Sub-Saharan Africa continues to dominate the list of poorest countries: When looking at our Consensus Forecasts for the economies with the lowest GDP per capita (in U.S. dollars, current market prices) in 2026, one thing jumps out: 18 of the 20 poorest are from Sub-Saharan Africa (SSA). The non-African nations in the top 20 are the conflict-riven countries Afghanistan and Yemen. Though SSA has been the second-fastest growing economic region after Asia in recent years, exceedingly high population growth—over 2% per annum—means that GDP per capita has risen far more slowly. Moreover, factors such as extreme weather, political turmoil—the continent has experienced a host of coups since 2020—and insecurity continue to stop SSA from reaching its full potential.

Which are the Poorest Countries in the World?

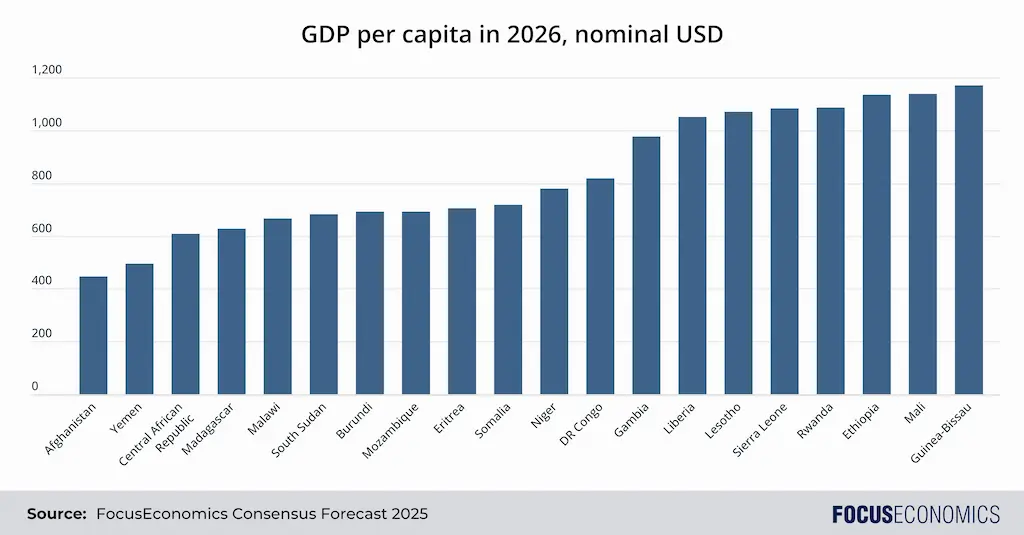

Below is a list of the top 20 poorest countries in the world:

1st poorest country: Afghanistan

GDP per capita 2026 Consensus Forecast: USD 445

Afghanistan’s poverty stems from decades of conflict, including foreign invasions, civil wars, and insurgencies. Continuous instability has ravaged infrastructure, undermined institutional development, and deterred foreign investment. The productivity of the agricultural sector, on which most Afghans rely, is low due to outdated farming practices, water scarcity, and land degradation. Widespread corruption and a weak central government further hamper development, with the economy remaining heavily dependent on international aid. Additionally, the Taliban’s return to power in 2021 has led to the isolation of Afghanistan from global markets and financial systems, stifling the economy and exacerbating humanitarian crises. Our panelists expect only muted GDP growth next year, notwithstanding some support from infrastructure projects linking Afghanistan to Central Asian neighbors.

2nd poorest country: Yemen

GDP per capita 2026 Consensus Forecast: USD 493

Yemen has been beset by civil conflict for over a decade, with the country divided into different factions, chiefly the Houthi-rebel-dominated northwest and the Arab-backed Southern Transition Council in the south. The conflict has ravaged infrastructure and caused mass population displacement; as a result, GDP per capita next year is projected to be only around a third of its pre-crisis level.

