Kunal Kumar Kundu is the India economist at Société Générale CIB based in India, where he has been since August 2013. Kunal has more than 17 years of experience in financial research and has held a variety of roles in global finance. He started his career as a journalist with Dalal Street Investment Journal (one of India’s leading investment magazines) in 1996 and has a Master’s in Economics along with post-graduate diplomas in Business Management and Equity Research & Analysis.

Kunal Kumar Kundu is the India economist at Société Générale CIB based in India, where he has been since August 2013. Kunal has more than 17 years of experience in financial research and has held a variety of roles in global finance. He started his career as a journalist with Dalal Street Investment Journal (one of India’s leading investment magazines) in 1996 and has a Master’s in Economics along with post-graduate diplomas in Business Management and Equity Research & Analysis.

FocusEconomics: How have your forecasts been affected by the government’s demonetization?

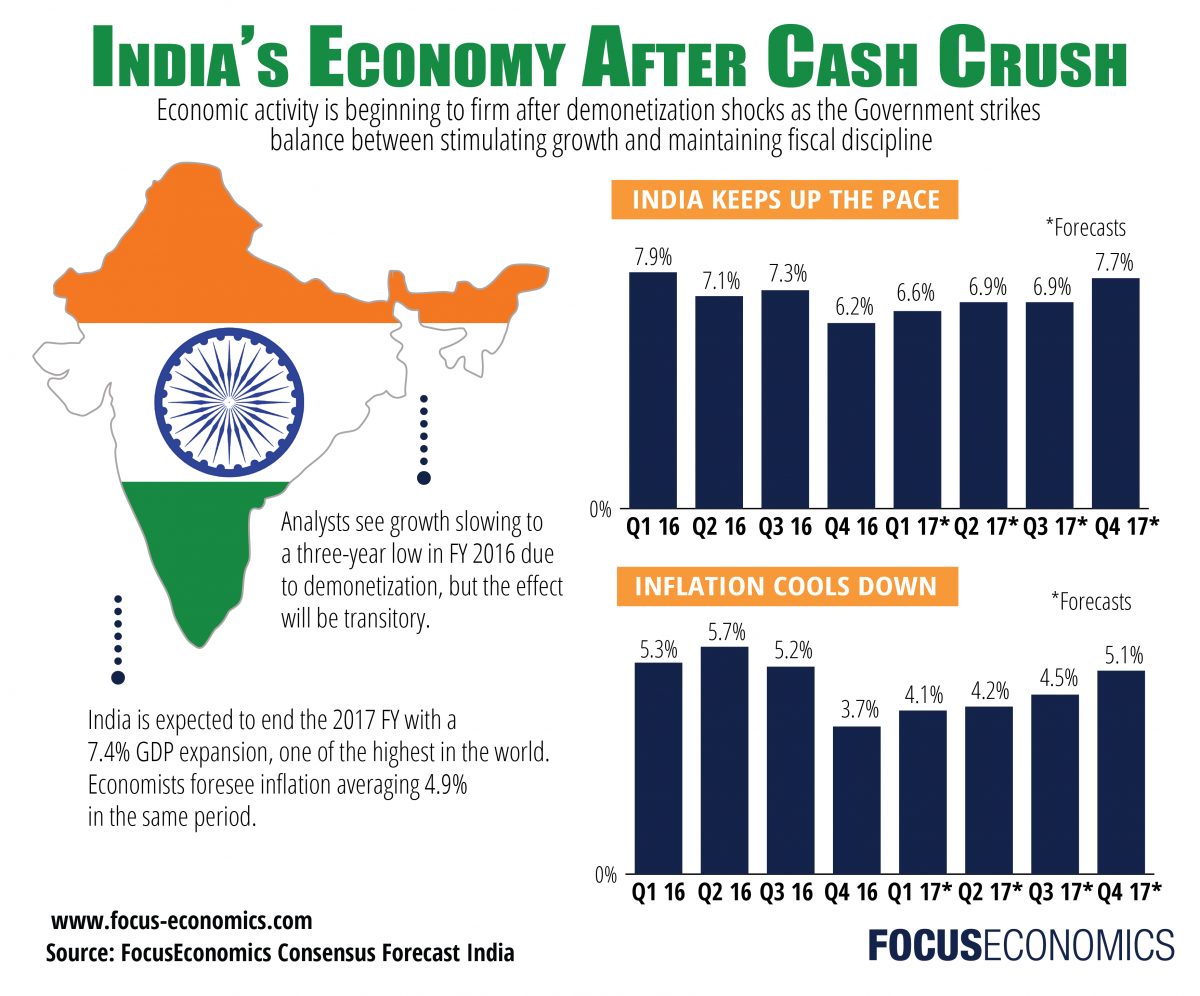

Kunal Kundu: Removing 86% of the currency in one fell swoop from an economy that is predominantly cash-based (approx 80% of transactions take place in cash) ought to have had an impact on India’s overall economic activity. We believe that India’s informal sector, which accounts for roughly 80% of employment and roughly 40% of GDP, is likely to have been the most affected given that the majority of transactions in this space take place in cash. Crimped demand, especially in rural areas, ensuing falling capacity utilisation and weakening business confidence ought to have resulted in a far lower growth rate than India would be comfortable with. The sharp drop in headline CPI to sub-4% corroborates our fear. We believe the currency shortage will last at least until the end of March 2017, if not later, before things eventually return to normal. As per data from the Reserve Bank of India (RBI), India could achieve remonetisation (the introduction of new currency notes in lieu of the scrapped old ones) to the extent of 60% during the three-and-a-half month period post demonetization.

