A key hurdle for forecasters is determining the impact of lockdowns in conjunction with various levels of fiscal and monetary stimulus. Furthermore, the impact will depend on countries’ economic structure. Economies driven predominately by domestic demand will likely experience sharp declines in 2020, followed by increases in activity over the next couple of years. Meanwhile, resource-dependent economies will be hit twice from weak global demand for commodities.

Determining the shape of the economic recovery will be important for households, businesses and investors, as well as, of course, governments and policymakers steering their economies through unchartered waters. Below are the possible shapes the global recovery could take, our panelists’ Consensus Forecasts, as well as some of their insights.

- The V-shaped recovery

In most cases when economies are faced with a temporary exogenous shock, the recovery is a classic V shape. This is a sharp fall in output with a clearly defined trough followed by a strong recovery, typically spanning over the course of a year or so and induced by one-off disturbances to economic output with minimal long-term implications. The V-shape is the strongest form of recovery from a downturn.

Commenting on the V-shaped recovery, analysts at Handelsbanken noted:

“This scenario is based on there not being any setbacks in the spread of the infection, that the uncertainty among households and companies eases quickly, and that governments across the world implement packages of stimulus measures to kick-start the economy once the pandemic peters out. At the same time, we assume central banks will support the recovery by pursuing a very expansionary monetary policy in the next few years. […] In this scenario, global GDP drops by 1.5 percent in 2020 and grows by no less than 6.5 percent in 2021.”

- The U-shaped recovery

The trajectory of a U-shaped recovery has a sharp fall in activity with a longer downturn period, which tends to last between one and two years. The global financial crisis, for example, resembled a U-shaped recession. Applying this shape to the current recession implies a recovery by early to mid-2021.

Commenting on the probable economic recovery for the U.S. economy, analysts at JPMorgan noted:

“We have shifted our base case from a rapid “V-shaped” rebound to a more measured “U-shaped” recovery since we now see a more gradual resumption of activity after social distancing measures begin to ease. We expect GDP to contract by 3.2% in 2020 and not to return to its prior peak until 2022. Even in the U-shaped recovery, we see GDP rebounding faster than it did following the 2008–2009 Global Financial Crisis, and a lot faster than during the Great Depression. In the end, the virus represents an “exogenous” economic shock, from which the recovery should be swifter compared to “endogenous” recessions resulting from excess leverage in the financial and household sectors.”

- The W-shaped recovery:

The W-shaped recovery—commonly known as a double-dip recession—is essentially two short-lived downturns in quick succession. For instance, the U.S. fell into recession in 1980, but by 1981 the economy was experiencing exceptional growth—mimicking a V-shaped recovery. However, the economy fell back into recession in 1982 after the Federal Reserve raised interest rates to stave off inflation, before recovering again in 1983.

The W-shape recovery could reflect a second wave of the virus if economies reopen too soon, with subsequent lockdown measures tipping the world back into recession.

Commenting on the W-shaped recovery, analysts at ING noted:

“This is a slight variation of our base case scenario […] with a gradual easing of lockdown measures in May and June. However, in this scenario, the virus returns in the autumn and despite more widespread testing efforts and contact tracing, the new spread pushes most economies back into lockdown […] For indicative purposes, we’re assuming it will take until April 2021 before the virus is back under control and economies, as well as societies, begin to return to normality. This is a ‘W-shaped recovery’. GDP growth would be lower in 2020 but higher in 2021 than in our base case scenario. However, it may well take until late-2022 before most economies have returned to their pre-crisis levels.”

- The L-shaped recovery

The L-shaped recovery represents a deep depression in which the economy takes several years to recover. Historical examples include Japan’s lost decade of the 1990s or the U.S. Great Depression in the 1930s. The L-shape is the worst-case scenario; the hit to the labor market would be unprecedented and public and household debt levels would rise significantly. This scenario would likely represent the single-biggest hit to global economic activity in modern history.

Commenting on the possibility of an L-shaped recovery, analysts at JPMorgan noted:

“This scenario would likely include more corporate bankruptcies and insufficient policy support. The most likely path to the L-shaped scenario is where the virus never really gets “under control”—every time social distancing is lifted, another wave of outbreaks emerges, making it very difficult for businesses to sustain operations and for consumers to return to pre-shutdown behavior. Eventually, “herd immunity” or a vaccine may end the spread of the virus, but each is a long way off (1–2 years at the earliest). This scenario is more like a “depression,” where even by 2022, activity remains well below 2019 levels, and unemployment lingers at the highest levels since the Great Depression.”

- Other possibilities

As well as the shapes mentioned above, there are other paths the economic recovery could take, particularly given the unprecedented situation economies are currently facing. The checkmark, or Nike-swoosh-shaped recovery, is one example. This outcome would translate into a mixture of both the V-and U-shaped recoveries, representing a slow and steady rebound in the global economy.

Commenting on the U.S. and Canadian economies, Beata Caranci, chief economist at TD Economics, noted:

“Canada’s real GDP will not eclipse pre-crisis levels until the second quarter of 2022 (a full two years from the shock), while the U.S. may get there a quarter or so earlier. The recovery in the level of activity is very much U-shaped, even though the growth rates give the impression of a V. This causes some confusion with clients or in how recoveries may be portrayed in the media. For this reason, some are characterizing the cycle as looking like the Nike Swoosh, marking a compromise between the two shapes.”

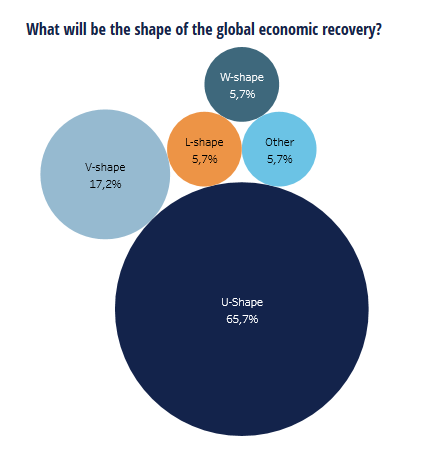

- FocusEconomics panelists’ expectations

We have surveyed our panelists on their expectations of the shape of the economic recovery over several months. Most of our panel has expected a U-shaped recovery since late March, with a V-shaped recovery considered the second most viable option.

As of 6 May, roughly 66% of our panel expects a U-shaped recovery, while approximately 17% projects a V-shaped recovery. This suggests the Consensus forms a checkmark-shaped rebound in activity but leaning more towards a U rather than a V shape. Nevertheless, risks are skewed to the downside, and about 10% of our panelists project either a W- or L-shaped recovery in global economic activity.