The first half of 2018 was marked by the slow death of the Goldilocks markets – the environment of relatively subdued volatility, and persistent inflows of funds into risky assets. The economic environment was supportive of the Wall Street: low wage inflation and unemployment prints, robust headline growth, and gradual monetary policy tightening in the U.S., moderated by the continued monetary easing in Europe, Japan and China – all offered the prospect of the lasting nirvana.

In contrast, the second half, and especially the last quarter of 2018 offered us a glimpse of what awaits investors in 2019 and 2020. The Goldilocks era was sharply bumped off its pedestal to be replaced by the VUCA (volatile, uncertain, complex and ambiguous) dynamics of the markets consumed by the re-coupling of key risks. These risks are here to stay.

The main driver of the VUCA dynamics is the monetary policy shift from QE (quantitive easing) to QT (quantitive tightening). In the second half of 2018, we witnessed the early omens of the major impact yet to come. Global dollar liquidity conditions have started deteriorating. Having averaged at around 6 percent annual growth rate from mid-2011 through 1H 2018, global M2 money supply growth fell below 5 percent in 2H 2018. The signs of this coming were already in place back in 2017, but few paid any attention to it back then. By September 2018, global liquidity supply was shrinking, hitting annual rate of decline of 1.4 percent in November 2018. Dollar strengthened substantially, with trade-weighted green buck ending 2018 at the highest level since 2001.

Change in the direction of the monetary policy across a range of the advanced economies, most importantly the coupling of the U.S. Fed tightening with the forthcoming end of the QE by the ECB, can trigger a range of VUCA loops – the downward pressures during which the markets can enter self-sustaining sell-offs. Based on our past experiences, we know of at least four such coupled factors, all capable of triggering the next systemic crisis.

The first potential trigger is the sovereign-financial loop. Pressures in sovereign bond markets can propagate through bonds holdings by government agencies (fiscal channel), central banks (monetary channel), and banks (banking channel). Following the Global Financial Crisis, U.S., Japanese, European and other banks have dramatically increased their holdings of government debt. Increasingly, these holdings are concentrated in the bonds issued by the governments of the countries of bank domicile. These positions are not set against capital reserves, effectively leaving the banks without any safety cushion against a liquidity shock or a sell-off. Monetary tightening, by increasing interest rates, is putting downward pressure on key government bonds valuations. At the same time, ample supply of U.S. Treasuries (fuelled by rising deficits and declining Fed holdings of bonds) in 2019 is now set to run into the declining demand for Treasuries from key foreign buyers. Both factors are putting at risk banks’ valuations of their bond holdings. A sharp sell-off can trigger the demand for banks bailouts – a cost many governments cannot absorb without a dramatic increase in fiscal deficits, which will push further losses onto banks’ balances sheets, leading to more bailouts. The sovereign-banks risk loop – the core problem exposed by the euro area crisis of 2010-2014 – has never been resolved, and in 2019-2020, we just might have to pay a high price for failing to do so.

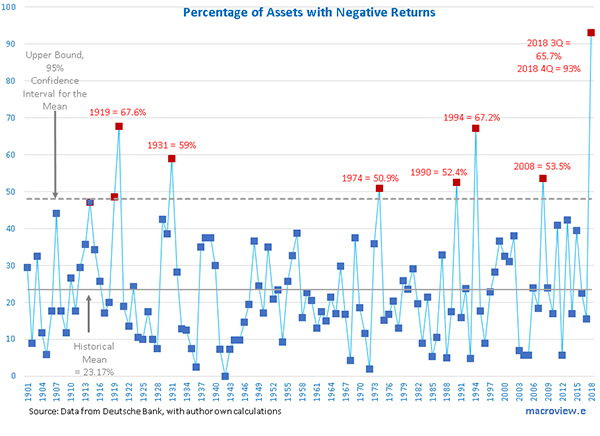

The second factor that can trigger the next crisis is the impact of highly volatile markets on the value of the financial collateral. As in 2006-2007, the problem is further exacerbated by the leverage accumulated in the financial snd economic systems. So far, declines in the values of shares have not triggered margin calls. However, a squeeze in the corporate bond markets, private equity and venture capital, or a sharp deleveraging in the real economy, can easily trigger solvency problems across the corporate sector, leading to a simultaneous decline in equity prices and a surge in bad loans on banks’ balance sheets. Combined effect of major corrections in several markets can trigger a sell-off of liquid assets, pushing down capital buffers and feeding into a sovereign-financial VUCA loop outlined earlier. Chart below shows the extent of leverage in the U.S. economy and the associated decline in the effectiveness of debt to sustain economic growth (see the fourth factor below).

