Bond yields in major advanced economies have been on the up so far this year. Japanese 30-year bond yields have hit record highs so far in July, while 10-year yields have reached levels not seen in over a decade. In the same month, UK long-term yields climbed to levels last seen in 1998, with 10-year yields also approaching their highest levels since before the global financial crisis (GFC). Moreover, in the U.S., long-dated bond yields spiked in May to their highest since 2007, while 10-year yields have hovered near GFC-era levels since January. This reflects a broad loss of appetite for the long end of the yield curve. Why is this happening? What’s going on in global credit markets?

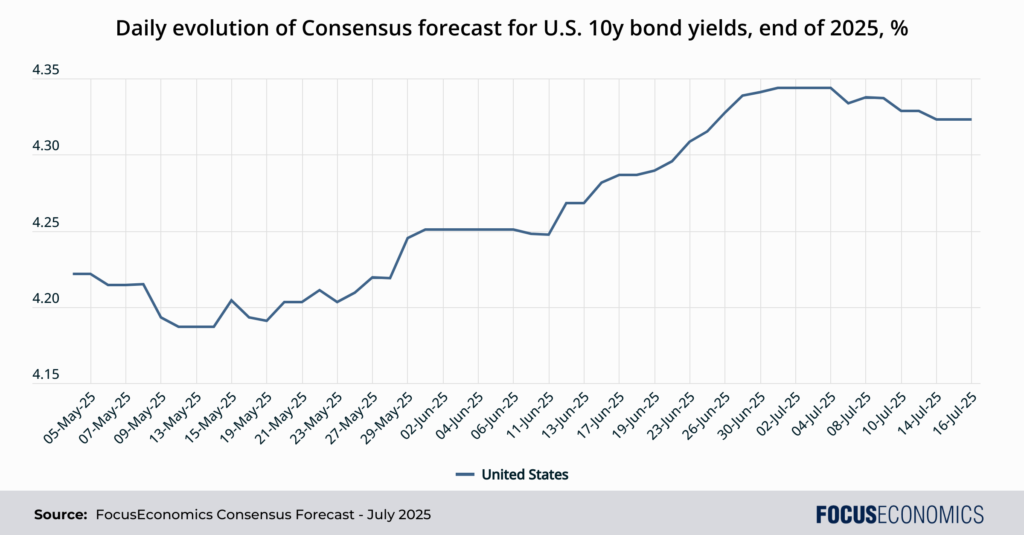

Erratic U.S. policy: In the U.S., rising protectionism is expected to bolster inflation and hinder economic growth. Moreover, Trump’s erratic policies have fueled uncertainty, reinforcing doubts about fiscal stability, as highlighted by Moody’s credit rating downgrade in May. As a final blow, the recently passed “One Big Beautiful Bill” is projected to add USD 2–5 trillion to America’s enormous USD 36.2 trillion public debt pile over the next decade. These developments have raised concerns about debt sustainability and pressure on Treasury financing. The result? Higher borrowing costs and an intensified push upward on bond yields.

