Insights from Our Analyst Network

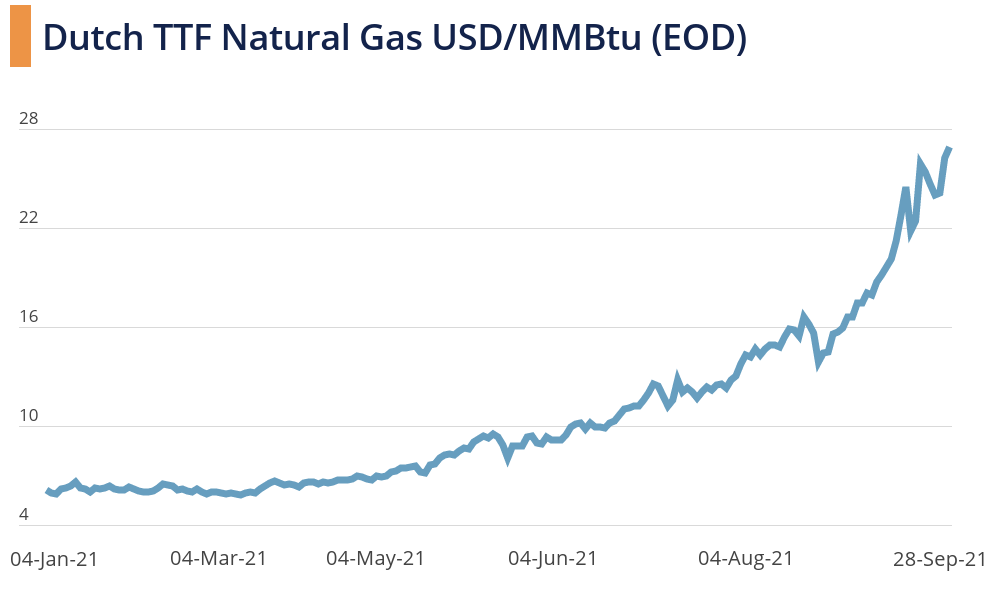

Commenting on the short-term outlook for the European gas market, Warren Patterson and Wenyu Yao, commodity economists at ING, said:

“The natural gas market continues to trade at elevated levels as concerns around tightness going into winter continue to linger. European gas storage is a little over 72% full, compared to the 5-year average of around 88% for this time of year. At times, it has appeared as though LNG supplies could offer some much-needed relief to the European gas market. However, spot Asian LNG prices have more than kept up with the strength in the European market. So, with the spot Asian market trading at a premium to Europe, spot LNG flows are likely to continue to make their way into Asia, rather than relieving some of the tightness in Europe.”

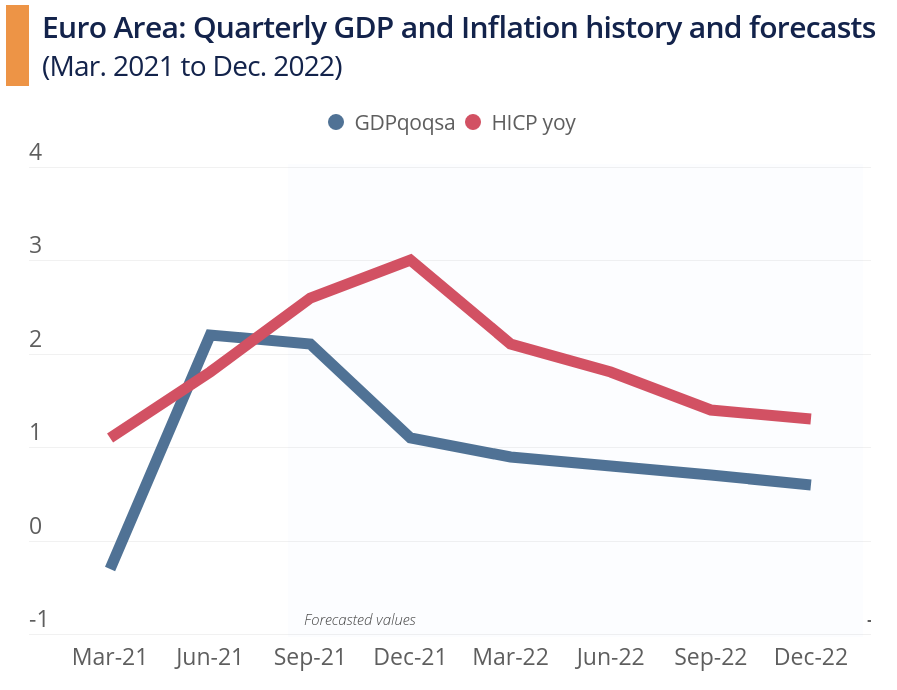

Commenting on the impact of rising gas prices on the Euro area economy, analysts at JPMorgan noted:

“At face value, the recent rise in market gas and electricity prices could increase headline inflation by 0.5 percentage points in the short run. We think this increase will not be reflected fully at the consumer price level and we forecast a 0.3 percentage-point boost to headline inflation in September. […] Regarding consumption, the link between prices and household spending is not very tight. The purchasing power hit coming from gas and electricity prices could be contained. On the production side, there is a risk of disruption in some industries reliant on gas and electricity. But so far, there is very limited evidence of such disruptions in the Euro area. As a result, we leave our near-term GDP forecast unchanged.”

Our Latest Analysis

- How has the pandemic affected global trade? What is the global trade outlook going forward? Find out in our latest special report.

- The Federal Reserve kept its monetary stimulus measures unchanged in September, but our economist Steven Burke has the latest on what to expect at its November meeting.

- The Bank of England adopted a more hawkish tone at its meeting in late September. Our economist Stephen Vogado has the details