The third factor is the increasing degree of complexity in markets strategies designed to control for risk. Investors hedging of risks arising in one asset class can lead to a cascading sell-off in, or rotations into and out of, different assets. This creates both, contagion channels and increased uncertainty in the markets, effectively replacing priceable risk dynamics with less manageable VUCA dynamics. One example of this from the late 2018 is the large scale rotation by investors out of corporate debt into Government debt, that has been adversely impacting not only asset valuations, but also market signals underlying monetary policy. In the presence of VUCA dynamics, these problems are further exacerbated by market herding.

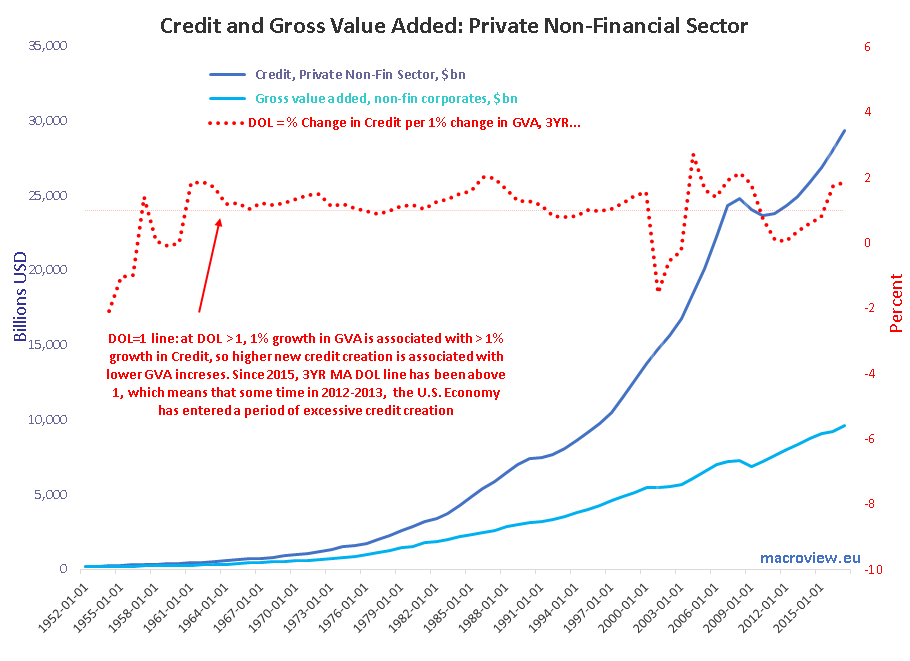

The fourth, and perhaps the most important in the long run, factor is the real economy’s reliance on debt, or the real credit cycle (highlighted in the second chart above). Over recent years, dramatic increases in corporate debt, coupled with reduced equity cushions (due to rampant shares buybacks and M&As, fuelled by cheap debt), have increased corporate sector vulnerability to rising interest rates. 2017-2018 changes to tax deductibility of interest in the U.S. are adding some fuel to the fire of monetary policy ‘normalization’ by the Fed. Recent indicators from the banking sector show sharp fall-offs in domestic non-financial and asset-backed credit outstanding in the U.S. Net interest margin uplift through 2018 has also been dramatic, and provisions for bad loans are rising steadily across the U.S. banking sector. This problem is even more pronounced in Europe, where structural weaknesses in the credit-fuelled economy, and lack of long term productivity growth are now driving sharp fall-off in macroeconomic indicators even before the onset of ECB monetary tightening.

In simple terms, 2019 is likely to be a year of structural breaks and VUCA re-coupling. Advanced economies’ weakening real growth conditions are likely to run parallel to the financial markets characterized by rising liquidity risks, increased volatility and uncertainty. Growing complexity of financial strategies deployed to counter these risks will become tightly coupled with the ambiguity of the overall macroeconomic and monetary policies, as the U.S. and the rest of the world diverge on fiscal deficits and monetary tightening. Pursuit of growth by policymakers and chasing of higher returns by investors can easily give way to deleveraging and wealth preservation objectives. Such a shift, while overdue, is likely to be a painful one for all involved.