3rd poorest country: Central African Republic

GDP per capita 2026 Consensus Forecast: USD 609

The Central African Republic (CAR) is plagued by instability and conflict. Armed groups control large swathes of the country, undermining central government authority and creating a constant state of insecurity. Frequent clashes involving these groups have displaced millions, destroyed infrastructure, and prevented economic development. Though the CAR is abundant in natural resources like diamonds, gold and timber, these assets are often exploited by corrupt officials or rebel groups, with little benefit to the general population. The lack of basic services like education, healthcare and reliable infrastructure further entrenches poverty.

4th poorest country: Madagascar

GDP per capita 2026 Consensus Forecast: USD 628

Madagascar’s low GDP per capita is tied to multiple factors. Firstly, chronic political crises, including coups and contested elections, have weakened institutions and handicapped development efforts. Secondly, deforestation and unsustainable farming practices have degraded the country’s biodiversity, reducing agricultural productivity and increasing vulnerability to natural disasters like cyclones. Thirdly, Madagascar’s geographical isolation from major markets, combined with poor infrastructure, makes trade and investment difficult. Finally, a reliance on low-productivity agriculture and the limited diversification of industries have kept the economy stagnant: Just four goods—cloves, cobalt, nickel and vanilla—account for close to half of all goods exports. The upshot is that nearly 80% of the population lived in extreme poverty (that is, had income of less than USD 2.15 per day) in 2023—the highest rate in the world.

5th poorest country: Malawi

GDP per capita 2026 Consensus Forecast: USD 667

Malawi’s poverty is driven by its dependence on subsistence agriculture, with this activity involving the majority of the population. Extreme climate events—including frequent droughts and floods—regularly disrupt crop yields, exacerbating food insecurity. The most recent of these was the El Niño weather phenomenon, which caused exceedingly dry weather in 2024. Limited industrialization, creaking infrastructure, and an education system that struggles to equip the workforce with marketable skills further stifle economic growth. Additionally, Malawi’s landlocked geography makes trade expensive and hinders access to global markets. Government inefficiencies, corruption, and high population growth further compound these issues. Substantial financial support from foreign creditors provides the economy with a lifeline but has also led to external debt accumulation; Malawi has been in debt default since 2022.

6th poorest country: South Sudan

GDP per capita 2026 Consensus Forecast: USD 683

South Sudan’s poverty is tied to its protracted civil war, which erupted soon after the country gained independence in 2011. The violence displaced millions, destroyed infrastructure and disrupted agriculture, the backbone of the economy. In addition, mismanagement, corruption, and conflict over oil fields have led to inconsistent production and income of petroleum, South Sudan’s main revenue source. Ethnic divisions and fragile political institutions, high inflation, food insecurity, and a lack of education and healthcare further contribute to the country’s underdevelopment. A civil war in neighboring Sudan caused further havoc, with South Sudanese oil exports being shut in due to a pipeline being ruptured in Sudan in early 2024. Our Consensus is for the country’s GDP growth to roughly track the SSA average in the coming years, which will be insufficient to lift the country notably up the GDP per capita rankings.

7th poorest country: Burundi

GDP per capita 2026 Consensus Forecast: USD 692

Burundi’s poverty is a result of its history of ethnic conflict, most notably the 1993–2005 civil war, which shattered its economy and infrastructure. The country relies on subsistence agriculture, but the sector suffers from overpopulation, soil degradation, and limited access to modern farming techniques. Furthermore, political instability and corruption have deterred foreign investment and aid. Burundi also faces a poorly developed education and healthcare system, with the latter failing to prevent the spread of epidemics such as 2024’s mpox outbreak. Finally, frequent flooding has held back activity; in the year to September 2024, torrential rains affected 300,000 people and displaced close to 50,000.

8th poorest country: Mozambique

GDP per capita 2026 Consensus Forecast: USD 692

Mozambique’s underdevelopment stems from a history of colonial exploitation, followed by a drawn-out civil war that ended in 1992. Although the country has abundant natural resources—particularly large gas reserves—their mismanagement, combined with corruption, has limited their contribution to overall development. Infrastructure, particularly in rural areas, remains basic, hampering trade. Periodic natural disasters like cyclones and floods, coupled with an ongoing Islamic State insurgency in the north, have further disrupted economic progress. Mozambique is expected to see above-average growth among SSA economies in the coming years thanks to the extractive sector, though a large share of these economic gains are unlikely to filter through to the ordinary populace.

