Overview: Israel’s recent conflicts and political climate

Since 7 October 2023, Israel has been embroiled in its most sustained and multi-fronted conflict in decades. The initial, devastating assault by the Palestinian militant group Hamas, which resulted in 1,200 deaths and the capture of 253 hostages, triggered a massive military response in the Gaza Strip with the stated aims of dismantling the military and governing capabilities of Hamas and securing the return of all hostages. For regularly updated macro and risk projections, see our Consensus Forecast. This, however, was merely the opening act of a wider, escalating regional crisis.

Almost immediately, Hezbollah, an Iran-backed militia in Lebanon—for years regarded as a powerful foe by Israel—began its own campaign of attacks on northern Israel in solidarity with the Palestinians. This led to a simmering, attritional conflict along the border, forcing the evacuation of over 96,000 Israelis from their homes and causing significant damage to property and land. From October 2023 to September 2024, over 10,000 cross-border attacks were recorded, the vast majority launched by Israel into Lebanon. The fighting marked the most significant escalation between Israel and Hezbollah since their 2006 war. For additional context and updated projections, consult our Consensus Forecast.

The shadow of Iran has loomed large over these conflicts. Tehran, which supports both Hamas and Hezbollah, has seen its “axis of resistance” strategy severely tested: The war has not only weakened Hamas and Hezbollah, but also led to direct state-on-state confrontations. In April 2024, Iran launched its first-ever direct missile and drone attack on Israel, which was largely intercepted. This was followed by more direct exchanges, including Israeli strikes on Iranian nuclear facilities and military personnel in June 2025. This direct conflict, though short-lived, represented a perilous new phase in the long-running cold war between the two nations.

