In early 2026, the American economy resembles a high-stakes experiment. On one side, the country’s tech firms are pouring hundreds of billions into AI while the government has locked in lower income tax rates and attempted to deregulate in areas such as environmental protection and financial services. On the other, the administration is tightening the screws on the two historical drivers of American dynamism: The free flow of goods and the free flow of people.

The result is a decoupling—not just from China, but from the traditional economic orthodoxies that have governed the U.S. since the end of the Second World War. As the Federal Reserve prepares for a leadership change and AI productivity gains begin to show in the data, the question is no longer whether the American economy can grow, but whether it can do so while systematically dismantling the pillars of the globalized architecture it had strived to construct decades prior.

AI Investment vs Scientific Restrictions

If there is a secular religion in corporate America today, its central deity is the Large Language Model. The Trump administration’s recent white paper on “AI and the Great Divergence” frames the technology not merely as a tool, but as a national imperative—a way to ensure that “America wins the race” it started.

Investment is, by all accounts, staggering. Venture capital continues to flood into the sector, and the federal government has moved aggressively to preempt a fragmented policy landscape. By late 2025, a series of executive orders sought to strip states—most notably California—of their power to regulate “high-risk” AI. The administration’s logic is simple: In the battle for global dominance, any burdensome regulation is a form of unilateral disarmament.

While the U.S. deregulates the tech space and lavishes praise on AI company founders, the government has become far more heavy-handed and stingy when it comes to basic scientific research. According to Nature, the administration terminated or froze over 7,800 research grants, specifically targeting fields like infectious diseases, climate change and vaccines. The federal workforce has seen a massive exodus, with 25,000 scientists and personnel departing agencies like the EPA, NASA and FDA. Moreover, Trump has withheld billions in funding from top universities not deemed to be ideologically aligned with the President, resulting in some university researchers heading to places like Canada and Europe to continue their investigations. At the same time, the authorities have made it harder for foreign scientists to move to the U.S. for research. In short, the government appears to be betting that American capital and computation can compensate for the loss of global brainpower. It is a bold wager.

The Economic Impact of the Immigration Clampdown

Perhaps the most jarring shift in the 2026 economic landscape is the demographic one. For the first time in over half a century, net migration to the United States has turned negative. The immigration clampdown—a combination of tighter visa requirements, a Mexican border clampdown and a rise in the number of expulsions—has been rapid and effective. In 2025, net migration was estimated between -10,000 and -295,000.

For the American labor market, this is a supply-side shock of the first order. Historically, almost all growth in the U.S. labor force has come from immigrants. Without them, the breakeven employment growth—the number of jobs the economy needs to add to keep unemployment stable—has plummeted. We are now in an era of “jobless growth,” where the economy can expand by 2% while adding fewer than 50,000 jobs a month—which is exactly what happened in 2025.

This labor scarcity is estimated to reduce consumer spending by between USD 60 and USD 110 billion this year and next. In the longer term, it could force companies to innovate in order to step up automation, particularly in sectors like agriculture and manual labor, where native-born workers have shown no inclination to step into the roles vacated by immigrants.

Trade Barriers and the Effects of Tariffs on the U.S. Economy

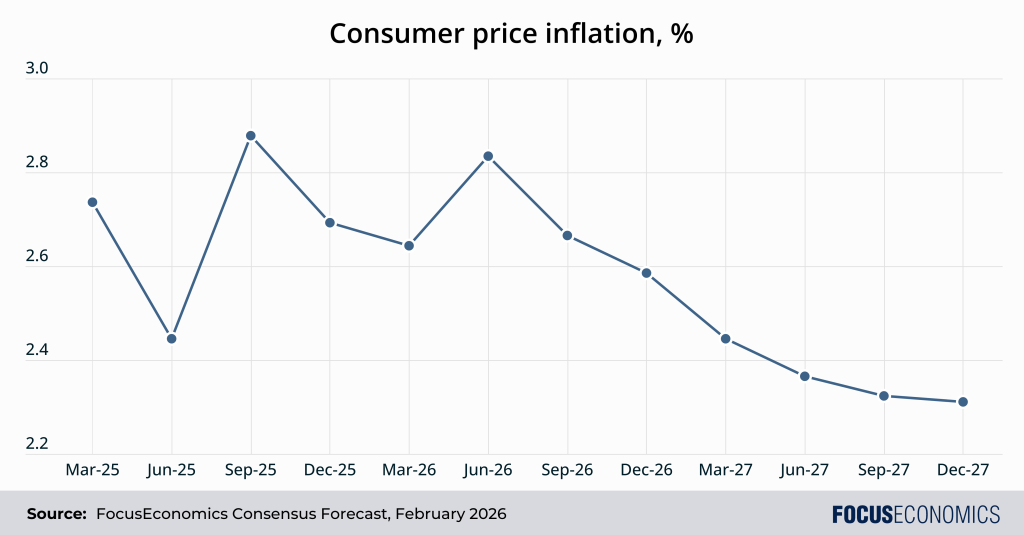

As of February 2026, the United States has reached a dubious milestone: The highest average effective tariff rate in nearly a century. That said, the impact on both inflation and GDP growth has been notably less than first feared; the U.S. continued to grow at the fastest pace in the G7 last year, while inflation peaked at 3.0% and has declined in recent months.

Moreover, in exchange for limiting tariffs on key trading partners, Trump has secured theoretically large concessions. For instance, Japan, South Korea and Taiwan have pledged USD 550 billion, 350 billion and 250 billion of investment in the U.S. respectively—figures which could provide a notable boost to U.S. GDP if they materialize.