According to a study by India’s largest organisation of manufacturers, the All India Manufacturers’ Organisation (AIMO), in the first 34 days following demonetisation, micro and small scale industries suffered 35% job losses and a 50% dip in revenue. The AIMO, which represents over 300,000 MSME and large-scale industries engaged in manufacturing and export activities, also projected a drop in employment of 60% and loss in revenue of 55% before March 2017. According to the study, the factors that have contributed to the impact include zero cash inflow, rules curtailing cash withdrawals, staff absenteeism, a weaker rupee, choked fundraising options, the inability of banks to work on proposals and a derailed real estate sector, among other factors.

We believe that a large number of job losses will lead to a highly stressed household sector and hence weakening consumption. Evidence suggests that investment dropped substantially in calendar 4Q16. We expect investments to remain weak or weaken even further in the current year, and this in turn will further impact the household sector. Hence we do not expect the pain to go away in two quarters but rather to continue for at least four quarters, if not more. Essentially, we believe that as the private investment recovery gets pushed back further, household stress is set to continue, leading to a negative spiral.

Click on the image above to open a full-size version

FE: What is your view on the recently released official GDP data?

KK: India’s official 3QFY17 (April 2016 to March 2017) GDP data surprised all and sundry. In fact, by suggesting a real GPD growth of 7% yoy, as compared to market expectations of 6.1% yoy, it managed to surprise every economist polled by Bloomberg (where the highest forecast was 6.9% yoy). At the disaggregated level, however, the data raises more questions than it answers as it contradicts other official data and even some high frequency data. We believe that this data, in all probability, will be revised downward.

There are multiple challenges, including poor rural wage growth and weak farm income, especially due to the trashing of perishable items by farmers on account of a fall in demand as the cash-driven supply chain came to a grinding halt. This situation ought to have resulted in weak Gross Value Added (GVA), yet GVA growth in agriculture was unusually high. Despite high and rising inventory accumulation, falling capacity utilisation and one of the weakest growth rates in personal loans during the quarter, private consumption grew by a huge 10.1% yoy. Under these circumstances, one cannot begin to comprehend a sharp growth in manufacturing.

It seems that the Indian Central Statistics Office (CSO) has not been able to collect comprehensive data from the informal sector. We believe that as more data flows in, the GDP data will need to be revised down.

FE: What is the scope and timing of any fiscal gains from demonetization?

KK: The basic assumption of demonetisation is that the informal sector activity is purely a reflection of the black economy and hence demonetization will push toward more formalisation leading to more tax revenue generation. We think that this is a fairly exaggerated expectation. While we agree that the probability of generating black income is higher in the informal sector than in the formal sector, the fact remains that not paying taxes is not the main reason why farms tend to operate in the informal sector. Onerous regulations force many farms to remain informal. Moreover, the majority of employees in this sector earn income which remains under the minimum threshold for income tax.

FE: Would you elaborate a bit more on why is black income generated and what are its sources?

KK: I see three main factors that generate black income:

- Inadequate direct tax reforms – While much discussion has taken place over the last decade, no action has been taken so far. Reforming direct tax and ensuring better intelligence will likely prove to be more effective in curbing black money than demonetisation.

- Lack of transparency in political funding – In India, the process of political funding remains very opaque and has evolved into a major end-use for black money. The recent announcement of a maximum amount of permissible cash donations will hardly have any meaningful effect unless transparency is ensured.

- Non-taxing of agriculture income tax – Agricultural income is not taxed at all in India. For a country with such a poor direct tax-to-GDP ratio, it is incomprehensible how virtually 15% of the economy remains untaxed. In fact, this has emerged as a significant conduit for tax evasion as a large chunk of income is shown as agricultural income and hence there is no incidence of tax.

FE: The RBI recently shifted its stance from accommodative to neutral, do you see any rate hikes in India’s horizon?

KK: As of now, given the official data alleging fairly high growth despite demonetisation, it seems that the RBI is done with its rate-cutting cycle. Also, a potential rate hike in the US and the recent movement of commodity prices will keep the RBI in a wait and watch mode.

FE: The government stuck to a broadly market friendly budget for FY 2017-2018 with a fiscal deficit target of 3.2% of GDP. Do you see this as achievable?

KK: Like the past few years, we think that the government will achieve the target as this is now its primary focus. Historically, we have seen the government cutting capex or resorting to accounting practices to keep the deficit in check if revenue falters. As of now, we have no reason to believe that the deficit target will be breached.

FE: What are the key risks for India’s outlook?

KK: A sharp spike in oil prices and major trade protectionism by the US.