The U.S. economy is experiencing an expansionary period many economists and financial analysts feel is sustainable for the immediate future. This means such factors as employment, gross domestic product, and wages will continue seeing favorable upward trends. While more people will be working and consumer spending will increase, there are some possible signs that could spell eventual trouble for the American economy. The four areas or bubbles that could spark a financial crisis are increases in credit card debt, student loans, car loans, and the rising stock market. Each of these four bubbles should be regarded as red flags that will have a severe impact on the American economy if one were to burst. Each has specific problems that could hamper growth for the American economy, possibly cause the other bubbles to burst, and perhaps lead to a recession. In order to understand these bubbles, some analysis is necessary.

Car Loans

Americans love their cars. A rite of passage into adulthood for many people in the United States is obtaining a driver’s license and then a new car soon after. Whether it is in the Midwest with pickup trucks or California with a new car to go to work or school, cars are an obsession with Americans. According to the United States Census Bureau, in 2016 85.4 percent of Americans used cars, trucks, or vans to commute to their jobs, or roughly 128.3 million people. In 2006, the number commuting to work was 119.9 million Americans. The problem is that unless the owners of these vehicles used cash to purchase their vehicles, regardless if they are new or used, they most likely took out a loan to finance their acquisition.

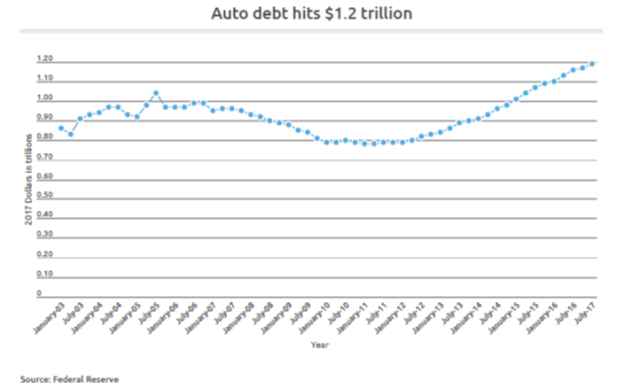

This leads to the problem of the ever-increasing amount of car loans. At the tail-end of 2017, Americans had $1.238 trillion in car loans which was an increase of $64 billion from September 2017. According to TransUnion, in the final quarter of 2017 the average auto loan contained a balance of $18,588. Experian stated that the average new vehicle loan reached a new record high of $31,099 in 2017. American consumers want to purchase cars and with auto dealers making it easier than ever to do so, the temptation is too great. This also means that dealers are using what they consider incentives to have consumers be able to afford new vehicles. For example, extending new vehicle loans to customers with little to no credit, no down payment, or high amount for a trade-in.

According to Edmunds.com, the average length of a loan on a new vehicle purchase went from 65.5 months in April 2013 to 69.2 months in 2018. Many consumers feel they are getting extra time to pay off the loan, but in actuality they are really paying more interest. Two decades ago, car loans were between three to five years. Americans are also buying bigger and more expensive vehicles such as SUVs, crossovers, and larger pickup trucks such as Ford F-130. To make matters worse, in 2017 consumers paid an average price of $35,176 for a new vehicle which is an all-time high exceeding the previous record of $33,532 in 2015. The bottom line is that consumers are buying more car than they can afford and there are signs of trouble up ahead.

The first sign of trouble is the delinquency rate on car loans. According to the New York Federal Reserve Bank in 2017 there were 6.3 million Americans who were late 90 days or more on their car loan payments which was up 400,000 from 2016. This sign of a 90-day delinquency is a dangerous red flag because when a borrower gets this far behind on loan payments, losing their vehicle to repossession is a very real possibility. The key idea to keep in mind is that with the U.S. economy at its current healthy stage, this number of delinquencies is high. The big concern among financial analysts and economists is what will the number look like when the American economy goes into a recession and unemployment increases. At that stage, many Americans will be without work and not be able to pay their car loans. Wilbert van der Klaauw, senior vice president at the New York Federal Reserve Bank warns that, “Delinquency rates among auto finance lenders are considerably higher and rising, especially for subprime borrowers, in part reflecting differences in underwriting standards.”

