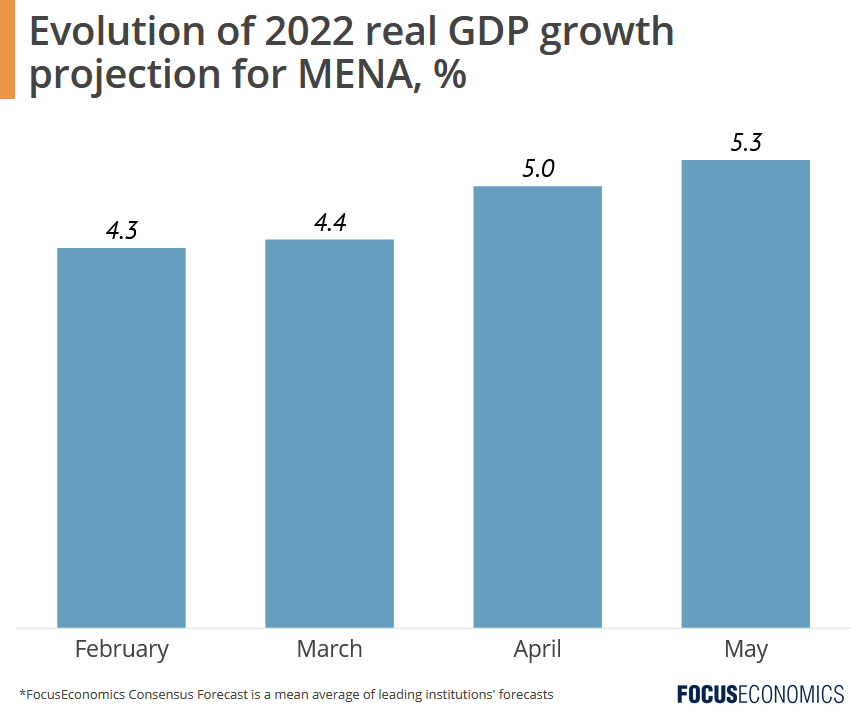

Most of the regions that we cover have seen downgrades in their economic projections as a result. These declines in expectations have been particularly large in the Euro area and Eastern Europe. But there is one region which has seen its forecasts revised upwards: the Middle East and North Africa (MENA). Since February, our analysts have upgraded their 2022 growth forecasts for MENA by a full percentage point to 5.3%, and have also revised up their projections for 2023.

Surging energy prices as a result of the war in Ukraine have been the main driver behind the re-rating, given MENA’s position as a key exporter of oil and gas. The unexpected windfall to public finances should enable governments to step up spending—or, at the very least, to refrain from adopting austerity measures. The introduction of a VAT in Kuwait and Qatar, for instance, is likely to be delayed to 2024. The windfall is also encouraging greater fiscal generosity towards the region’s more vulnerable oil importers: In April, the Gulf states pledged USD 22 billion to Egypt to cover the country’s current account deficit, while Saudi Arabia sent Jordan USD 50 million to prop up its budget.

That said, turning these ephemeral economic gains into something more durable will require a doubling-down on diversification efforts. MENA is still the most dependent region on fossil fuels by far. Oil rents account for 12% of GDP according to the latest data. Positively, virtually all MENA oil exporters now have comprehensive diversification plans in place; Saudi Arabia’s Vision 2030 is the prime example. Plus, the last year has seen a series of economic reforms to make the region a better place to do business, with the UAE leading the way with a barrage of measures tackling everything from the structure of the working week to unemployment insurance. Finally, inter-regional trade ties are strengthening: The embargo on Qatar was lifted in early 2021, while Israel has signed a host of deals with its Arab neighbors in recent years, most recently with the UAE.

-

Insight from our analysts

On economic prospects in the Gulf, Daniel Richards, senior MENA economist at Emirates NBD, said:

“The outlook for the GCC economies is constructive. Growth will be driven by increased investment and production in the hydrocarbon sectors, while the non-oil sectors will continue to recover from the pandemic contraction as restrictions have been eased, Covid-19 vaccination rates are high and international travel rebounds. However, higher inflation, slower global growth and rising interest rates are likely to prove headwinds to growth in the non-oil sectors. Improved fiscal dynamics for GCC oil exporters will allow governments to cushion some of the impact of higher global energy and food prices on their consumers, if they choose to do so.”

Farouk Soussa, economist at Goldman Sachs, commented on Egypt:

“Egypt has received close to USD 13 billion in financial support so far from the Gulf, staving off the need for a sharper economic adjustment to the balance of payments shock it experienced in the wake of Russia’s invasion of Ukraine. This has provided breathing space to negotiate a new programme with the IMF. […] Policy makers appear focused on structural reforms, namely promoting private and foreign direct investment in the manufacturing/tradable sector. A range of initiatives are being launched to achieve these aims, including announced privatisations and a new traffic-light system indicating the state’s degree of involvement in various sectors of the economy.”