Kast takes the reins: Chile’s new president took office in March announcing an immediate 3% cut in departmental spending. In mid-April his government then announced a package of reforms, including a corporate tax cut, reduced environmental restrictions, financial employment incentives and measures to encourage greater investment. The package could face resistance in Parliament given Kast’s Republican Party is nowhere close to a majority on its own in either house of the legislature.

The Iran war will be a headwind one way or another: The new government allowed fuel prices to rise at the fastest pace in decades in March by deliberately not using a state mechanism to temper the pass-through from surging global energy costs. Together with further fuel price hikes from April, this will raise inflation and strain consumer spending; our panelists currently see inflation jumping to 3.6% in Q2 from 2.7% in Q1. The move has predictably proved politically unpopular, with some truck drivers already announcing strike action. If the government eventually bows to public pressure, this would limit inflation at the cost of widening the fiscal deficit—precisely the opposite of what the new president aims to achieve.

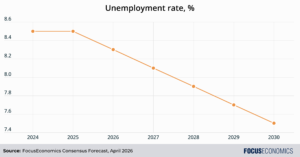

The new government has ambitious goals: GDP growth of close to 4% a year and an unemployment rate of 6.5% by 2030 are two objectives outlined explicitly by the new administration. Another striking figure is Kast’s pre-election pledge to cut public spending by USD 21,000 billion, or over 5% of GDP, in order to stop the steady upward trend in the public debt-to-GDP ratio observed in recent years.

Our panelists appear largely unconvinced: The lofty rhetoric is so far not matched by our Consensus forecasts. Let’s take GDP growth to start. Our panelists currently predict the economy to expand slightly above 2% per annum for the rest of this decade, almost identical to the forecasts made before the Q4 2025 elections. This wouldn’t be a catastrophically slow pace, but neither is if fast enough to enable a meaningful convergence to average OECD living standards. The unemployment rate, meanwhile, is seen above the government’s target, declining only gradually from 8.5% last year to 7.5% by 2030.

As for the fiscal balance, it is expected to narrow under the Kast administration, from 2.8% of GDP last year to 1.4% in 2029. However, this is at least partly due to far higher copper prices in the next few years than in 2025, and panelists don’t seem to judge the goal of cutting USD 21,000 billion from spending as credible.

Insight from our panelists:

On the implications of the Iran war, EIU analysts said:

“We expect that the conflict will not change Mr Kast’s economic policy priorities, which include front-loading fiscal consolidation, easing environmental and labour regulations, cutting the corporate tax rate and expanding the remit of public-private partnerships. Mr Kast will also pursue tough-on-crime policies, stop undocumented migration, deport those in the country illegally, and implement tax cuts and business-friendly reforms. However, these reforms will require legislative support. The inflation caused by the war has dented Mr Kast’s approval with voters, posing moderate but growing risks to governability in the short term.”

On politics, Itaú Unibanco analysts said:

“President-elect Kast’s cabinet will target higher growth. Jorge Quiroz was confirmed as Minister of Finance, while Daniel Mas will head both the Ministry of Economy and the Ministry of Mining. The picks underscore the focus on advancing measures to streamline investment, cutting corporate taxes, and implementing a fiscal adjustment. The remainder of the cabinet consists of technocrats and experienced politicians across the political spectrum. Chile’s political “honeymoon period” is relatively short (around six months), offering a narrow legislative window to advance priority reforms.”

Our latest analysis:

China’s economy outperformed market expectations in Q1.

The UK’s GDP growth was deceptively strong in February.