The Federal Reserve Bank of New York reported that at the end of June 2018, the U.S. auto loan delinquency rate of 90 days or more was at 4.17 percent compared to 3.92 percent in June 2017 and higher than the long-term average of 3.23 percent. If this tendency increases in the next year, lenders such as commercial banks and finance companies will see severe losses on their income statement and get stuck with new vehicles they must desperately sell in order to raise cash. This could also have a domino effect on asset-backed securities (ABS) such as bonds that have vehicle loans backing up the instrument. If new vehicle loans default, then these bonds will go bad by losing their ratings and eventual value. This could ultimately cause the bond market to take a serious hit. The news only gets worse. Fitch Ratings reported in May 2018 that the delinquency rate for subprime auto loans that exceeded 60 days attained a high of 5.8 percent, which was the highest since 1996 and went beyond the 5 percent rate set during the 2008-09 financial crisis.

Credit Cards

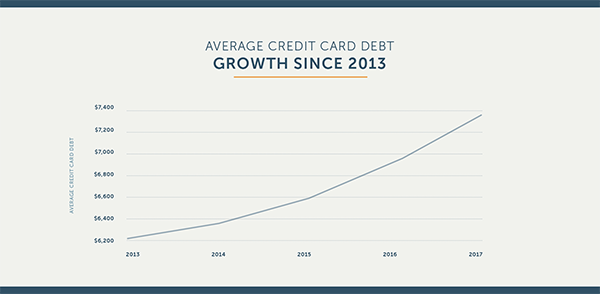

The United States is a consumer-based economy in which spending is a key function. The main method that Americans use to spend are credit cards which have good and bad aspects. The good aspect of credit cards is that they can provide a way to pay for goods and services in case of an emergency. Also, if an individual is short on cash, credit cards can provide the needed funds. The bad part of credit cards is that consumers can over-extend themselves and go on a spending spree that can cause serious financial long and short-term problems. Currently, Americans have approximately $1.041 trillion in credit card debt that exceeds the record set in 2008 of $1.02 trillion.

But a key question is how did American society get to this point of over $1 trillion in credit card debt? The financial crisis of 2008-2009 actually saw a decrease in consumer spending and credit card debt due to the serious recession facing the United States. Consumers cut back and threw away their credit cards. Credit card companies were still offering to extend credit but consumers were too spooked to spend. As the global economy gradually recovered, home foreclosures decreased, employment opportunities increased, and the American economy grew, Americans started spending again by using cash and credit cards. The problem is that Americans not only went back to the old dangerous habit of overusing their credit cards, but also exceeded their previous debt levels.

Another reason for increased credit card debt is the Bankruptcy Protection Act of 2005. This legislation made it much more difficult for individuals in declaring bankruptcy. While this law is beneficial to commercial banks and financial institutions sponsoring credit cards, the legislation made it impossible for credit card users to write off their excessive amount of debt and were stuck with a severe financial burden. The problem is that credit card users would run up their debt even further to pay for their daily living expenses to the point that they were stuck in an endless cycle.

Credit card use would not be so bad a problem if users paid off their balances immediately every month. These individuals are known as “transactors” who could be regarded as the ideal credit card users. However, there are also “revolvers” who carry credit card balances and pay monthly interest charges exceeding double-digits. If they miss a payment or are late, then there are late fees as well as increased monthly interest charges. This is a serious economic problem because if these “revolvers” lose their jobs and cannot pay their credit card bill, then they are stuck with a debt that will only increase significantly every month. The National Foundation for Credit Counseling reported that the percentage of American households having monthly revolving credit card debt has increased to 38 percent in 2018 after seeing a steady decline from 41 percent since 2010. This is a dangerous trend because more individuals could be having a harder time paying their credit card obligations. If the American economy goes into a recession, whether moderate or severe, the percentage of Americans having monthly revolving credit card debt could possibly exceed 50 percent.

The bottom line is that if the U.S. economy goes into a recession, then the credit card bubble could make a resounding pop that will have severe ramifications for commercial banks, financial institutions, and other issuers of credit cards such as retail stores.

Source: Federal Reserve Bank of New York

Student Loans

Perhaps the most worrisome and problematic of the three debt bubbles is student loans. Just like the ones mentioned in this article, each has serious economic consequences if the bubble bursts. But currently student loans are having a severe economic and financial impact on the American economy and can also have long-term ramifications.

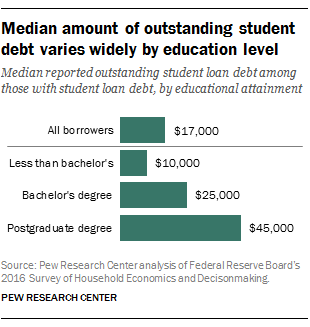

The total amount of outstanding student loans is $1.5 trillion for over 44 million Americans. This comes to approximately 25 percent of American adults that are in the process of paying off student loans. Currently, the average borrower of a student loan is $37,172 in debt as opposed to the average student loan of $17,172 in 2005. This will mean that borrowers will have 5, 10, 20, or 30 years to repay their obligation as long as they have a good paying job that will allow them to make their periodic payments. And speaking of student loan repayments, it has been estimated by the Federal Reserve Bank of Cleveland that the average monthly student loan payment has gone from $227 in 2005 to $393 in 2016. If this involves a payback period of 20 or even 30 years, the total loan repayment is significant. It is not unusual to hear of students having loans of between $5,000 and $200,000 by the time they finally graduate from school.