Regarding revenue, in the year to date the government has raised more than USD 30 billion due to tariffs—more than triple the corresponding figure for last year. Over 2025 as a whole tariffs and excise duties raised around USD 290 billion, compared to around USD 100 billion in previous years. However, this is still only a small share of the total federal fiscal deficit of around USD 1.8 trillion.

Institutional Threats and the Fed Interest Rate Forecast for 2026

No institution in Washington is under more pressure than the Federal Reserve. As Jay Powell—long in the crosshairs of President Trump—prepares to exit the stage in May 2026, the question of Fed independence has moved to center stage.

A Federal Reserve that is seen as a wing of the Treasury would lose its inflation anchor; if bond buyers believe the Fed will keep rates artificially low, they will demand higher yields to compensate for the risk. This would lead to the ultimate irony: A politically captured Fed meant to lower mortgage rates could actually end up driving them higher.

Most of the panelists polled by FocusEconomics see rates on hold until Q2, at which point monetary easing is likely to resume. Our Consensus is for two 25 basis point cuts in the second half of 2026, bringing the upper bound of the Fed funds target range to 3.25%, though projections range from the Fed on hold to 100 basis points of extra cuts. Regarding the next Fed Chief, Kevin Warsh is Trump’s pick; Warsh was previously on the Fed’s board in the late 2000s and is seen by markets as unlikely to advocate for radical interest rate cuts, which has helped assuage investor concerns about the Fed’s independence somewhat recently.

Our Forecasts for the U.S. economy at large

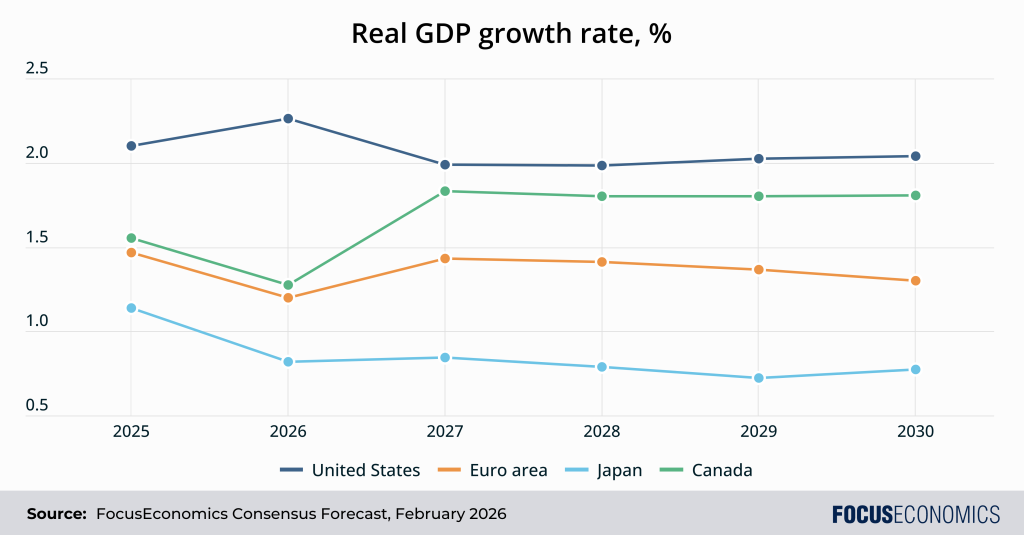

Our panelists see GDP rising 2.3% this year—0.6 percentage points higher than forecast in mid-2025 in the wake of Trump’s tariff announcements. As a result, the U.S. will outperform all G7 economies for the fourth straight year. Ongoing capital investment in and productivity gains from AI will be a key driver, as will looser monetary policy and fiscal support from the One Big Beautiful Bill Act.

There are plenty of downside risks: A misstep at the Fed, a retaliatory trade war that spirals out of control, or a failure of AI to translate into real-world productivity to name but a few. For now though, America is acting as the world’s most aggressive venture capitalist—investing heavily in itself while cutting off its oldest partners.

Insight from our panelists:

TD Economics’ Ksenia Bushmeneva said:

“The economic divide between America’s households at the top of the income spectrum and everyone else continued to widen last year. Upper-income households benefited from the still-robust wage growth, strong gains in equity markets, and better access to consumer credit. Despite these diverging fortunes, elevated economic uncertainty and a slowing labor market, overall consumer spending has remained surprisingly resilient. In 2026, consumer spending is expected to remain solid, supported by easier financial conditions, wealth gains, higher tax refunds and lower taxes, and some stabilization in the labor market. Still, the economic divide underneath the surface is likely to widen. The tax cuts are expected to benefit higher income households the most, while a reduction in funding to various government programs will weigh on low-income households.”

EIU analysts said:

“A sharp tech or AI-related stock market bust would rank among the most serious downside risks to the US growth outlook. A large, sustained equity correction of dot-com magnitude today would lower the level of US GDP as higher risk premia, weaker business investment and tighter credit conditions feed through the economy. The shock is likely to be larger than the dot-com period because US households are now far more exposed to equity prices: direct and mutual-fund equity holdings account for a much larger share of household assets than in 2000, so a market slump would generate powerful negative wealth effects and a marked slowdown in consumption. At the same time, AI-related projects currently account for more than the entirety of US business fixed investment growth, meaning that a sudden reassessment of AI earnings prospects would trigger a disproportionate pull-back in capital expenditure and hiring.”

Access Extensive Data & Forecasts for the U.S. Economy

We invite you to have a look at FocusAnalytics, our macroeconomic data platform where you can access forecasts from hundreds of top sources in one powerful platform. Start a free trial here: https://www.focus-economics.com/free-trial/