The impact on Israel’s GDP of recent conflicts

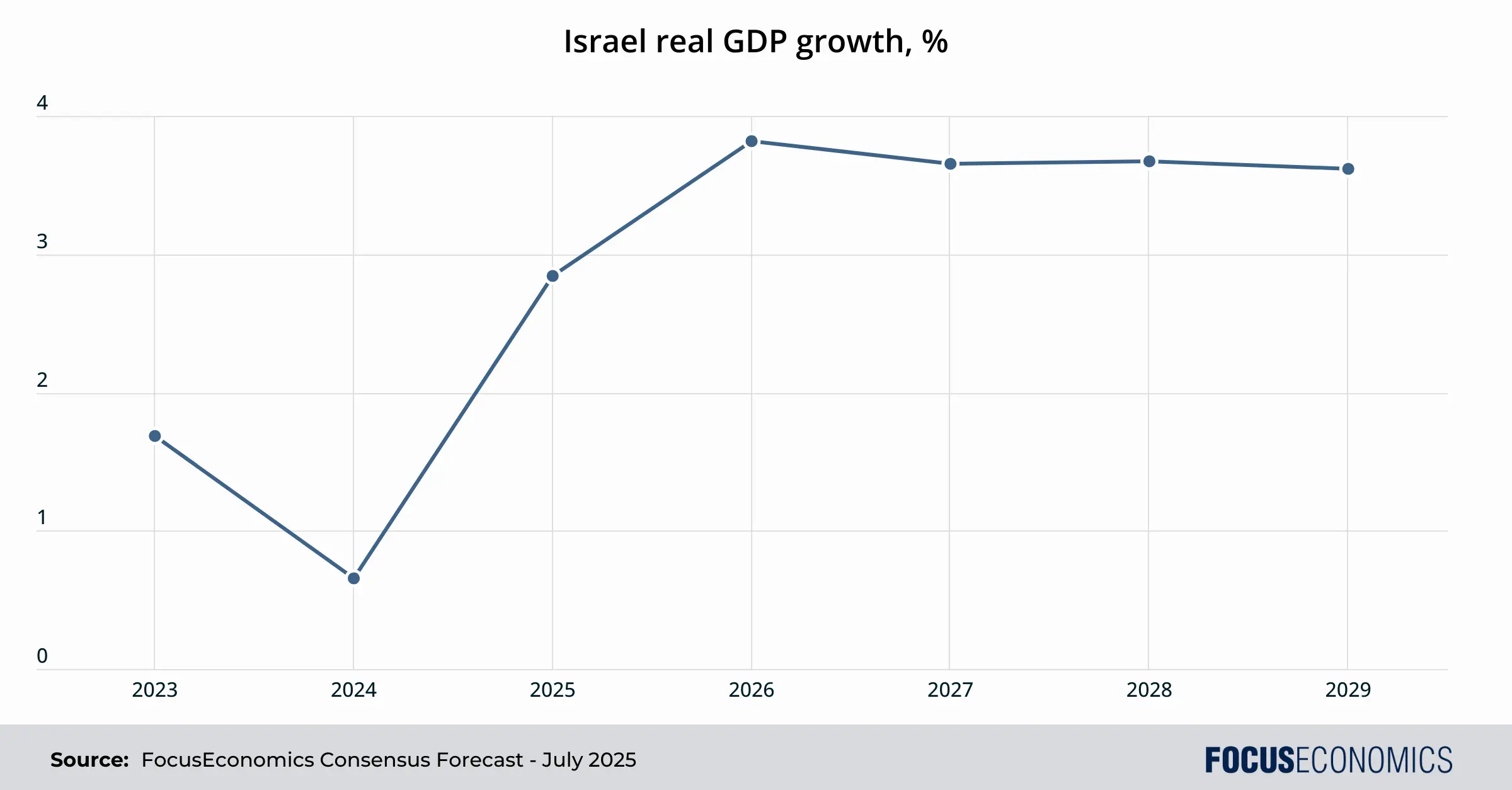

The multi-front war has exacted a notable price on Israel’s once-booming economy. The immediate aftermath of the 7 October attacks saw the economy contract sharply: In the final quarter of 2023, Israel’s GDP plummeted by an annualized 21%, driven by drops in private consumption, exports and business investment. While the economy showed some signs of recovery in early 2024, economic growth in the year as a whole was just 0.7% compared to the 3%+ readings that had been the norm in prior years.

The economic hit came from multiple channels. The call-up of reservists to fight tightened the domestic labor market and depressed private spending. Moreover, the reduction in Palestinians entering Israel for work hampered the construction sector. Finally, tourist flows dried up, and economic activity in the border region with Lebanon was disrupted by Hezbollah rocket attacks.

