Overview of U.S. tariffs and their implementation

Since taking office in January, U.S. President Donald Trump has threatened, implemented and backtracked on tariffs at a dizzying rate, making keeping pace with the latest developments tough. As of 25 July, the United States currently has 25% tariffs in place on most goods from Canada and Mexico that don’t comply with the USMCA free trade deal. A baseline global levy of 25% is also in place on cars and car parts, and 50% tariffs have been imposed on aluminium and steel. Trump briefly hiked tariffs on China to triple digits in April before rowing back, though tariffs on the country are still notably above those in the Biden era. For up-to-date cross-market projections, visit our Consensus Forecast.

Summary of the tariffs imposed on the United States by other countries

Since March, Canada has imposed retaliatory tariffs worth around USD 22 billion on U.S. imports, and China retaliated with a 10% tariff on U.S. goods—down from the triple-digit figures briefly seen earlier in the year. Other countries have so far preferred engagement with the Trump administration rather than direct tit-for-tat tariff confrontation.

The economic effect of Trump’s tariffs on the U.S. economy to date

The impact of tariffs on inflation

Likely due to a mix of inventory building and firms’ desire to protect sales, past tariff hikes have taken longer than expected to trickle through to U.S. consumer prices. U.S. inflation fell from 3.0% in January to 2.4% in May, though a rise back to 2.7% in June suggested some incipient impact from higher import levies, an effect which should intensify in the second half of the year.

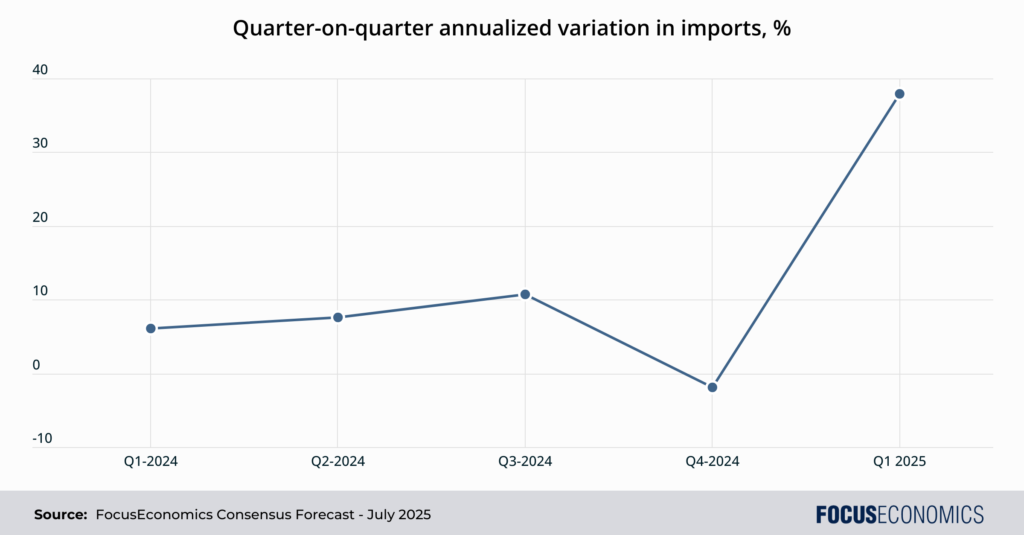

The impact of tariffs on trade

The impact on trade has so far been largely distortionary rather than destructive. U.S. imports jumped 38% in quarter-on-quarter annualized terms in Q1, the highest rate since lockdown restrictions were lifted in 2020, as firms rushed to bring forward shipments ahead of impending tariffs. This effect is expected to have unwound in Q2, with panelists penciling in a sharp decline in imports compared to Q1. U.S. export volumes were broadly stable in Q1 and are expected to have remained so in Q2, likely weighed on by greater trade frictions with Canada and China.

The impact of tariffs on GDP

The U.S. economy contracted for the first time in three years in Q1 2025, largely due to trade distortions as firms front-loaded imports. However, tariff talk also knocked consumer confidence, which appeared to weigh on private spending. The unwinding of the import boom should have supported a return to GDP growth in Q2, though readings for private spending and investment were likely considerably weaker than in recent years.

In short, while tariffs are taking the shine off the U.S. economy, they have yet to cause a serious downturn. The economy continues to have things in its favor, chiefly ongoing solid employment growth and a dynamic tech sector.

