Bond vigilantes smell blood

In recent weeks, investors from London to New York have dumped government debt, driving 10-year government bond yields in the United Kingdom and the United States to their highest level since the 2007–2008 financial crisis, and those in France and Germany to the highest since the peak of the Euro area debt crisis in the early 2010s. Japan’s sleepy debt market was not immune, with 10-year bond yields rising above 1% for the first time since 2011.

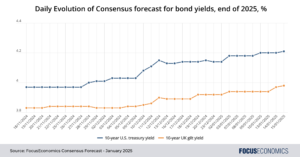

Our panelists revise up their forecasts

As part of our Daily Updates to our Consensus forecasts, every day our panelists send us their latest forecasts for the 198 countries and 39 commodities that we cover. These are available via our FocusAnalytics platform. In recent days, our panelists have revised up their forecasts for 10-year bond yields for the UK and U.S. at the end of 2025:

In recent days, bond yields have since fallen thanks to a lower-than-expected core inflation figure in the U.S., and our panelists still expect bond yields in both countries to cool from current levels as inflation eases and central banks cut interest rates. The difference is that, now, they expect them to be higher than before, remaining at some of the highest levels since the financial crisis and raising pressure on government finances.

What has driven the increase in yields?

In part, the rise in yields is due to Donald Trump’s reelection as U.S. president in November; his tariffs will stoke inflation, forcing the U.S. Fed to cut more slowly, and his tax cuts will fatten America’s public debt pile. In the UK, the selloff in bonds was driven by a lack of confidence in the government’s fiscal consolidation plans, which are based on relatively optimistic projections for GDP growth.

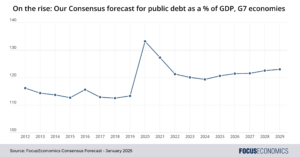

In all advanced economies, however, the recent rise in yields reflects a deeper cause: The steady rise in public debt. In October, in its Fiscal Monitor report, the IMF said that it expected public debt to rise to 93% of the world’s GDP by the end of 2024 (over USD 100 trillion), and approach 100% by 2030. This would be the largest share since World War II, and above that seen in World War I. Why has this occurred? The rise of populism has discouraged politicians from making difficult decisions about government taxation and spending, with Boris Johnson, the people-pleasing ex-Prime Minister of the UK, stating once that “my policy on cake is pro having it and pro eating it.” This has compounded the strain on public finances from ageing populations, the Covid-19 pandemic, the push toward renewables, the recent spike in energy prices, and rising geopolitical insecurity.

Insight from our analysts

On the recent bond rally, DBS economists commented:

“US Treasuries rallied across the curve as inflation data proved to be not as bad as feared […]. That said, we note that this is merely a sentiment shift (not so much a shift in fundamentals) and the rally marks a much needed pullback from extremely stretched levels. Market participants still have to contend with policy uncertainties after Trump gets inaugurated next week. We suspect that Trump uncertainty may be an even more important factor than CPI in driving rates.”

On UK debt, Goldman Sachs analysts said:

“We continue to think that slowing growth momentum and easing domestic inflationary pressures, as further evidenced by the decline in underlying services inflation in December, will allow the BoE to deliver more rate cuts than markets are currently pricing. This should help anchor Gilt yields—the latest CPI release was a start in that direction. As such, we remain positive on Gilts and expect 10y yields to end the year at 4%.”

Our latest analysis

- Peru’s central bank cut rates on 10 January. Read more here.

- In the Dominican Republic, there was also monetary policy easing recently.