See-saw price movements: After trending relentlessly upward in 2025, gold prices have had a volatile start to the year, rising from USD 4300 to a record high of nearly USD 5300 before crashing back to the high 4000s in late January. Silver saw even more violent price movements, going from around USD 70 per ounce at the start of the year to a peak of USD 121 in late January before pulling back to below USD 80. Overall, the crash wiped roughly USD 7 trillion from the two metals’ market value.

Structural drivers obscured by short-term speculation: The January price ramp-up was partly due to fundamental factors such as central bank purchases, geopolitical tensions, the EV transition, investor concerns over the USD, and new Chinese silver export rules. However, speculation by retail investors also played a role. They initially boosted prices by making option-related trades and leveraged purchases, but then sent them crashing after they decided to sell to lock in profits. The collapse in silver prices, in particular, was amplified by low liquidity in the London market.

Positive price story remains intact: Despite the whipsawing recently observed in markets, the aforementioned fundamental bullish factors haven’t gone away, and are unlikely to in the coming months or even years. Central banks and investors will likely continue hedging their exposure to the USD by purchasing precious metal as a result of unpredictable U.S. policymaking; moreover, the shift to cleaner energy will continue to gird industrial demand for silver. Finally, the supply of gold and silver is inelastic and thus unlikely to see a sudden increase.

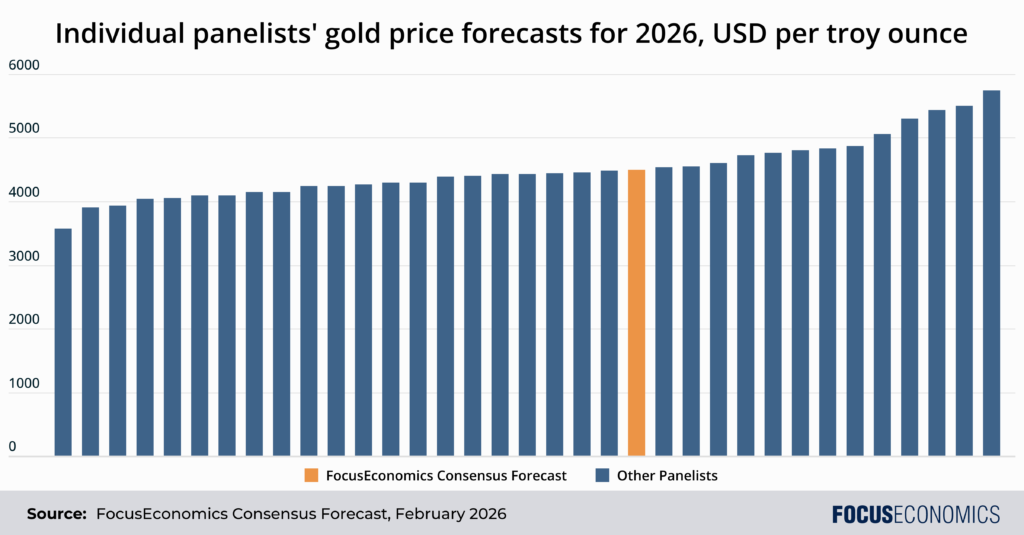

Our Consensus Forecasts: Our panelists see both silver and gold prices averaging at historically high levels this year, though the spread among forecasters is extremely large—reflecting recent wild price swings. In gold for instance, our Consensus is for the metal to average at USD 4500 this year, with a maximum forecast of USD 5750 and a minimum forecast of USD 3575. The spread in silver is even more extreme, with forecasts ranging from USD 41 to USD 115 and a Consensus of USD 65. In these times of price volatility, the Consensus Forecast—the average projection made by our panel of 30+ economists—is now more than ever the reliable guide to what will happen with gold and silver markets ahead.

Insight from our panelists:

On the gold outlook, Goldman Sachs analysts said:

“We continue to see significant upside risk to our gold forecast of $5,400/toz by Dec 2026. Our forecast incorporates two drivers: that central banks maintain their recent pace of accumulation (60 tonnes monthly average over past 12 months) and that private investors step up gold ETF purchases as the Fed cuts rates. We do not account for potential further private sector diversification –a source of additional demand that we view as a significant upside risk to the outlook, because gold allocations in Western financial portfolios remain low. Gold ETFs account for just ~0.20% of US private financial portfolios. We estimate that every 1bp increase in the gold share of US financial portfolios–driven by incremental investor purchases rather than price appreciation–raises the gold price by ~1.5%.”

ING analysts commented on speculative purchases and sales:

“CFTC [Commodity Futures Trading Commission] positioning shows a cooling in speculative interest across precious metals. Managed money [hedge fund] net longs in COMEX gold fell by 17,741 lots last week to 121,421 lots, driven by a drop in gross longs. Speculators also cut net longs in silver by 4,032 lots, the third weekly reduction, taking positioning to its lowest since February 2024. Overall, volatility across precious metals is likely to remain elevated in the near term. For gold and silver, macro uncertainty, real rate expectations, and USD direction will continue to dominate sentiment.”

Our latest analysis:

Mexico’s GDP growth was better than expected in the fourth quarter.