A key problem with student loans are defaults. Technically, a borrower defaults on a student loan if the payment is over 270 days late. Missing a student loan payment has a serious impact on the borrower’s credit score and will have long-term ramifications when applying for a home mortgage, personal loans, renting an apartment, or even applying for life insurance. According to the Brookings Institute, approximately 40 percent of borrowers enrolling in college in 2005 are expected to default on student loans by 2023. If the economy goes into a recession, it is not surprising if this rate increases by 10 to 20 percent. Currently, the student loan default rate (90 days or more in delinquency on payments) is 10.7 percent with new delinquent balances (30 days or more past due) at $32.6 billion and that is with the American economy in a relatively healthy state.

The dilemma with student loan debt is that it is no longer a problem confronting young people under 30. More borrowers are over the age of 50 and even 60. Recent statistics have shown that student loan borrowers 60 years of age and older increased by 1,256 percent since 2004. These individuals are either paying off their own student loans or have taken on the debt of their children who have finished school. From 2004 to 2017, student loan debt for people 60 years or older has gone from $6.3 billion to $85.4 billion. This comes to an annualized increase of 96.58 percent!! The scary part of this situation is that this age group is incurring debt that will sap their retirement income and perhaps make their long-term financial situation even worse.

Another group that has been hit hard by the student loan debt bubble are women. According to a study by the American Association of University Women (AAUW), women have almost two-thirds of the outstanding student debt in America which comes to nearly $900 billion in the middle of 2018. The AAUW analysis found that 41 percent of women undergraduates had student loans while only 35 percent of male undergraduates were burdened with debt. Across the board, from associate degrees to doctoral degrees, women were deeper in debt. The problem only becomes worse since women take longer to repay their student loans at a slower rate than men due to the gender pay gap. Because women make less income than men, they have a lesser amount to repay their student loans. Also, it severely hurts their chances of saving money to purchase a home or even going back to school for further education. The good news is that 57 percent of bachelor’s degrees from American colleges and universities go to women but the bad news is that they have heavier student loan obligations than men by $2,740.

If the student loan bubble were to burst, then borrowers would be in a very deep hole since they are stuck paying their debt obligations with no help from employers or the state or federal government. This would mean putting off having a family, getting married, buying a home, or even being able to change careers by going back for further education and training.

The Stock Market

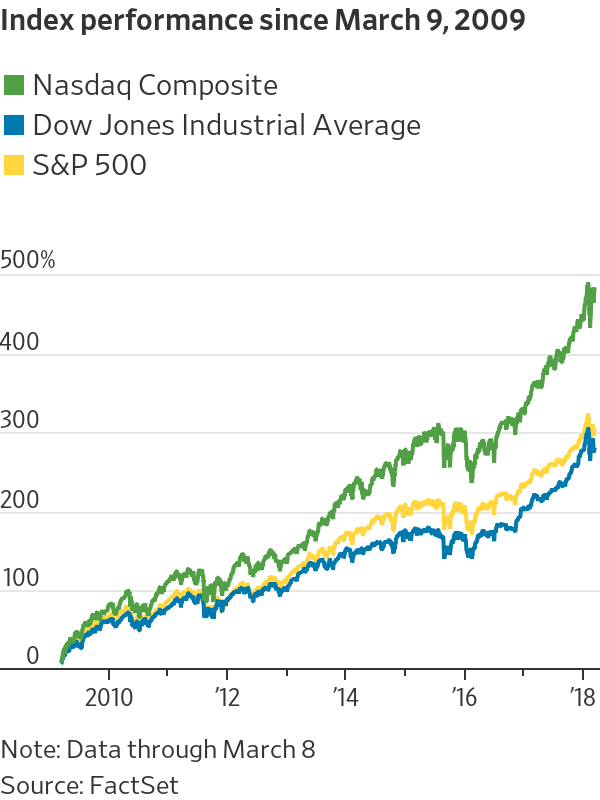

Perhaps the bubble that has many economists and financial analysts worried but the average investor quite content is the current state of the stock market. Despite recent volatility the market is experiencing it is still very high and has recovered from the crash due to the Financial Crisis of 2008-2009. The Dow Jones Industrial Average sank to 6,547 in March 2009 and eventually rebounded to surpass 11,000 in April 2010. The Dow went above 21,000 in mid-2017 and currently it is over 25,000, as of November 2018. But how high will it go or is it bound for a downward swing? While American households are wealthier now than they have been in a while, this euphoria could soon be replaced by investor anxiety when the stock market bubble bursts.

