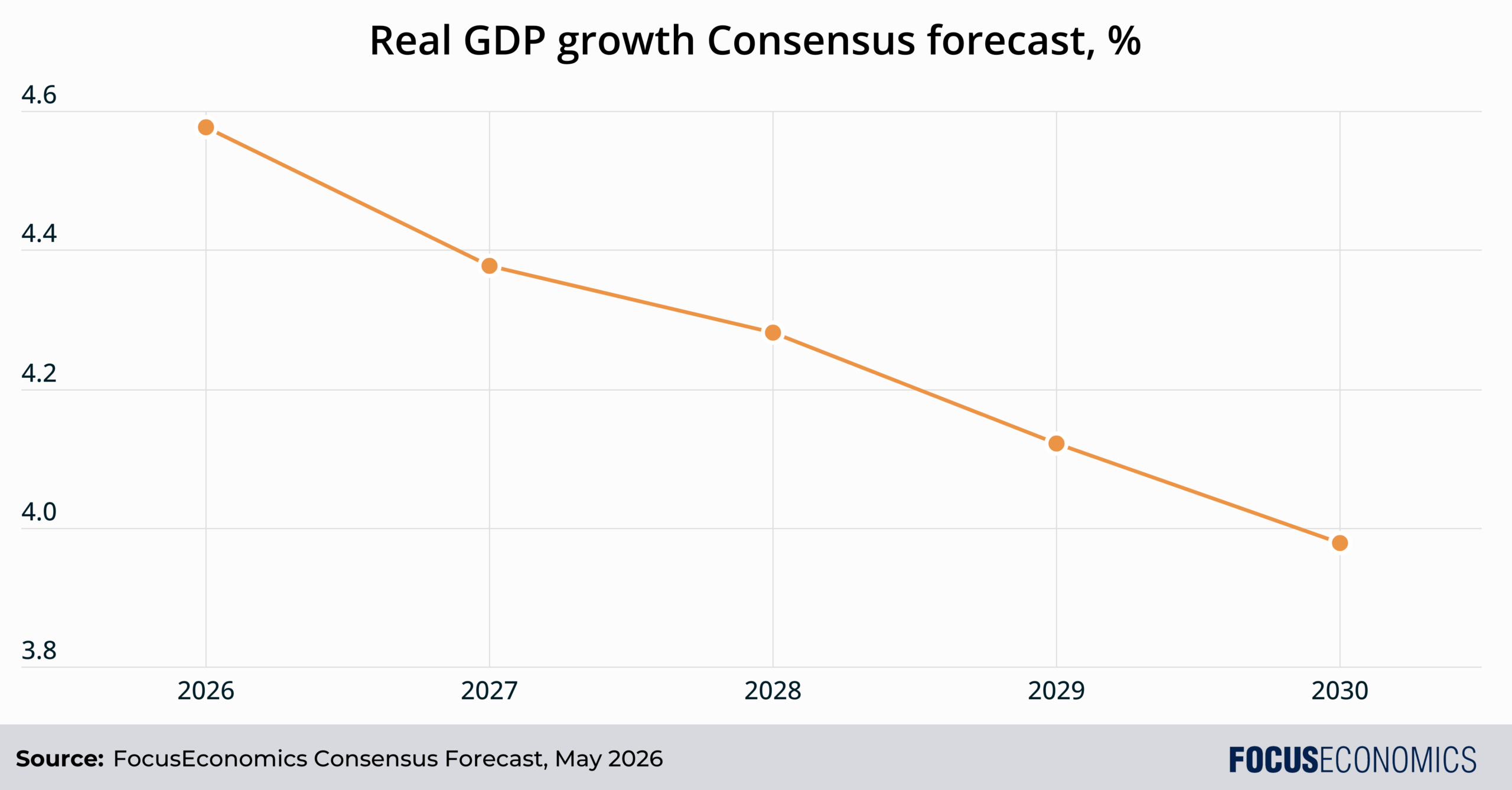

Our current Consensus is for China’s GDP growth to gradually decelerate in coming years as the demographic decline gathers pace, export restrictions increase and urbanization slows. However, even for 2030, panelists pencil in an expansion of 4.0%, above the global average.

No nation has yet reached Western living standards with China’s mix of highly interventionist economy, tech decoupling from the West, suppressed private spending, one-party rule, strict social control and lack of an independent judicial system. One thing is for certain: China’s efforts to become the first will be a fascinating economic experiment to watch.