9th poorest country: Eritrea

GDP per capita 2026 Consensus Forecast: USD 704

Eritrea’s low GDP per capita level stems from the country’s reliance on subsistence agriculture and its status as one of the world’s most closed and repressive nations, which hampers investment and exports. The country does sell some zinc and gold—key sources of foreign exchange. A key threat to political stability is the potential sudden passing of the elderly leader of nearly three decades. Such an event could trigger a fierce succession battle and lead to a level of instability the country has not previously experienced. Tensions with neighboring Ethiopia spilling into conflict are a further risk.

10th poorest country: Somalia

GDP per capita 2026 Consensus Forecast: USD 717

Somalia’s extreme poverty is primarily a result of decades of civil war, the collapse of central government authority, and an ongoing insurgency by the Al-Shabaab militant group. The prolonged absence of a functional government has left infrastructure, including schools, hospitals and roads in a state of disrepair, and piracy and terrorism have scared off potential investors. Clan-based power struggles and fragmented political control make it difficult to implement national development policies. Moreover, the country also suffers from frequent droughts, which devastate agriculture and lead to chronic food insecurity. On the flipside, flooding can also occur, as observed in 2023–2024 due to the El Niño weather pattern; the late-2023 rainy season led to torrential downpours affecting 2.5 million people. More positively, the country benefits from international aid, plus an African Union peacekeeping mission.

11th poorest country: Niger

GDP per capita 2026 Consensus Forecast: USD 780

Niger’s poverty is partly driven by its harsh desert climate, which limits agricultural productivity and contributes to frequent droughts. Moreover, as a landlocked country, it faces challenges in accessing international markets, exacerbating its reliance on low-income farming. The fertility rate—one of the highest in the world—puts immense pressure on the country’s limited resources, particularly in terms of food and basic services. Additionally, Niger’s weak governance, high corruption levels, and ongoing security threats from extremist groups in the Sahel region further undermine development efforts. 2023’s successful coup exacerbated matters by reducing international aid and leading to sanctions by ECOWAS, a regional trading bloc—though the latter have since been lifted.

12th poorest country: DR Congo

GDP per capita 2026 Consensus Forecast: USD 819

The Democratic Republic of the Congo (DRC) is incredibly resource-rich—the country is the main producer of cobalt for instance, a key element in lithium-ion batteries. However, the DRC remains deeply impoverished. Civil wars and conflict, fueled by competition over minerals, have devastated infrastructure and led to millions of deaths and displaced citizens over the years. Fighting with the M23 militia—allegedly backed by Rwanda—continues in the east of the country. Widespread corruption, especially in the mining sector, prevents wealth from reaching the population; the government is ineffectual and unable to provide basic services such as healthcare, education or security. In the coming years, our panelists project that GDP growth should be rapid by regional standards, boosted by foreign investment in mining and transport infrastructure, though economic hardship will persist for many.

13th poorest country: The Gambia

GDP per capita 2026 Consensus Forecast: USD 977

The Gambia’s economy is undiversified and relies on tourism and nut exports. Moreover, the authoritarian rule of Yahya Jammeh (1994–2017) left a legacy of corruption and weak institutions that continue to hinder development. Additionally, high youth unemployment and limited access to quality education contribute further to widespread poverty, with many Gambians resorting to irregular emigration in search of better opportunities. More positively, the country appears relatively politically stable under the current leadership of Adama Barrow, which should aid investment going forward. The construction and tourism sectors, in particular, should push up GDP growth above the SSA average in the coming years.

14th poorest country: Liberia

GDP per capita 2026 Consensus Forecast: USD 1050

Liberia’s poverty is rooted in the aftermath of two devastating civil wars (1989–1997 and 1999–2003), which destroyed much of its infrastructure and left its institutions weak. Although the country is rich in natural resources such as iron ore, gold and rubber, corruption and mismanagement have prevented these industries from benefiting the broader population. The Ebola outbreak in 2014 further crippled the already shaky healthcare system and set back economic recovery efforts. Additionally, Liberia’s education system is underdeveloped, limiting opportunities for workforce development. That said, our Consensus is for the economy to grow faster than the SSA average over the coming years, supported by IMF funding and the development of the mining sector.