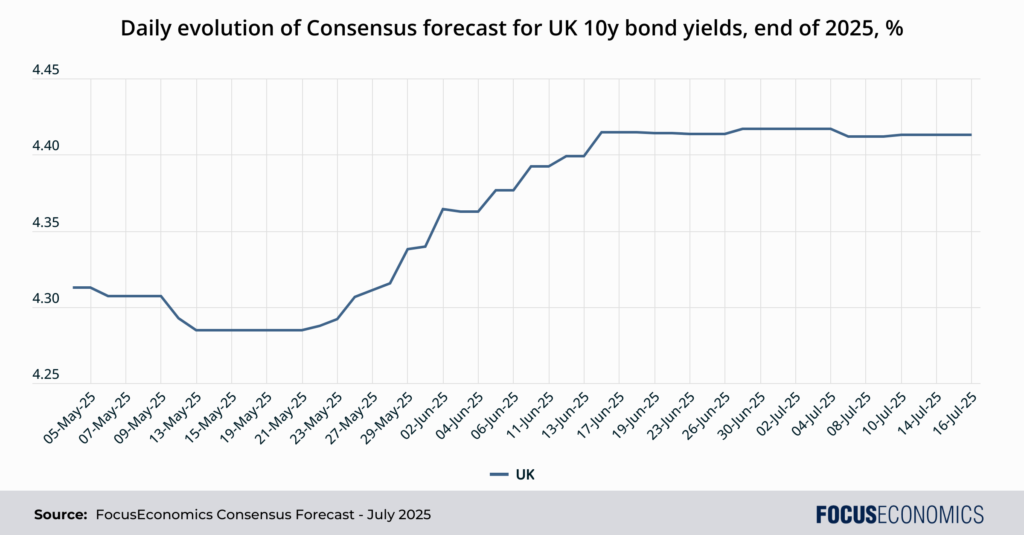

Markets request fiscal discipline in the UK: In early July, global bond markets reacted sharply to UK Prime Minister Keir Starmer’s failure to openly support Chancellor Rachel Reeves in Parliament plus the government’s failure to secure meaningful reforms to cut the welfare bill. The developments caused 30-year gilt yields to rise, a reaction seen as a warning call to the UK government. The UK faces a fragile fiscal position—with one of the highest deficits among developed economies—and skepticism over how it will finance its spending plans, raising the prospect of tax increases and looser fiscal rules in the autumn budget. Moreover, stubbornly high inflation—which in June exceeded market expectations—and underwhelming economic growth further raised concerns about government debt sustainability.

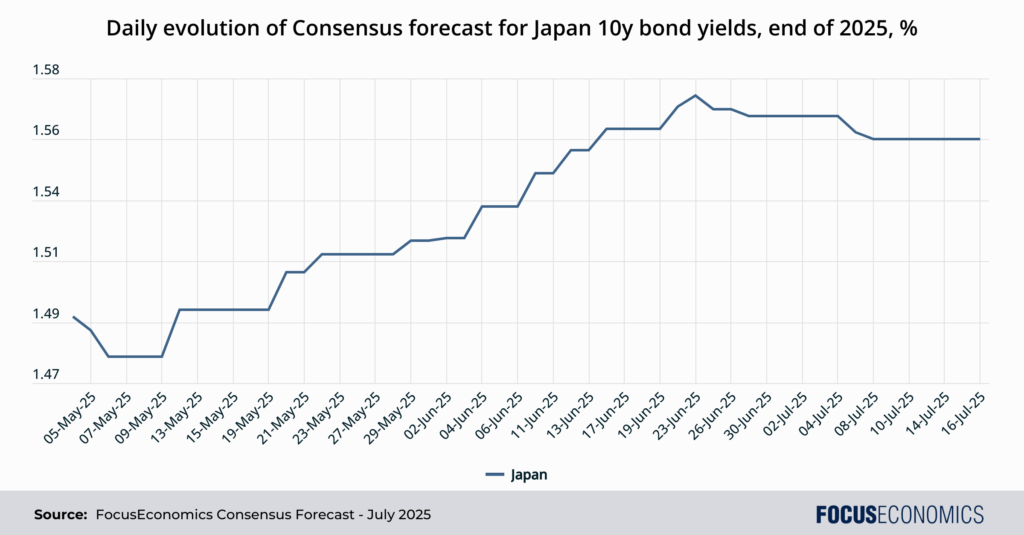

All eyes on Japan: The world’s fourth-largest economy is a special case, as the rise in long-term yields appears driven by structural factors. Japan has the world’s highest share of people aged 65 and over, and this has prompted institutional investors such as pension funds to rebalance their portfolios towards shorter-term bonds. Additionally, rising inflation has pushed investors to seek higher-yielding assets. This has possible global implications as higher long-term yields in Japan, the world’s second-largest creditor, could spark a wave of capital repatriation with Japanese investors pulling funds from the U.S.

Our panelists raise their forecasts: As part of Daily Updates to our Consensus forecasts, every day our panelists send us their latest forecasts for 10-year yields. Since May, our panelists have raised their forecasts for this maturity. So far, the increase in debt-servicing costs has been moderate, but it is a trend that warrants close attention; if the upward trajectory persists, it could pose serious risks to the financial system. The bond market is the bedrock of global finance and government funding: Sustained stress here could erode the value of private-sector assets, trigger credit downgrades, sour investor sentiment, crowd-out private investment and strain public finances, ultimately leading to macro-financial instability and weighing on global growth.

Insight from our analysts:

On future possible implications of rising yields for long-term Japanese bonds, Goldman Sachs analysts commented:

“We would expect that a return to gradual BOJ hikes should begin to reanchor the long-end, driving higher 5y and 10y yields vs 30y, coupled with a cautious but continued stance on QT led by the belly. And while recent volatility is unlikely to be sustained, the move in 30y JGB yields serves as a warning that bouts of weakness in global long-end bonds are a pattern not an aberration.”

On future U.S. bond yields, EIU analysts stated:

“Bond yields, especially at the long end of the yield curve, will remain elevated in the next few years as US inflation rises and investor confidence in US financial institutions weakens, pushing up interest costs. Although the US is capable of meeting its debt obligations, political tensions remain a cause for concern. The debt limit was lifted by the recently passed budget bill, avoiding the previously looming deadline to raise the cap and extending the US’s ability to borrow into 2028.”

Our latest analysis

The United Kingdom’s economy records the quickest inflation since January 2024 in June.

In China, economic growth lost traction in Q2 but beat expectations.