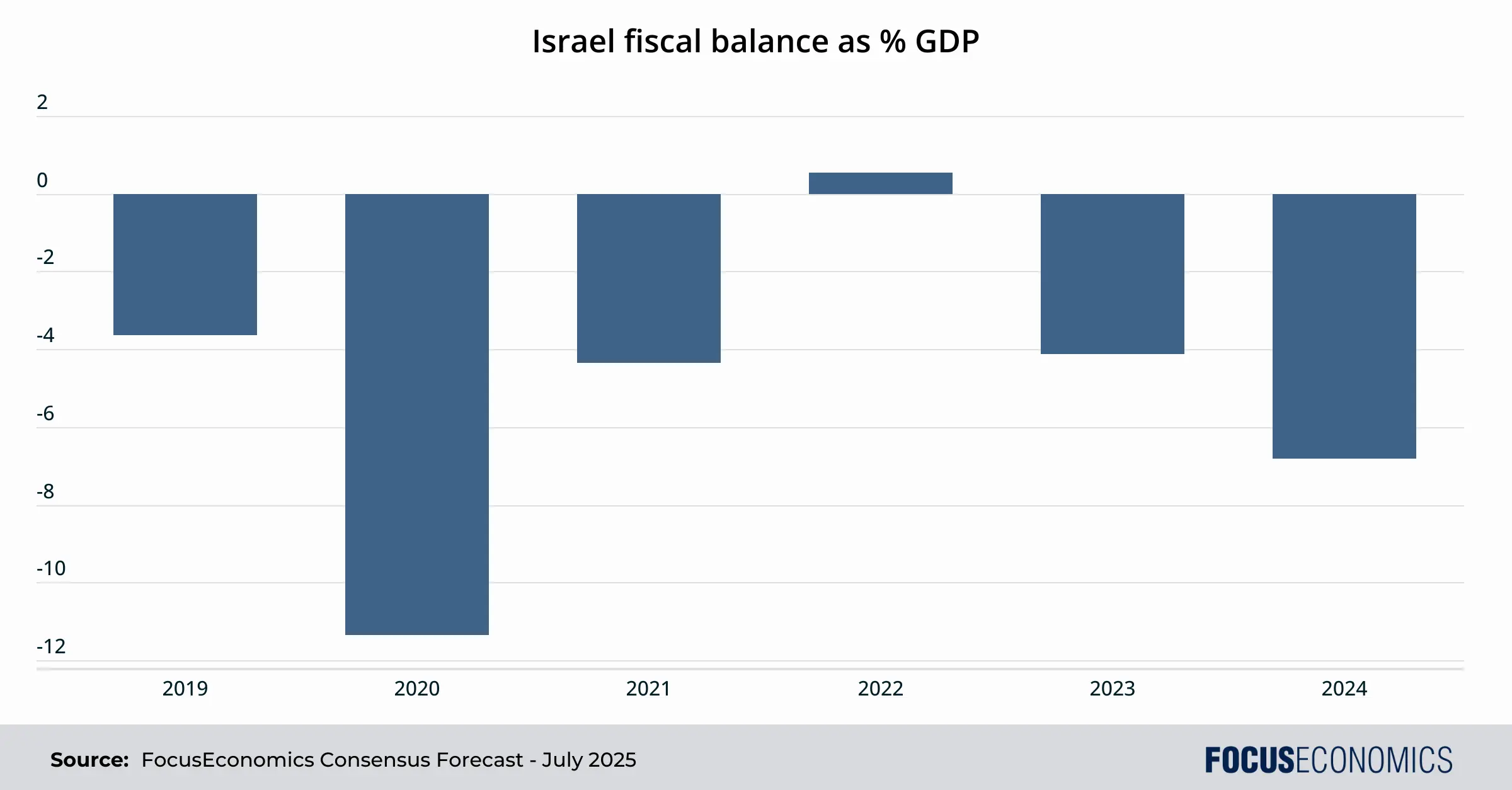

The sheer cost of the military operations is staggering. Last year, the Bank of Israel estimated that the direct war-related costs for 2023–2025 could reach USD 55.6 billion, equivalent to about 10% of the country’s GDP. This immense expenditure has weakened the nation’s finances: The budget deficit swelled to 6.8% of GDP last year, the highest since the pandemic, while the government’s debt-to-GDP ratio is set to jump from around 60% before the war to nearly 70% this year. To attempt to rein in the deficit and debt, the government has proposed austerity measures, including a 3% cut across all ministries, and increased the value-added tax (VAT) rate from 17% to 18% in early 2025.

The economic strain has not gone unnoticed on international markets. Both S&P and Moody’s have downgraded Israel’s credit rating since the Gaza war began, citing the risks of the ongoing conflict and the potential for significant additional military spending. This will raise the government’s future borrowing costs, further compounding the financial pressure.

How key economic sectors are faring

Tourism: Israel’s tourism industry has been decimated. Before the conflict, the country was on track to welcome a record 5.5 million visitors in 2023. That prospect evaporated overnight. In the fourth quarter of 2023, tourist arrivals plunged around 80% compared to the previous year and remained similarly depressed for much of 2024. 2025’s incipient recovery was set back by the brief missile exchange with Iran that saw visitor numbers plummet in June. A full recovery could take multiple years and is likely dependent on a permanent end to hostilities with Hamas, Hezbollah and Iran.

Technology: Tech is Israel’s economic linchpin. The high-tech sector contributes about 20% of Israel’s GDP, employs over 10% of the workforce, and makes up over half of the country’s exports. While the call-up of hundreds of thousands of reservists initially disrupted operations and the number of high-tech employees has roughly stagnated since 2022, the tech sector has proven resilient to the war.

High-tech GDP grew by 2.2% in the first three quarters of 2024, even as the overall economy contracted. Investor confidence, after an initial wobble, has seemingly returned. In 2024, Israeli tech companies raised over USD 12 billion, a 27% increase from the previous year, outpacing growth in European and Asian markets. The first half of 2025 saw this momentum continue, with firms raising USD 9.3 billion, the strongest six-month period for tech funding in three years. Crucially, the share of funding rounds involving global investors increased, signaling long-term confidence in Israeli innovation despite the complex security situation.

Merger and acquisition (M&A) activity has also been strong, hitting a record USD 15.8 billion in 2024. This reflects a maturing business ecosystem, shifting from a “startup nation” to a “scale-up nation” with more established companies attractive for acquisition. Cybersecurity firms have led the fundraising charge, followed by enterprise software. The conflict has also spurred renewed investment in security-focused artificial intelligence (AI), a field where Israel is a global leader.

