The Iran-Israel conflict remains a major risk for the world economy: The ceasefire between Iran and Israel came quickly, ensuring that the world will—for now—escape the worst-case scenario: A surge in oil prices that shoves up inflation, in turn further hitting a world economy that’s already reeling from Trump’s tariffs.

In addition, last week media reported that U.S. envoy Steve Witkoff would meet with Iranian Foreign Minister Abbas Araghchi in Oslo this week to restart nuclear talks, leading to a decline in oil prices.

According to our panelists, it would, however, be premature to act as if the conflict had just been a bad dream. Like a fresh wound, the conflict could reopen at any time, the possible consequences of which are described by analysts at Fitch Solutions:

“In the event of a re-escalation in tensions which leads to the closure of the strait [of Hormuz], energy importers with high dependence on the Strait of Hormuz and substantial energy subsidies – such as India, Egypt, and Thailand – are especially vulnerable to oil supply disruptions and price shocks, particularly if they have limited fiscal and monetary policy space.”

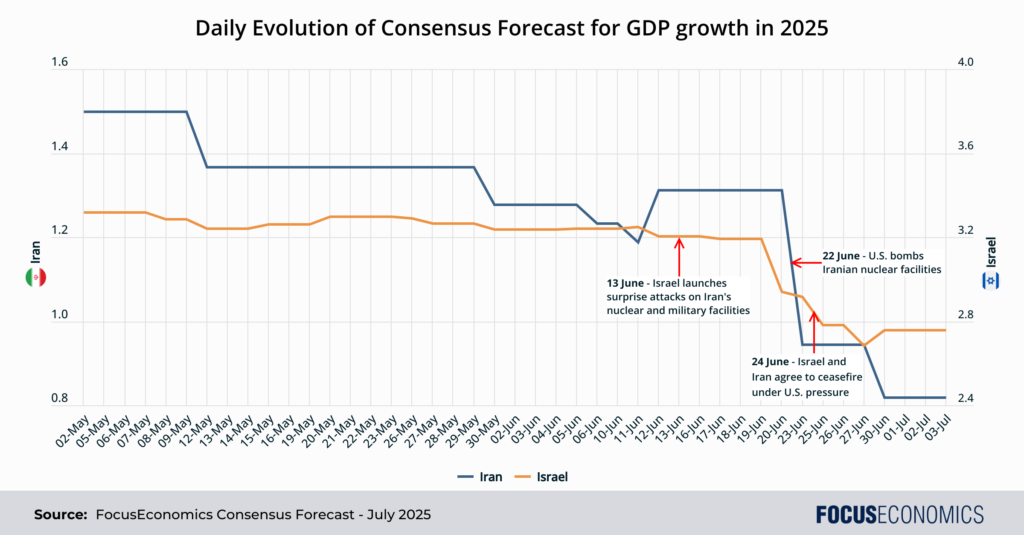

The economic outlook for both Iran and Israel has worsened: As for Iran and Israel, the threat of nuclear bombs hangs above the economies of both like the Sword of Damocles. The dust may have settled on the conflict for now, but the psychological damage to both economies will linger. This can be seen in the below graph, which highlights the Daily Updates to our Consensus Forecast, available via our data platform:

The economic uncertainty generated by the conflict is likely to lead consumers to bolster precautionary savings, tourists to cancel their travel plans, and businesses to freeze investment. As a result of this and the war in Gaza, Israel’s economy is set to undergo its weakest streak of growth in 2022–2025 since the early 2000s, when the economy was ravaged by the Second Intifada and the dot-com crash. Iran, meanwhile, is set to barely eke out growth this year, with its oil sector likely to suffer an additional blow from tighter U.S. enforcement of sanctions.

The future path of the conflict remains hazy: For now, it seems likely that the Iranian regime will survive. The real question is whether it will accept a nuclear deal or refuse one. As commented by EIU analysts:

“The outlook remains highly fluid and uncertain, but our baseline view is that, although it will engage in nuclear talks, Iran seems unlikely to accede to US demands to give up its ability to enrich uranium. Talks are likely to drag out, with the US reluctant to resort to (and act on) another time-bound threat of new military strikes if no satisfactory deal is reached. Depending on his assessment of the damage inflicted on Iran’s nuclear programme, Mr Trump may decide that there is no pressing need for a new nuclear deal.”

More insight from our analysts:

Goldman Sachs economists said:

“A temporary disruption of energy supply through the Strait of Hormuz would likely lower global growth by over 0.3pp and raise headline inflation by 0.7pp. Effects on global core inflation in these scenarios should be small (<0.1pp). Both the growth hit and inflation boost would be larger in the event of a sustained closure of the Strait of Hormuz.”

Our latest analysis:

Argentina’s GDP in Q1 grew at a robust rate, suggesting Milei’s reforms continue to bear fruit.

Japan’s core inflation rate rose in May, with rice prices surging over 100%.