15th poorest country: Lesotho

GDP per capita 2026 Consensus Forecast: USD 1072

Lesotho has numerous economic difficulties. The country’s landlocked, mountainous location near the bottom of the African continent hinders trade. Moreover, reliance on South Africa—a far larger country which completely envelopes Lesotho—is a hindrance given how poorly South Africa’s economy has performed in recent years. The country relies on a few narrow industries, chiefly diamonds and textiles, both of which are at risk from U.S. tariffs and fluctuations in external demand. Widespread corruption and violence are further problems. As a result, economic growth is forecast to be around half the SSA average going forward.

16th poorest country: Sierra Leone

GDP per capita 2026 Consensus Forecast: USD 1085

Sierra Leone’s underdevelopment is rooted in the aftermath of its brutal 1991–2002 civil war, which decimated infrastructure and strangled economic activity. Although rich in diamonds, resource mismanagement and corruption have prevented the economic returns from mining reaching the broader population. The country also suffers from poor governance and a fragile healthcare system, which was further strained by the 2014–2016 Ebola outbreak. Agriculture, the primary livelihood for many, remains unproductive due to outdated techniques and low investment.

17th poorest country: Rwanda

GDP per capita 2026 Consensus Forecast: USD 1085

Rwanda has seen a remarkable recovery since the 1994 genocide, with GDP per capita tripling so far this century. The country’s stable political environment, lack of corruption, and strong state-led development plan have all aided growth. However, poverty persists—particularly in rural areas. While the government has made strides in rebuilding infrastructure and diversifying economic growth, agriculture still accounts for around a quarter of GDP and a majority of employment. Moreover, limited natural resources and political instability in the neighboring DRC further constrain development. In addition, in 2025, the economy has taken a blow from EU sanctions on gold exports due to Rwanda’s involvement in conflict in the eastern DRC. But overall, Rwanda is expected to remain one of Africa’s top-performing economies in the coming years due to sustained expansions in the agriculture, industry and services sectors.

18th poorest country: Ethiopia

GDP per capita 2026 Consensus Forecast: USD 1136

Ethiopia’s relative poverty stems from a longstanding mix of factors such as drought and degraded land, political instability, conflicts, ethnic tensions and a large, inefficient state-led economy. However, the economy has seen one of the continent’s best economic growth trajectories in recent years thanks to deep structural reforms, IMF support and an infrastructure push, and this strong economic performance should continue in 2026.

19th poorest country: Mali

GDP per capita 2026 Consensus Forecast: USD 1137

Mali is highly reliant on agriculture, particularly cotton and livestock, making it vulnerable to climate change, droughts, and desertification. Additionally, corruption and shoddy infrastructure have discouraged foreign investment, keeping Mali trapped in poverty despite its sizable natural resources—particularly gold. Poverty is exacerbated by ongoing conflict in the northern regions against Islamist insurgencies and rebel groups, as well as by recurring political instability; successful coups took place in 2020 and 2021 for instance. The security situation has worsened in recent years due to the withdrawal of both French and UN peacekeeping troops.

20th poorest country: Guinea-Bissau

GDP per capita 2026 Consensus Forecast: USD 1171

Guinea-Bissau struggles with political instability: Frequent coups and a lack of effective governance have prevented the development of institutions and infrastructure. Drug trafficking is another major issue; Guinea-Bissau serves as a transit hub for cocaine smuggling, further eroding government stability. Moreover, the economy is largely dependent on nut exports, making it vulnerable to global market fluctuations and extreme weather. In addition, limited access to education, healthcare, and clean water keeps much of the population in poverty. That said, the economy should grow above the SSA average over our forecast horizon, thanks to IMF financial support and healthy infrastructure investment.

Originally published in December 2017, updated in December 2025