Energy: Israel’s natural gas output has rapidly become a cornerstone of its economy over the last decade. The discovery of major offshore fields like Leviathan and Tamar has transformed the nation from a net importer to a significant energy exporter, ensuring its own energy independence and generating substantial state revenue.

Progress on the gas front has been largely unimpeded by the conflicts of the past years: In 2024, Israel’s total natural gas production from the Leviathan, Karish and Tamar fields reached 27.38 billion cubic meters, representing an 8.3% increase compared to 2023. That said, the June 2025 missile exchange with Iran caused the government to temporarily close two of its three gas fields and halt exports.

Long-term economic outlook for Israel

GDP: Economic growth should accelerate this year from 2024 but remain below the historical trend. The 12-day conflict with Iran caused damage to buildings and other infrastructure and sharply disrupted economic activity by halting many non-essential services, trade, travel and shipping, and temporarily shutting down Israel’s gas fields. The Gaza conflict continues to weigh on the labor market as military reserve duty remains in place. Moreover, government consumption surged last year due to war-related military and civilian support, but this will partly unwind this year, limiting growth. Persistent security threats will slow the rebound in domestic spending, discourage tourism and weaken investment. In addition, new tax policies effective from January prompted early purchases in late 2024, likely reducing consumer durable demand in 2025. Business investment will begin to rebound in 2025, though concerns over global trade policies will temper the pace of recovery.

Looking beyond 2025, our panelists currently expect economic growth to return to its pre-war trend of 3+% per year, likely predicated on an end to conflict in Gaza enabling a full recovery in tourism and domestic employment. European moves to cut reliance on Russian energy will boost Israel’s gas exports and investment in hydrocarbons, while rapid population growth will underpin domestic consumption. Moreover, the tech industry should be buoyed by the growing technological intensity of the global economy, particularly with regard to AI.

Unemployment: Our Consensus is for the Israel’s unemployment rate to average between 3.0 and 4.0% in the coming years, below the OECD and global averages thanks to the expected uptick in economic growth boosting job creation and allowing Israel’s economy to largely absorb the large cohorts of youth joining the labor market each year.

Interest rates: In line with global trends, interest rates in Israel will decline in coming years. The Central Bank’s policy rate should fall from 4.50% currently to around 3% by 2029. That said, this figure would be well above pre-Covid trends: Greater world protectionism and focus on local supply chains will make Israel’s inflation rate structurally higher than in the past.

Government spending: After rising at a double-digit pace in 2024 due to the war, government spending is expected to see only minimal growth each year out to 2029, and well below the overall rate of GDP growth. Fiscal restraint will aim to pare back the budget deficit and stabilize the public debt-to-GDP ratio.

Challenges and opportunities ahead

Renewed hostilities with Iran or Hezbollah plus an expanded offensive in Gaza are the key downside risk to Israel’s economy. The brief missile exchange between Israel and Iran in June 2025 was enough to lead our panelists to slash their 2025 GDP growth outlook by 0.4 percentage points. The hit to economic activity from further conflict would be felt across sectors. A second key risk is future political moves that undermine institutional checks and balances, such as the further weakening of the supreme court. This would threaten investor confidence and thus both domestic and foreign investment in Israel. Higher U.S. tariffs are another concern; Israel is theoretically in line for a 17% U.S. “reciprocal” tariff in the absence of a trade deal.

If Israel’s conflicts with its adversaries subside, democratic checks and balances are preserved and tariffs don’t become too onerous, Israel has numerous strengths to leverage: A relatively young, fast-growing population, a world-beating tech sector and a burgeoning gas industry. Economic rapprochement with neighboring Arab nations, which has been largely put on ice since the Gaza war, could resume if conflict ends, further knitting Israel into regional trade networks; the formalization of diplomatic and economic ties with Saudi Arabia would be a particularly large prize.

Domestic challenges would persist even in such a scenario. The country’s political system is chronically unstable; since the late 1980s, no government has completed a four-year term, hindering long-term policymaking. The education system is underperforming vs the OECD average, infrastructure is shoddy, and Arabs plus orthodox Jews have much lower labor participation rates than other Israelis. Israel is thus a country with immense potential—but the challenges it faces are just as large.