The impact of tariffs on the exchange rate

The U.S. dollar index has weakened around 10% so far this year. This is partly due to market concerns over the economic fallout from tariffs, but also because of worries over fiscal largesse—made more acute by the recent passage of a bill in Congress that will likely add trillions of dollars to the public debt pile. Trump’s attacks on pillars of U.S. economic success—especially universities and the Federal Reserve—have further unnerved investors and hurt the dollar.

Positive tariff effects on the U.S. economy

It’s hard to find many macroeconomic positives to take from Trump’s tariff hikes, though fiscal policy is arguably one. Tariff revenue has already jumped to close to USD 30 billion per month from the sub-USD 10 billion figures seen before Trump’s second term, and will likely rise further as “reciprocal” and other sector-specific tariffs fall into place. The non-partisan Congressional Budget Office estimated that once factoring in the hit to GDP from the levies, revenue from tariffs implemented up to mid-May could reduce total federal deficits by USD 2.8 trillion over the next ten years. That said, this would still be tiny compared to the overall size of the deficit, which is currently running at close to USD 2 trillion each and every year.

The future economic outlook

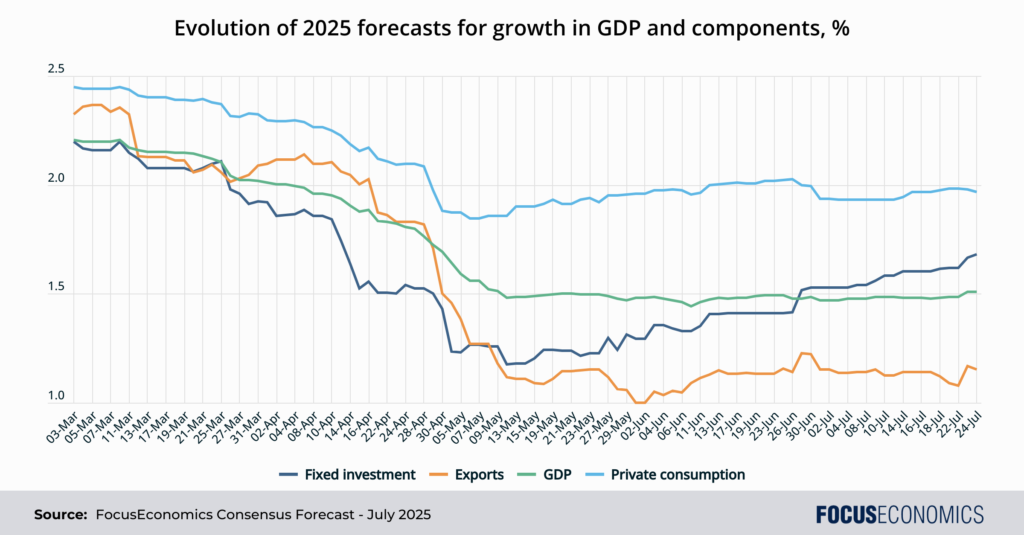

Since the first tariffs were implemented on Canada and Mexico in March, our panelists have cut their forecasts for 2025 GDP growth and the key components that comprise it. Private consumption will be dampened by higher inflation, fixed investment by uncertainty over where tariffs will eventually end up, and exports by expected retaliatory tariffs. That said, since hitting nadirs in May–June, forecasts have since been revised up slightly. This is likely because the U.S. economy has proved somewhat more resilient than expected so far this year, with employment growth holding up, consumer confidence stabilizing, and inflation taking longer than expected to feed through to prices. That said, panelists could revert to downgrades if tariffs on important trading partners are ratcheted up in the second half of the year.