A bubble can best be characterized as an economic phase in which there is a rapid increase in asset prices eventually followed by a sharp contraction. Regardless of the type of market, whether stocks, real estate or tulips, a bubble is the result of assets surging in value in which there is no real basis its financial fundamentals and is actually moved to unknown levels by exuberant, and some would say irrational, market behavior. The problem occurs when there is a sudden lack of investors who, for whatever reason, refuse to purchase the asset at the highly inflated price and then a huge sell-off materializes thus resulting in the bubble either eventually deflating or even violently bursting. Among the problems with asset bubbles is attempting to recognize that the market is in that state, buying assets at overvalued prices, getting caught up in irrational euphoria, and wondering how much monetary value was lost when the bubble burst.

The resulting burst of an asset bubble will occur either through a correction or a crash. A market correction occurs when the market tries shake up extremely exuberant investors who feel that the party will never end and that the market will continue its upward movement without any end in sight. Corrections occur when there is an approximately 20 percent loss in market value. Here the market will readjust itself to a new normal. A correction may result in the market eventually making a revised upward movement or possibly an economic recession. A crash happens when there is a large drop in market value causing investors to flee by becoming liquid or changing their asset into ready cash. The problem with a crash is that investors are now in a panic selling mode and are selling their holdings in a severely declining market resulting in massive monetary losses in which they will most likely never recoup. The long-term ramification with a crash is often an economic depression. The problem currently is that with the market making these up and down movements is it is difficult to tell whether there will be a crash or a much-needed correction.

There are a number of reasons why the stock market is currently in a bubble. First, interest rates have been at historic lows, from 0 percent to near 0 percent as the Federal Reserve has done what it can to keep the American economy in a recovery mode from the Great Recession of 2008-2009 and in a constant state of economic strength. Second, because of low interest rates, consumers, firms, and governments have been encouraged to borrow in order to spend more. This means more money being used to purchase goods and services which causes providers to have higher profits which the stock market approves of in the form of increased asset values. Third, due to the collapse of the residential real estate market, investors took money out of their first and second homes and used those funds to purchase stocks. When too much money started chasing too few stocks, asset values in the Dow and the S&P 500, to name a few, were bound to go up. Fourth, inflation has been relatively low, never going higher than 3 percent providing for a stable American economy and investors having one less worry regarding the value of their money. Fifth, savings rates have been extremely low. Interest rates for savings accounts and certificates of deposit (CDs) have been low for about ten years and savers have been looking for alternatives that could give them higher returns. When they could not find those higher returns in bonds, money market instruments, or CDs then stocks were their only viable alternative. Lastly, the Trump tax plan was rewarded by Wall Street with higher stock prices. Wall Street saw the plan as a way to have more cash available for firms from their overseas subsidiaries and brought back to the United States for more stock buybacks and increased dividends for shareholders.

The key problem with a stock market bubble is trying to predict accurately when it will either burst or go into correction mode. When a crash or correction does occur, then everyone will know it. But until then, investors are enjoying the ride and not worrying about when they must pay the piper.

Percentage gains since the start of the current bull market

Not a question if the bubble will burst, but when

The bubbles described here are real and a problem for economists, financial analysts, and policymakers. They must try to get a handle on them and prepare for the time when they burst. But they key question is which black swan or financial, economic, or political event will occur that causes the bubbles to burst and what it will mean for the American economy. Should action be taken to prevent a bursting of even one bubble or should all of them be dealt with and how?

Arthur Guarino is an assistant professor in the Finance and Economics Department at Rutgers University Business School teaching courses in financial institutions and markets, corporate finance, investments, and financial statement analysis. The first half of his career was spent in the financial services industry working for corporations such as TIAA-CREF, Met Life, and The Bank of New York. He writes articles dealing with finance, economics, and public policy.

Arthur Guarino is an assistant professor in the Finance and Economics Department at Rutgers University Business School teaching courses in financial institutions and markets, corporate finance, investments, and financial statement analysis. The first half of his career was spent in the financial services industry working for corporations such as TIAA-CREF, Met Life, and The Bank of New York. He writes articles dealing with finance, economics, and public policy.

Sample Report

5-year economic forecasts on 30+ economic indicators for 127 countries & 30 commodities.