On 9 September, France’s prime minister, François Bayrou, quit after losing a confidence vote that toppled his government. Shortly after, President Emmanuel Macron appointed a new prime minister, Sebastien Lecornu: He will be the second prime minister in less than a year and the fifth in two years under Macron’s presidency. The country’s problems remain: France has the highest fiscal deficit in Europe and a highly fragmented parliament.

One objective, many views: There is broad political consensus on the need to reduce France’s fiscal deficit—the highest in the Euro area and almost double the European Commission target of 3.0%—but sharp disagreements remain over how to achieve it. Left-leaning parties advocate for higher taxes on the wealthy, while the center-right opposes such measures, as it would undermine President Macron’s pro-business agenda. That said, Lecornu should avoid reopening the pension reform debate if he wants to keep his seat—his predecessors were ousted over this issue. France is now the only developed economy where the over-65 population enjoys higher average incomes than the working-age population, making pension reforms an especially sensitive subject.

Pouring gasoline on the fire: While political debates continue in parliament and across social media, mass protests against budget cuts have once again filled the streets. At the same time, Fitch Ratings has downgraded France’s sovereign credit rating to its lowest level on record, further intensifying the pressure on the country’s fiscal outlook. In this context, Lecornu is expected to send a full budget draft to parliament by October 7.

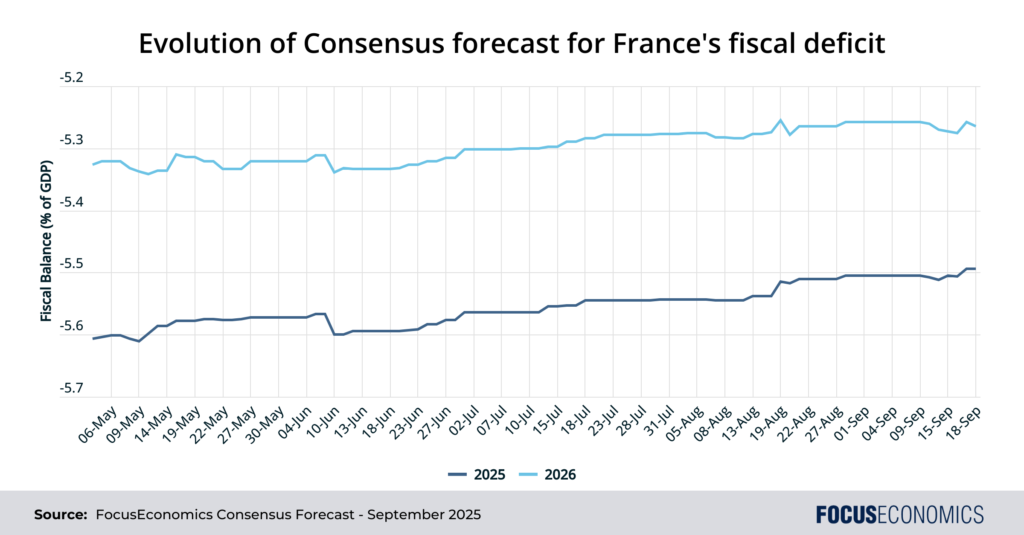

What our panelists think about the future fiscal deficit: Over the past months, our panelists have revised their forecasts to project a slightly narrower fiscal deficit in 2025 and 2026. Nevertheless, the fiscal deficit in both years is projected to remain well above the European Commission’s 3.0% of GDP threshold, as the country’s extensive welfare-driven public spending will take time to recalibrate. For context, France has not recorded a fiscal surplus since 1974—the year Richard Nixon resigned over the Watergate scandal and Muhammad Ali defeated George Foreman.

Insight from our analysts:

Commenting on future political instability, ING analysts stated:

“If […] the Prime Minister manages to keep his position, it will probably be at the cost of less rigorous fiscal consolidation, effectively postponing the promised budgetary consolidation. However, it remains possible that Mr Lecornu will not succeed in forming a viable coalition. In this case, Macron could appoint a new Prime Minister, but the chances of success would not be any higher. This could ultimately lead to another dissolution of the National Assembly. In our view, the probability of Macron resigning is very low at this stage. Nevertheless, instability will remain at least until the 2027 presidential elections.”

Moreover, EIU analysts added:

“The forthcoming discussions between Mr Lecornu and other parties do not look promising. His political survival is contingent on obtaining parliament’s confidence and then maintaining it for long enough to get a budget passed that reduces the deficit. He will also need to find a way to soothe public tensions and de-escalate the protests. With opposition parties seemingly unwilling to co-operate with a new government, these tasks may prove to be impossible. There is a high risk (45% probability) that Mr Lecornu’s government collapses prematurely, before the next presidential election in April 2027.”

Our latest analysis

The U.S. recorded stronger-than-expected retail sales in August.

In August, China’s economic activity was below market expectations.