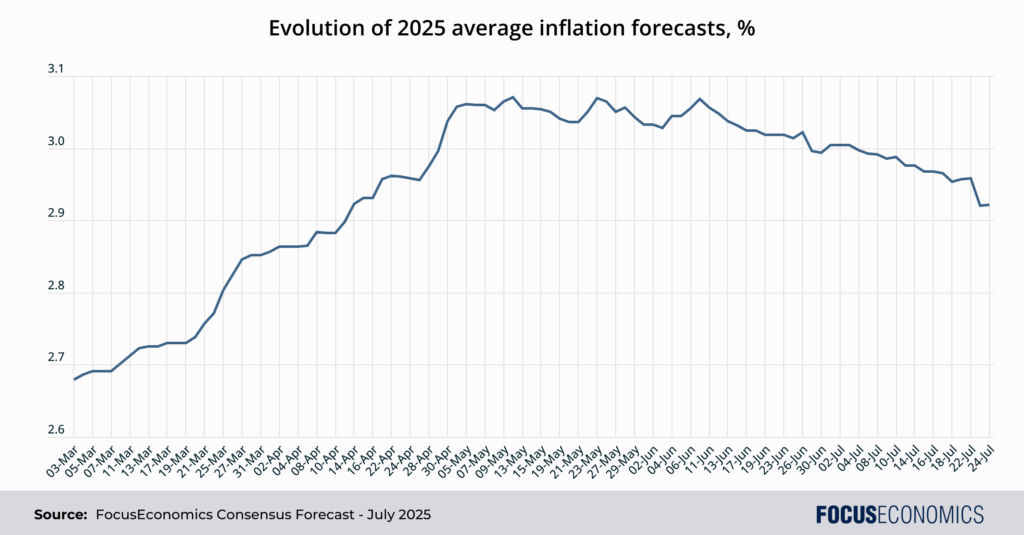

A similar pattern is evident with inflation. After hiking forecasts rapidly in April and May, panelists have since trimmed them in light of the slow pass-through of higher tariffs to consumer prices, as the graph below indicates.

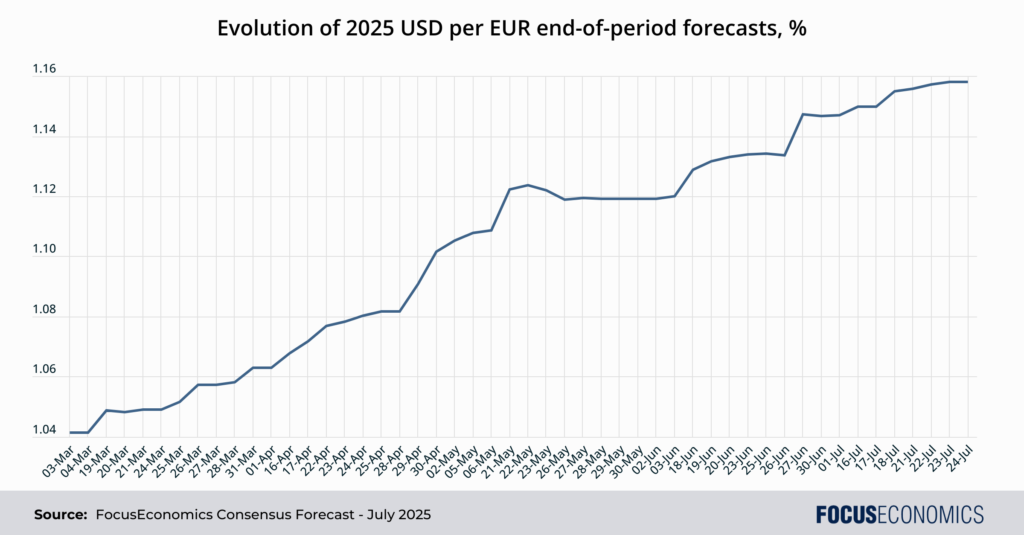

One daily forecast that has shown a consistent linear trend is that for the U.S. exchange rate—likely in part as the rate is determined by many factors other than tariffs. Our panelists have continued to downgrade their projections for the dollar in recent months due to a mix of ongoing tariff turmoil, fiscal profligacy and institutional uncertainty.

The bottom line: The U.S. can still count on its vast domestic market, world-beating technology sector, entrepreneurial mindset, flexible labor market, laissez-faire business conditions and safe-haven status to gird economic activity despite higher trade barriers. As such, tariffs are currently a nuisance but not a tragedy for the U.S. Unless Trump’s policies undermine more of the economy’s key strengths, things are likely to stay that way.

Insight from our analysts:

EIU analysts said:

“We continue to expect the US to retain a cautious approach to future tariff adoption, given the expected blowback on to the US economy and financial markets if Mr Trump were to adopt his tariffs as threatened. At the very least, this possibility will keep the US open to negotiations.”

On the recent EU-U.S. trade deal, ING’s Carsten Brzeski commented:

“Looking ahead, at face value [the] deal falls in line with our base case scenario of an effective tariff rate on European goods of close to 20%. However, we also know that a trade deal is only done and dusted when everyone has signed it. In the European context, this still means a European Parliament and all national parliaments.”

Our latest analysis:

Malaysia’s economy surprised markets to the upside in Q2.

U.S. retail sales rebounded in June despite the tariff turmoil.